Accounting Cost for Small Businesses: What You Need to Know

Accounting helps you track your financial performance, plan your budget, make intelligent decisions, and comply with tax laws. But what is the cost of accounting services for small businesses? Which factors determine the pricing of these essential services?

This blog will explore the costs of hiring an accountant for your small business, various bookkeeping services available, the fundamental accounting tasks every small business owner should know, and much more.

Contents

What is the Accounting Cost of a Business?

Cost of Accounting Services for Small Businesses

What Do Other Small Businesses Pay for Accounting Services?

What Makes Accounting Services More or Less Expensive? Here Are the Factors You Should Know

How Do You Pay Your Accountant? By the Hour or by Services Provided?

CPA vs. Bookkeeper Costs

CPA or Bookkeeper: Which is Right for Your Business?

How Do You Negotiate Your Accounting Fees Like a Pro?

Accounting Tasks for Small Business Owners

Outsource or Hire? How do you choose the best accounting option for your business?

Certified Public Accountants and Bookkeeping Services

How Do You Save Money on Accounting for Your Small Business?

FAQs

What is the Accounting Cost of a Business?

The accounting cost of a business refers to the explicit costs or expenses incurred during its operations. These costs are recorded in the company's financial statements and include rent, salaries, utilities, materials, and other operational costs.

Additionally, businesses might have costs like the depreciation of assets, interest on loans, and taxes. Knowing all these costs is important for planning how to spend money wisely and understanding if the business is making enough money to cover all these expenses.

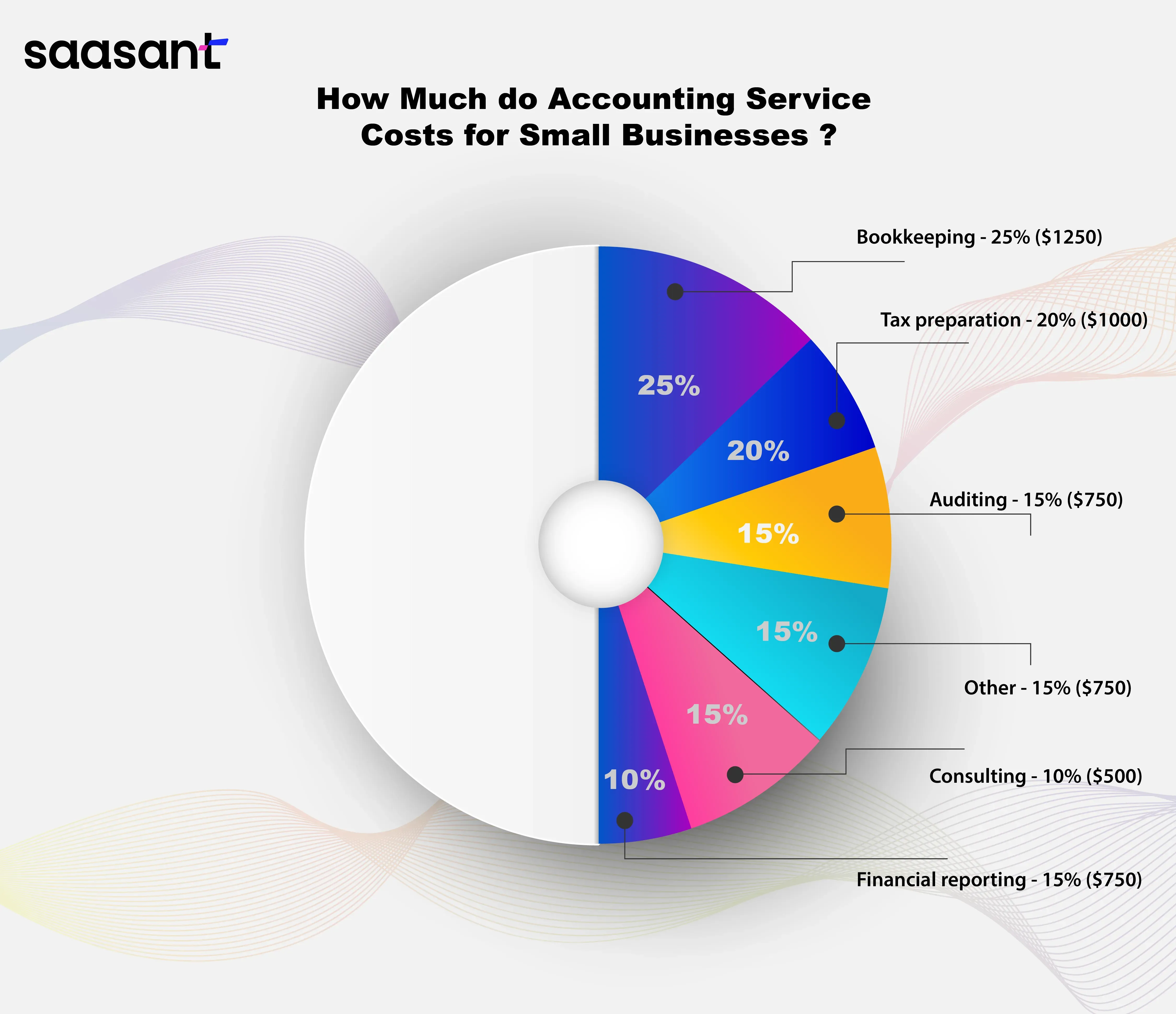

Cost of Accounting Services for Small Businesses

As a small business owner, you know that accounting is not just about numbers. It's about managing your money, reporting your finances, making intelligent decisions, and following tax laws. But how do you pick the right accounting services for your needs? And how much will they cost you? Understanding the average monthly costs associated with these services can help you budget effectively and ensure you're making informed decisions.

Here are some of the services you might need for your small business accounting and what you can expect to pay for them:

Bookkeeping Service: This basic service records your income and expenses and generates simple reports. Bookkeeping is essential for keeping track of your cash flow, managing your costs, and filing your taxes. You can expect to pay between $20 and $50 per hour for this service, depending on the number of transactions you have and their complexity (salary.com).

Payroll Service: Handles payments to your employees and contractors, including taxes and benefits. Payroll is a complex and tedious task that requires accuracy and compliance with federal, state, and local laws. You can expect to pay between $50 and $200 per month for this service, depending on the number of people you pay and the frequency of payments (business.com).

Tax Service: This service prepares and files your tax returns, helps you save on taxes, and addresses tax issues. Taxes are a crucial aspect of accounting as they impact your profit and legal obligations. You can expect to pay between $150 and $500 per return, depending on your business type and size and the complexity of your tax situation (Investopedia).

Audit Service: Auditing verifies the accuracy and reliability of your financial reports. An audit validates your financial statements and ensures compliance with accounting standards and regulations. Depending on the audit's scope and depth, you can expect to pay between $2,000 and $20,000 per year for this service (Harvard Law School).

Forensic Service: Forensic accounting detects and prevents financial crimes. This specialized field investigates fraud, embezzlement, money laundering, and other illegal activities. Depending on the case's nature and extent, you can expect to pay between $300 and $500 per hour for this service (howmuchisit.org).

Management Accounting Service: This service provides financial information and advice for your business. Management accounting uses your financial data to plan your budget, forecast revenue, analyze performance, and make strategic decisions. You can expect to pay between $100 and $300 per hour for this service, depending on the level of expertise and guidance you need.

Cost Accounting Service: Cost accounting analyzes and allocates your production, operation, or project costs. It measures your production or delivery costs and identifies ways to improve efficiency and profitability. The cost varies from $75 to $250 per hour, depending on your business type, size, and cost structure.

International Accounting Service: This service addresses accounting issues and regulations in different countries or regions where you do business. International accounting navigates the challenges and opportunities of cross-border business, such as currency exchange, tax treaties, transfer pricing, and reporting standards. You can expect to pay between $200 and $500 per hour for this service, depending on the complexity of your foreign operations.

Accounting services vary widely in scope, value, and price. The best way to determine the cost of accounting services for your small business is to get quotes from various providers and compare them based on their qualifications, experience, reputation, and customer service. Considering the average monthly costs of these services can provide a clearer financial picture and assist in making more strategic decisions for your business.

But don't just focus on the price tag. Investing in quality accounting services is crucial for your small business.

Don't skimp on your accountant. A good accountant is worth every penny, helping you save on taxes, avoid penalties, improve cash flow, and grow your business. They are your partner, not an expense.

What Do Other Small Businesses Pay for Accounting Services?

The answer is that it depends. Many factors affect the cost of accounting services, such as the type and size of your business, the number and complexity of your transactions, the skill and experience of the accountant, and their billing method, whether hourly or per service.

According to some sources, the average cost of accounting services for small businesses is between $1,000 and $5,000 per year or between $146 and $457 per service. But these are just averages, and your business's actual cost may differ depending on your needs and situation.

Accounting is an essential part of running a successful small business. However, it need not be excessively costly. Following these tips, you can find an accountant that suits your needs and budget.

What Makes Accounting Services More or Less Expensive? Here Are the Factors You Should Know

The type and size of your business determine the accounting needs. Here is a list of factors that affect accounting costs:

The type and size of your business

The number and complexity of your transactions

The skill and experience of the accountant

The pricing model they use determines how they charge you for their services. There are two main pricing models: hourly and fixed.

In hourly pricing, an accountant charges you by hour for their services. This rate may vary depending on market demand and supply.

Fixed pricing means an accountant charges you a flat fee for a specific service or a package of services, which may give you more certainty and transparency.

How Do You Pay Your Accountant? By the Hour or by Services Provided?

It is a question that many small business owners face when they hire an accounting professional. Both options have pros and cons, depending on your situation.

If you pay by the hour, you pay for your accountant's actual time on your books. Having simple and predictable transactions or needing occasional or one-time services can be good.

However, it can also be risky if you have complex and variable transactions or need ongoing or comprehensive services. You may end up paying more than expected or receiving less value than deserved.

If you pay by the service, you pay a flat fee for a specific service or a package of services. Having complex and variable transactions or needing ongoing or comprehensive services can be good. This approach offers more cost certainty and transparency and incentivizes your accountant to work efficiently and effectively.

However, it can also be tricky if you have simple and predictable transactions or need occasional or one-time services. You may pay more than you need or get less flexibility than you want.

The choice between paying by the hour or by the service depends on several factors, such as the type and size of your business, the scope and scale of your accounting needs, your budget and preferences, and the benefits and challenges of each pricing model. You should weigh these factors carefully and communicate with your accountant before signing a contract.

Remember, it’s not just about the price but the value your accountant can bring to your business.

CPA vs. Bookkeeper Costs

When it comes to managing the accounting cost of a small business, it's crucial to understand the roles and costs associated with Certified Public Accountants (CPAs) and bookkeepers. Both professionals offer valuable services, but their responsibilities and pricing structures may differ. Let’s find out!

Feature | CPA (Certified Public Accountant) | Bookkeeper |

Role |

|

|

Expertise |

|

|

Services |

|

|

Costs |

|

|

Best for Scenarios |

|

|

Value to Small Business |

|

|

CPA or Bookkeeper: Which is Right for Your Business?

The choice between a CPA and a bookkeeper depends on your business needs. A bookkeeper is sufficient and cost-effective for daily financial record-keeping, transaction management, and basic financial reporting. However, for tax strategy, complex financial planning, audits, or if your business is in a highly regulated industry, the expertise of a CPA can be invaluable.

How Do You Negotiate Your Accounting Fees Like a Pro?

Accounting can be expensive. How can you get the best value for your money when hiring an accountant or an accounting firm? Here are some tips to help you negotiate your accounting fees like a pro.

First, do your homework. Know the going rates for accounting services you need. Use sites that offer information on accounting services, like Thumbtack or Forbes, to shop around and read reviews. This way, you can bargain better and find ways to cut costs or get more value.

Second, be upfront and polite. Tell your accountant what you want and need from them. Ask them how they price their services and what affects their rates. Show them why their services matter and recognize their challenges and risks. Be transparent and honest to avoid misunderstandings.

Third, be flexible and creative. Consider the cost, quality, and scope of work involved. Find intelligent ways to save money or add value for both sides. For example, you can sign a long-term deal or pay in advance for a lower fee. You can also mix and match services or change the frequency or difficulty of the tasks. Be creative and find win-win solutions.

Fourth, build a good and productive relationship with your accountant by listening, asking questions, addressing concerns, offering feedback, and expressing gratitude. Show them that you respect and value their skills and partnership. It will lead to better results, referrals, and repeat business.

Following these tips, you can negotiate your accounting fees like a pro and get the best accounting services for your budget and goals.

Accounting Tasks for Small Business Owners

How Do You Do Your Accounting Tasks Every Day?

As a small business owner, you manage several daily accounting tasks. Here’s what you should be doing:

Update your financial data. Sync your bank and credit card feeds and sales data to your accounting system. It will help you track your money in real-time.

Reconcile your cash and receipts. Reconcile your cash and check payments against your sales records. It will help you catch and fix any errors or mismatches and keep your records accurate and compliant.

Review and reconcile your transactions. Reconcile your bank statement's deposits and withdrawals with your accounting records. It will help you catch and fix any errors or mismatches and ensure your records match your bank records.

Record and categorize your expenses. Categorize and record all outgoing transactions in the appropriate accounts within your accounting system, such as cost of goods sold, rent, utilities, payroll, etc. It will help you track your expenses and profits.

Deposit your cash and checks. Deposit all cash and check payments into your checking account. It will help you improve your cash flow and reduce the risk of loss or theft of money.

These daily accounting tasks allow you to manage your finances better and avoid problems later.

Why Do You Need to Keep Your Financial Records Accurate?

If you’re a small business owner, you must keep your financial records accurate for many reasons. Here are some of them:

You can track your money. You can see how much you make, spend, own, owe, and keep. You can evaluate your business performance and position.

You can plan your budget. You can estimate how much money you need and have for a given period. You can allocate resources, control costs, avoid cash problems, and find opportunities.

You can make informed decisions. You can use your financial data and analysis to support your choices and actions for your business. You can improve your performance, competitiveness, and customer satisfaction.

You can comply with tax regulations. You can prepare and file your tax returns, pay your taxes, and solve any tax issues for your business. You can avoid penalties, audits, and legal troubles.

You can access loans and grants. You can apply for external funding from banks or institutions for your business. You can overcome financial challenges, expand your operations, or pursue new projects.

By keeping your financial records accurate, you can manage your finances better and avoid problems later.

Why You Should Use Accounting Software for Your Business?

According to a study by Clutch, nearly half of the small businesses surveyed (45%) didn’t have an accountant or a bookkeeper on their payroll. And more than 60% of them use accounting software, which helps them with accuracy, efficiency, and compliance (source: G2).

Here’s why smart business owners use accounting software:

You can save time and money by automating your accounting tasks, such as creating entries, statements, reports, payroll, and expenses.

You can reduce errors. You can collect, record, manage, and share your accounting data from one platform. You can ensure the accuracy and reliability of your records.

You can generate reports. You can create and pull financial reports such as profit and loss, balance sheet, cash flow, etc. You can track and measure your business performance and position.

You can streamline tax filing. You can prepare and file your tax returns, plan your tax strategies, and solve your tax issues. You can comply with tax regulations and avoid penalties and audits.

You can organize your records. You can keep copies of all your receipts, invoices, bills, transactions, etc., for tax purposes and reference. You can ensure the accuracy and compliance of your records.

You can share financial information. You can provide financial information and advice to internal or external users such as managers, owners, investors, creditors, regulators, or the public.

You can access data from anywhere. You can use cloud-based accounting software that connects to a central server or database. You can access your data from any device or location.

Using accounting software for your business can help you manage your finances better and avoid problems later.

Outsource or Hire? How do you choose the best accounting option for your business?

You must decide how to handle your accounting tasks if you're a small business owner. You have two options: outsource or hire. Outsourcing means paying an outside firm to do your accounting for you. Hire means employing an accountant who works for your business. Both options have pros and cons.

37% of small businesses outsource their accounting tasks, and 22% employ full-time or part-time outsourced accountants (Source: Clutch).

Options | Pros | Cons |

Outsource |

|

|

Hire |

|

|

You can choose the best accounting option for your business by comparing these pros and cons.

Certified Public Accountants and Bookkeeping Services

What Can a CPA Do For Your Business?

As a small business owner, you already have plenty on your plate without the added stress of managing your financial and tax matters. That's where a certified public accountant (CPA) can make a difference. A CPA can assist you with

Tackling your taxes: A CPA can take care of your tax returns, payments, and any issues that may arise, saving you from headaches, fines, and potential legal issues.

Securing loans and grants: A CPA can guide you in obtaining external funding from lenders or agencies, helping you address cash flow challenges, expand your operations, or kick-start new projects.

Providing financial insights and management reporting: A CPA can offer valuable financial insights and help you with management reporting, ensuring you make informed decisions and stay on top of your business's financial health.

Why Is It Worthwhile to Hire a CPA for Your Business?

Engaging a CPA is more than just an expense; it's a valuable investment in your business. A CPA can:

Conserve your time and resources: Using technology and tools, a CPA can efficiently manage, report, organize, and share your financial data with stakeholders, saving time and money.

Minimize errors and reduce risks: A CPA can enhance the accuracy of your records while adhering to the rules and standards of the accounting profession, reducing potential risks for your business.

Why Do You Need Bookkeeping Services for Your Small Business?

Bookkeeping services can save you time and money by handling your financial transactions, such as recording, reconciling, reporting, invoicing, and payroll. They can also help you with tax compliance, budget planning, decision-making, and profit and cash flow tracking.

Bookkeeping services can save you time and money using technology and tools to automate and streamline your bookkeeping processes. They can also reduce your errors and risks by ensuring the accuracy and reliability of your records. They can also follow the rules and standards of the profession.

You can choose from different bookkeeping professionals and methods (single-entry or double-entry) depending on your needs and preferences. Bookkeeping services can give you peace of mind and a clear picture of your finances.

One of the benefits of bookkeeping services is that they can provide you with financial statements. These reports tell you where your money is coming from and going.

How Financial Statements Can Help Your Small Business?

You need to know where your money is coming from and going to. That’s why you need financial statements. They are reports that tell you:

Your assets and liabilities (balance sheet)

Your income and expenses (income statement)

Your cash inflows and outflows (cash flow statement)

Your equity and changes over time (statement of changes in equity)

Financial statements can help you with

Filing your taxes and following the law

Planning your budget and setting your goals

Making smart decisions and improving your finances

Showing your results and getting more funding

You should make sure your financial statements are:

Prepared according to the rules and standards (GAAP)

Reviewed by a professional and trusted accountant (CPA)

Updated with any significant changes or events that happen after the end of the period

How Do You Save Money on Accounting for Your Small Business?

Accounting is essential if you want to keep your finances in order. But you don’t want to spend a fortune on accounting. That’s why you need to find the best accounting solution for your business that is efficient and meets all your requirements.

You have three options: hire an accountant, outsource your accounting tasks, or use accounting software.

Each option has a different accounting cost for small businesses; you must compare them carefully. You need reliable, accurate, and timely financial information to help you pay taxes, plan your budget, make intelligent decisions, and grow your business.

Are you looking to save on accounting costs for your small business? Then, take a look at SaasAnt Transactions a perfect automated solution to keep track of your finances. SaasAnt streamlines your bookkeeping by automating processes and seamlessly integrating QuickBooks Online, Xero with various payment and e-commerce platforms.

If you want to learn more about finding marginal cost, check out this guide how to find marginal Cost.

FAQs

What accounting is needed for a small business?

Small businesses typically need basic accounting to track income, expenses, assets, and liabilities. It includes bookkeeping (recording financial transactions), preparing financial statements (balance sheet, income statement, cash flow statement), tax planning and compliance, and payroll management.

How much will bookkeeping and accounting cost for my small business?

The cost of bookkeeping and accounting for a small business can vary widely depending on factors such as the company's size, the complexity of its transactions, the industry, and the level of service required.

What is the role of accounting in small businesses?

Accounting plays a critical role in small businesses by systematically recording financial transactions, tracking income and expenses, assessing financial health, and making strategic decisions. It helps business owners understand their profitability, manage cash flow, comply with legal and tax obligations, and plan for growth.

What is the definition of accounting costs, for example?

Accounting costs quantify the financial implications of undertaking an activity. These are the direct expenses associated with the operations of a business. For example, if a company pays $1,000 for rent, $500 for utilities, and $2,000 in salaries in a month, the total accounting cost for that month would be $3,500. These costs are easily identifiable, measurable, and recorded in the business's financial statements.