How Do You Record Outsourced Payroll in QuickBooks Online

As companies grow and evolve, many outsource payroll management to streamline operations and improve efficiency. If your business uses QuickBooks Online, you might wonder: "How do you record outsourced payroll?" This article aims to clear up this common question.

Understanding outsourced payroll accounting can be challenging, particularly if you're a business owner using QuickBooks Online. The process of accurately recording outsourced payroll may appear complex, but fortunately, the remedy to this issue is more accessible than you might think.

This step-by-step guide provides a detailed walkthrough to record your outsourced payroll expenses and liabilities and equip you with the know-how to manage outsourced payroll in QuickBooks Online.

Step-By-Step Guide for Recording Outsourced Payroll without Any Payroll Liabilities

Step 1: Receive Your Payroll Summary Report

Your payroll service provider provides a payroll summary report containing all the critical data you need for QuickBooks entry.

Step 2: Note Your Payroll Liabilities

When you rely on a payroll service provider, remember that the provider reports and pays your payroll liabilities. You only need to handle entries for the gross pay of employees and any taxes withheld.

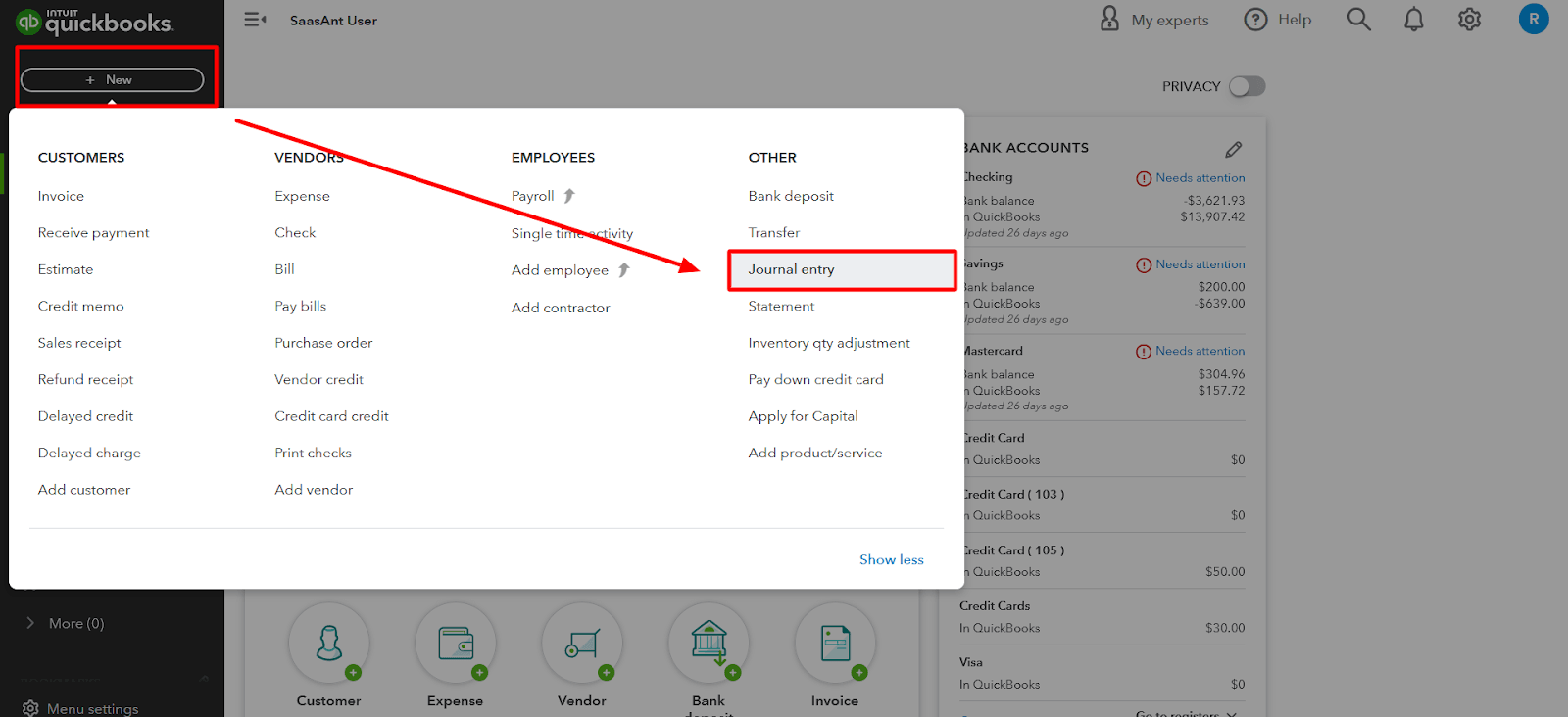

Step 3: Create a New Journal Entry

To start a new entry, click the '+New' button on the left panel of the home page. Select 'Journal Entry' under the 'Other' heading. This action opens the journal entry window.

Step 4: Input Paycheck Date and Journal Number

Next, input the paycheck date into the 'Journal Date' field. You can also enter a journal entry number into the 'Journal Number' field for your reference.

Step 5: Fill in the Debit and Credit Columns

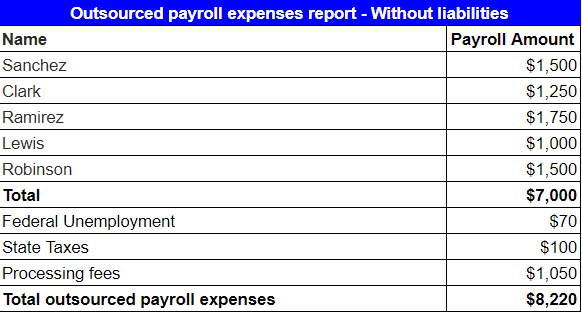

Let's look at a sample 'Payroll Expense Report' and briefly overview how we can fill in the debit and credit columns.

Track gross wages by debiting your expense account: Input the pay for the pay period.

Track Federal Unemployment payments by debiting your expense account: Input the total Federal Unemployment Tax withheld.

Track State taxes by debiting your expense account: Enter the total tax withholdings.

Track fees charged by your payroll service provider by debiting your expense account.

Finally, apply a credit to the bank account used for handling payroll. This action should reflect the complete payroll run provided by your payroll service, encompassing deductions from gross pay and processing fees.

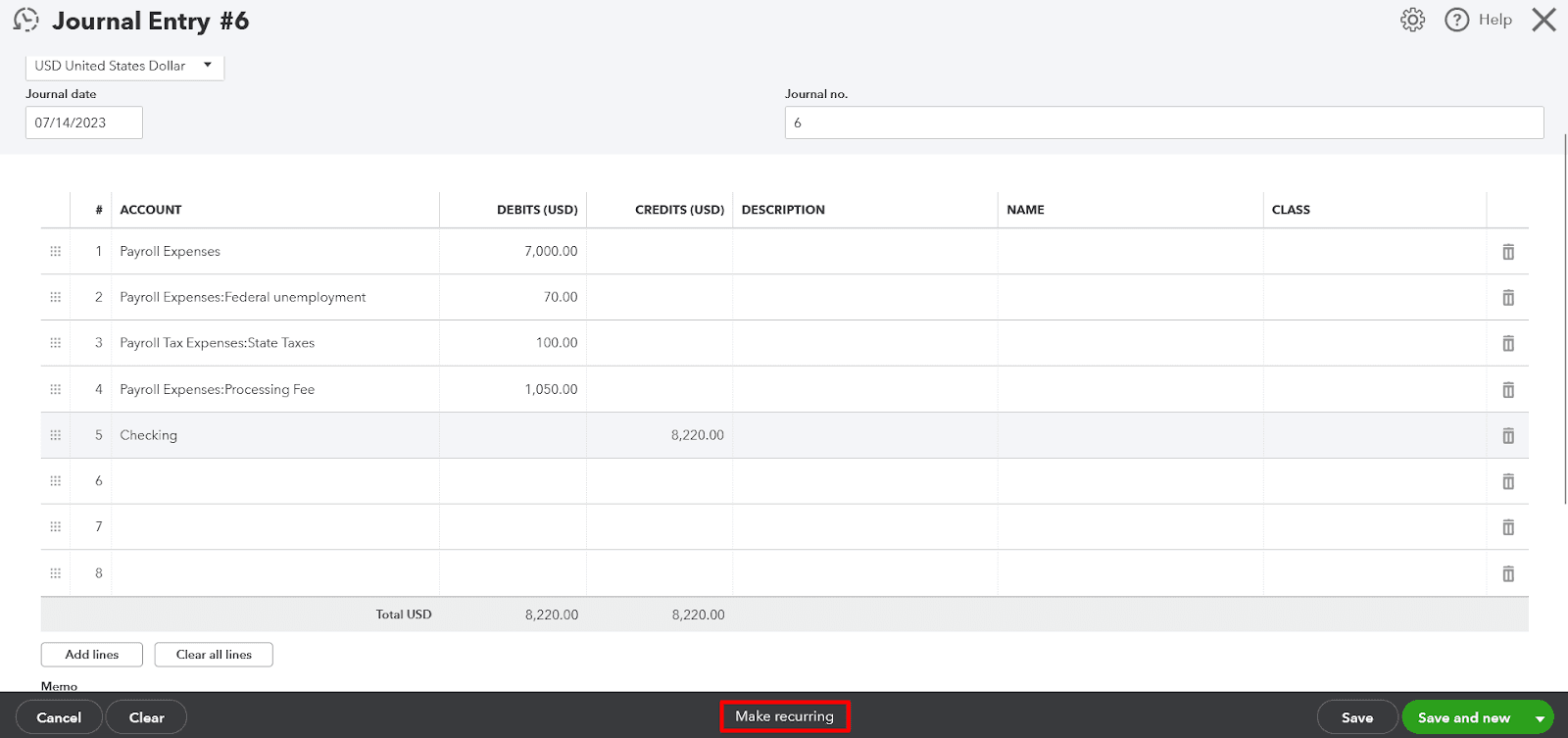

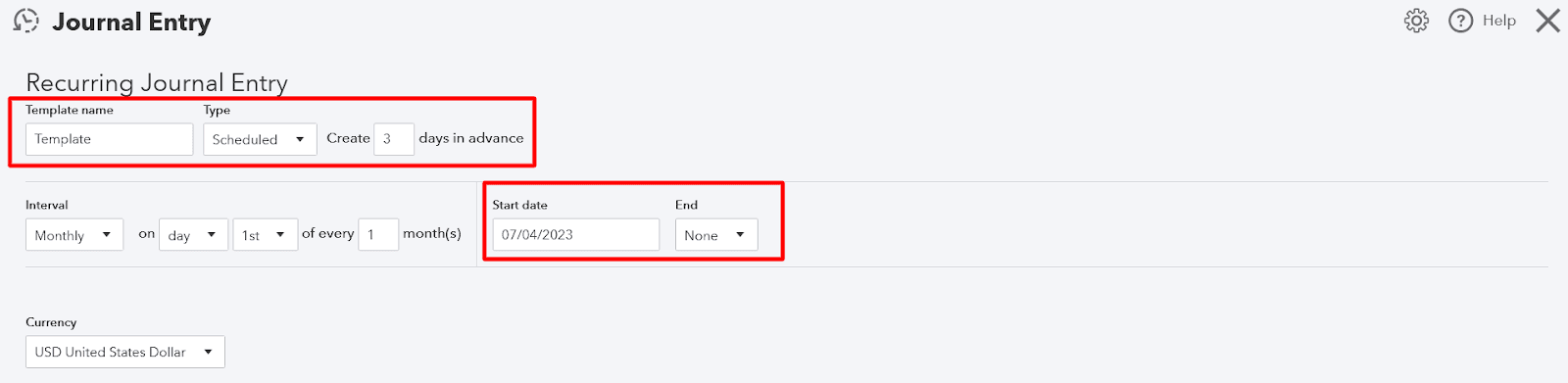

Step 6: Save as a Recurring Journal Entry

To make future entries easier, save this as a recurring journal entry. Click the 'Make Recurring' link at the bottom of the page.

Enter an identifiable name into the 'Template Name' field.

Set the template type to 'Unscheduled.' This way, you save the template without setting a specific recurrent schedule, so you can choose the template when necessary and modify the amounts.

Finally, click the 'Save Template' button to store this template for future use.

If you want to bring in historic data or speed up the process of payroll and other bookkeeping tasks, you can use SaasAnt Transactions, a complete bookkeeping automation suite.

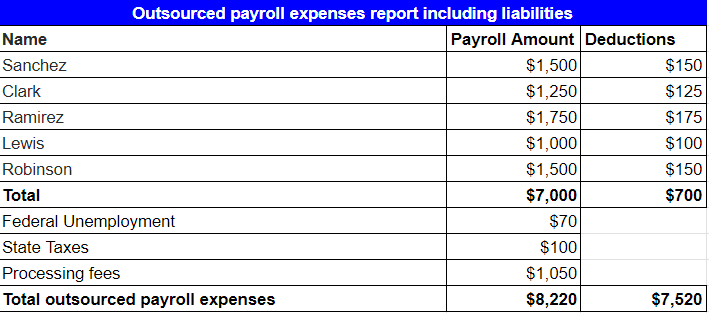

Step-By-Step Guide for Recording Outsourced Payroll While Including Liabilities

Let's look at a sample 'Payroll Expense Report,' including liabilities, and briefly overview how we can fill in the debit and credit columns.

Follow the below steps to account for these liabilities.

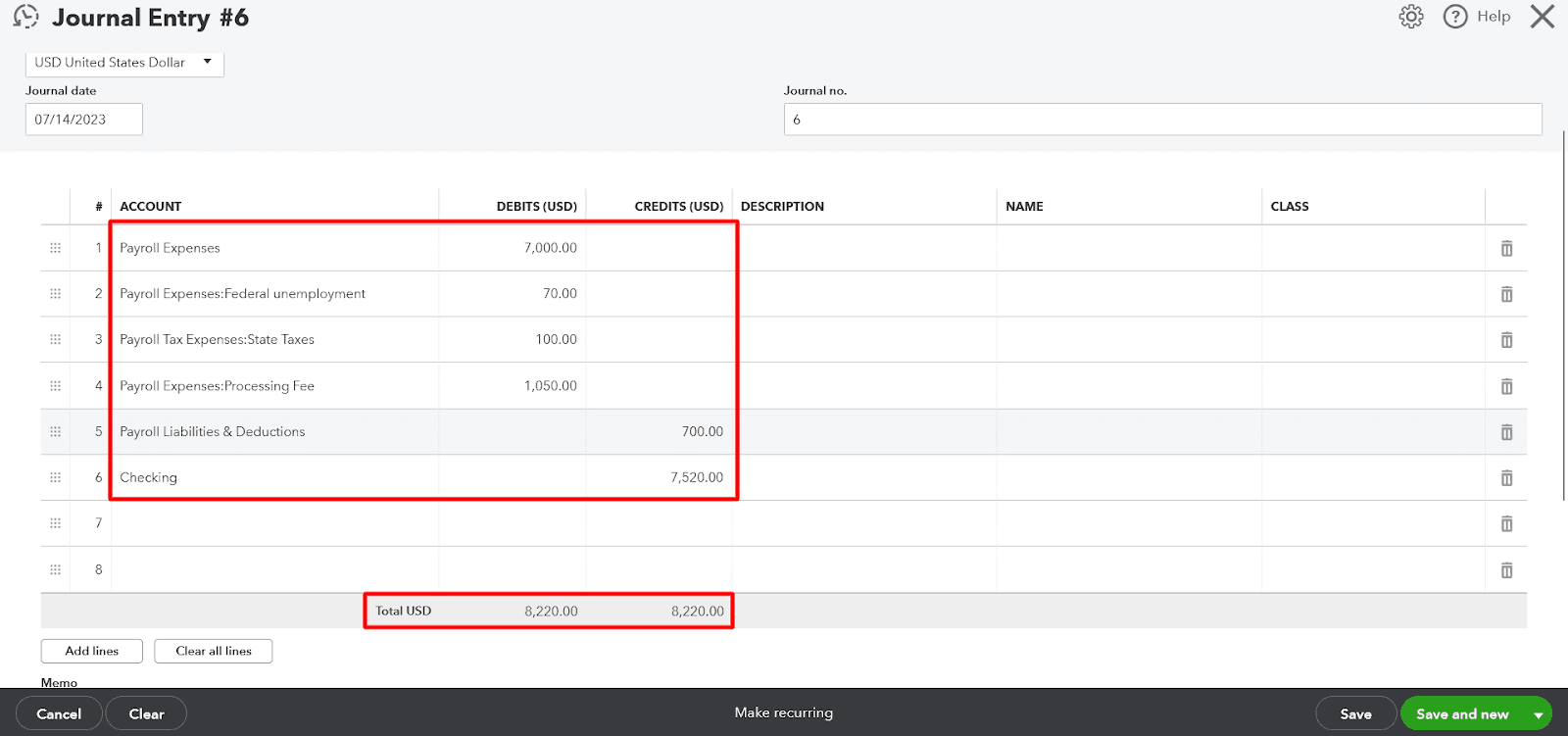

Step 1: Understanding the Payroll Structure

When you don't rely on a payroll service provider, you must account for the liabilities held for payment. You have to show the accrual of employer liabilities by recording three credit lines instead of a single one.

Step 2: Adjusting the Journal Entry Format

Firstly, you should credit the bank account used for processing payroll by the amount of the processing fee.

Next, record the total amount for the payroll liability by crediting the payroll liability account.

Finally, credit the bank account used for processing your payroll by the net paycheck amount, which is the total payroll amount less any payroll liabilities or deductions.

Step 3: Recording Payroll Liabilities

Record the payroll liabilities in the line above the final credit line. This process allows you to keep track of those amounts in a liability account until it's time to pay those liabilities.

Step 4: Understanding Withholding Taxes

Remember, federal and state employee withholding taxes aren't shown in the journal entries as these taxes are paid directly from the employee's gross pay to the tax agencies. As an employer, you act as a go-between for the employee and the tax agencies. Therefore, these are not an expense to you.

Step 5: Consulting with Your Payroll Service or Software

Consult your payroll service provider for precise withholding information and forms, or examine your supplementary software's associated features, if relevant.

Note: The examples above demonstrate the journal entries required to account for payroll manually. If you need to create a more complex payroll journal entry to account for items like insurance premiums or retirement contributions, consult with your accountant or payroll service. They will provide you with the necessary information to record for your company.

FAQs

Q1: How Do I Set up a Recurring Journal Entry for Payroll in QuickBooks Online?

To establish a recurring journal entry, click the 'Make Recurring' option at the bottom of the journal entry page. This feature makes future data entry easier.

Q2: Where Do I Enter Withholdings for Social Security, Medicare, and Other Deductions?

You should debit the respective expense accounts for each withholding, such as Social Security, Medicare, and Federal Unemployment. If applicable, do the same for state taxes.

Q3: Do I Need to Show Federal and State Employee Withholding Taxes in the Journal Entries?

Employees handle these withholdings, paying them directly to tax agencies from their gross pay; hence they're not an expense for the employer.

Q4: How Do I Categorize Payroll Service Fees in QuickBooks Online?

To track the payroll service fees, debit the expense account and enter the total processing fees your payroll company charges into this account.

Q5: What’s the Purpose of Crediting the Bank Account When Recording Outsourced Payroll in QuickBooks Online?

Crediting the bank account mirrors the outflow of money for the payroll run. This activity includes gross pay, deductions, and processing fees from your payroll company.

Q6: Can I Manage Both Payroll and Payroll Liabilities Using QuickBooks Online?

Yes, QuickBooks Online allows you to manage both payroll and payroll liabilities. You can adjust the journal entry format accordingly, depending on whether your business is responsible for payroll liabilities.

Tags

Read also

Import Journal Entries into QuickBooks Online: Step by Step Guide

How to Edit Journal Entries in QuickBooks Online

How to Delete Journal Entry in QuickBooks Online

How to Export Journal Entries From QuickBooks Online