How Can You Find the Exceptions to the Closing Date Report?

In financial management, closing date reports are crucial since they provide a snapshot of a company's financial status at a specific time. However, these reports can sometimes contain exceptions - anomalies, or discrepancies. Understanding and finding these exceptions is essential for accurate financial reporting, auditing, and tax compliance.

Contents

Understanding Closing Date Reports

What are Exceptions in Closing Date Reports?

Why is it Important to Find Exceptions?

Tax Exception Detection in Closing Date Reports

How to Find Exceptions in Closing Date Reports in QuickBooks

Frequently Asked Questions

Understanding Closing Date Reports

Closing date reports are financial statements summarizing a company's economic activities over a specific period, typically a fiscal quarter or year. These reports include various components such as income statements, balance sheets, and cash flow statements, providing a comprehensive view of a company's financial health.

What are Exceptions in Closing Date Reports?

Exceptions in closing date reports are typically inconsistencies or discrepancies that deviate from the norm. These could be unbalanced entries, missing transactions, or differences between financial statements. For example, a sales transaction recorded in the income statement but missing from the cash flow statement could be an exception.

Why is it Important to Find Exceptions?

Identifying exceptions in closing date reports is crucial for several reasons. Firstly, these exceptions can significantly impact a company's financial reporting, leading to inaccurate financial statements. Secondly, exceptions play a critical role in auditing and compliance. Auditors look for these exceptions to identify potential issues or areas of concern in a company's financial management. For example,

1. Incorrect Transaction Dates

Discrepancies in the closing date report may result from transactions recorded with incorrect dates. For example, a transaction in January might be mistakenly recorded as happening in February and could lead to inaccuracies in monthly financial statements.

Example: A business records a large sale on February 1st, but the transaction occurred on January 31st and could significantly impact the revenue reported for January and February. By identifying this exception, the business can correct the transaction date and ensure accurate reporting for both months.

2. Duplicate Transactions

Duplicate transactions can occur due to human error or system glitches. These duplicates can inflate revenue or expense figures and distort the business's financial picture.

Example: A business records a $500 payment from a customer twice due to a system error and would inflate the revenue for that period by $500. Identifying this duplicate transaction would allow the business to correct the error and ensure accurate revenue reporting.

3. Missing Transactions:

Transactions may not be recorded due to oversight or system issues, leading to under-reporting revenues or expenses.

Example: A business should remember to record a significant expense transaction, which could lead to an overstatement of profit for the period. Identifying this missing transaction would allow the company to correct the oversight and ensure accurate expense and profit reporting.

4. Incorrect Account Classification:

Transactions may be recorded under inaccurate accounts, leading to misclassifying revenues, expenses, assets, or liabilities.

Example: A business records a purchase of equipment (an asset) as an expense which would understate the asset value and overstate the costs for the company. Identifying this misclassification would allow the business to correct the error and ensure accurate asset and expense reporting.

5. Unbalanced Journal Entries:

In double-entry bookkeeping, each transaction should have a corresponding entry to balance the books. Transactions, when recorded incorrectly, can lead to unbalanced journal entries.

Example: A business records a $1000 payment from a customer as a debit to the cash account but needs to remember to record the corresponding credit to the accounts receivable account, which would leave the journal entry unbalanced. Identifying this exception would allow the business to complete the journal entry and maintain balanced books.

Tax Exception Detection in Closing Date Reports

Identifying exceptions in closing date reports is crucial for accurate financial reporting, auditing, and tax purposes. Here are a few tax-related use cases:

Income Tax Reporting:

Exceptions in income statements can lead to incorrect reporting of revenues and expenses, affecting the calculation of taxable income. For instance, an unrecorded revenue transaction can lead to under-reporting income, resulting in lower tax liability. Detecting such exceptions can help ensure accurate income tax reporting.

Sales Tax Compliance

If your business collects sales tax, sales transaction exceptions can impact your tax liability. For example, a sales transaction recorded without the corresponding sales tax can lead to under-collection and under-remittance of sales tax, potentially resulting in penalties and interest.

Asset Depreciation

Exceptions related to asset transactions can affect the calculation of depreciation expenses, which are often tax-deductible. An asset purchase not recorded in the books can lead to missed depreciation deductions, resulting in higher taxable income.

Using a tool like QuickBooks to identify and correct exceptions in each case can help ensure tax compliance and accurate tax reporting.

How to Find Exceptions in Closing Date Reports in QuickBooks

QuickBooks, a popular accounting software, offers tools to help identify exceptions in closing date reports. Here's a step-by-step guide:

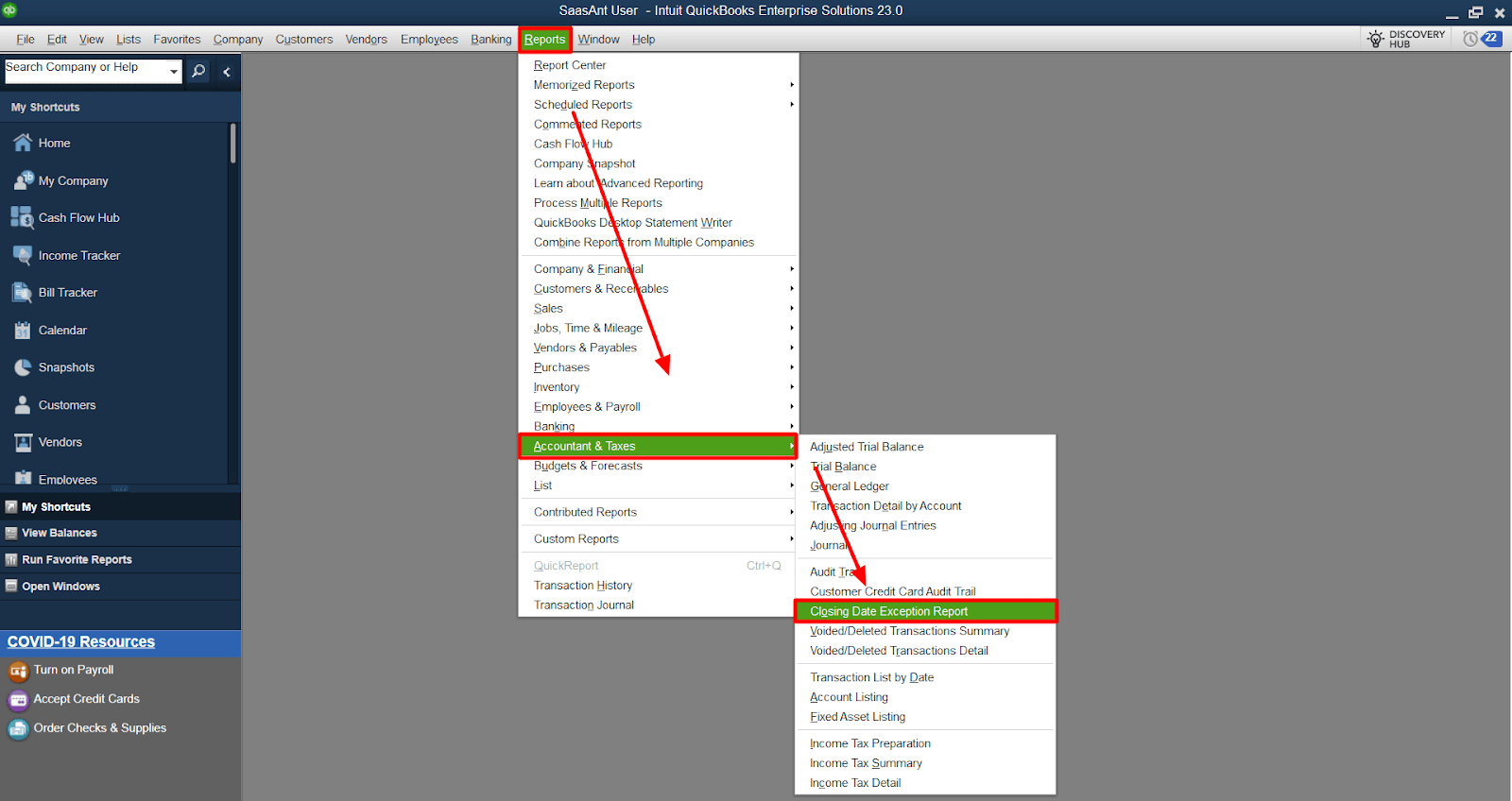

1. Open the Closing Date Exception Report: Navigate to the 'Reports' menu, select 'Accountant & Taxes', and then 'Closing Date Exception Report.'

2. Review the Report: Look for transactions dated after the closing date. These are potential exceptions.

3. Investigate Each Exception: Click on each exception to view the transaction detail, which will help you understand why the exception occurred.

4. Correct the Exceptions: Depending on the nature of the exception, you may need to edit the transaction, delete it, or enter a new transaction to correct the discrepancy.

Remember, the key to efficient exception detection is a regular review and thorough investigation.

Identifying exceptions in closing date reports is essential to financial management, auditing, and tax compliance. With tools like QuickBooks, identifying and addressing these exceptions can be easy.

Frequently Asked Questions

1. What is a Closing Date Report?

A Closing Date Report is a document that provides a summary of all financial transactions and balances up to a specific closing date. It's often used in businesses to mark the end of a financial period.

2. How to handle exceptions in a Closing Date Report?

Exceptions in a Closing Date Report typically refer to discrepancies or irregularities that don't align with the expected data. These can be handled by identifying the source of the exception and making necessary corrections or adjustments in the financial records.

3. What causes exceptions in a Closing Date Report?

Various factors, such as data entry errors, unprocessed transactions, or discrepancies in financial data, result in exceptions in a closing date report. Identifying the cause is crucial to resolving the anomaly.

4. How to prevent exceptions in a Closing Date Report?

Preventing exceptions in a Closing Date Report can be achieved by maintaining accurate financial records, regularly auditing financial data, and ensuring all transactions are processed correctly and on time.

5. What are the implications of exceptions in a Closing Date Report?

Exceptions in a Closing Date Report can indicate potential issues in the financial data, such as inaccuracies or inconsistencies. If not addressed, these can lead to more significant financial discrepancies and impact the overall financial health of a business.

6. How to find and correct exceptions in a Closing Date Report?

To find and correct exceptions in a Closing Date Report, review the report to identify discrepancies. Once identified, trace the exception back to its source in the financial records. After finding the source, make corrections or adjustments, and recommend reviewing the processes that led to the exception.