Classified Balance Sheet: A Complete Guide

A classified balance sheet is a critical financial document that segments a company’s assets, liabilities, and equity into specific categories, providing a clear and detailed view of its financial health. This structured approach enhances the clarity and comprehensiveness of financial statements, making it easier for stakeholders to analyze the company’s financial position. By organizing financial data into current and long-term classifications, a classified balance sheet aids in assessing liquidity, solvency, and overall financial stability, essential for effective decision-making and strategic planning in business.

Contents

What is a Classified Balance Sheet?

Importance of a Classified Balance Sheet

How to Prepare a Classified Balance Sheet?

Classified Balance Sheet Example

Benefits of Using a Classified Balance Sheet

Conclusion

FAQs

What is a Classified Balance Sheet?

A classified balance sheet organizes financial information into specific sections, providing a clearer and more detailed view of a company’s financial health. This structured format divides assets, liabilities, and equity into current and long-term categories, enhancing the analysis and understanding of the company's financial position. By categorizing these elements, a classified balance sheet helps stakeholders assess liquidity, solvency, and overall financial stability, facilitating better decision-making and strategic planning.

Components of a Classified Balance Sheet

Current Assets

Current assets are expected to be converted to cash or used up within one year. They are crucial for managing day-to-day operations and ensuring liquidity. Examples include:

Cash and Cash Equivalents: Highly liquid assets like bank balances and short-term investments.

Accounts Receivable: Money owed by customers for goods or services provided.

Inventory: Goods available for sale or production.

Prepaid Expenses: Payments made in advance for services or goods to be received in the future.

Long-Term Assets

Long-term assets are expected to provide value beyond one year, supporting long-term operational efficiency and growth. Examples include:

Property, Plant, and Equipment (PP&E): Tangible assets like buildings, machinery, and equipment.

Intangible Assets: Non-physical assets such as patents, trademarks, and goodwill.

Long-term Investments are intended to be held for more than one year.

Current Liabilities

Current liabilities must be settled within one year, which is crucial for assessing short-term financial health. Examples include:

Accounts Payable: Money owed to suppliers for goods or services received.

Short-term Loans: Borrowings that need to be repaid within a year.

Accrued Expenses: Expenses that have been incurred but have yet to be paid.

Long-Term Liabilities

Long-term liabilities are obligations due after one year, essential for understanding long-term financial commitments. Examples include:

Long-term Debt: Loans and financial obligations due beyond one year.

Bonds Payable: Long-term debt securities issued to investors.

Deferred Tax Liabilities: Taxes that are assessed or due for payment at a future date.

Shareholders’ Equity

Shareholders’ equity represents the owners' residual interest in the company after settling all liabilities. It is a crucial indicator of the company's net worth. Components include:

Common Stock: Equity capital raised through the issuance of shares.

Retained Earnings: Cumulative net income retained in the business rather than distributed as dividends.

Additional Paid-in Capital: Amounts received from shareholders above the stock's par value.

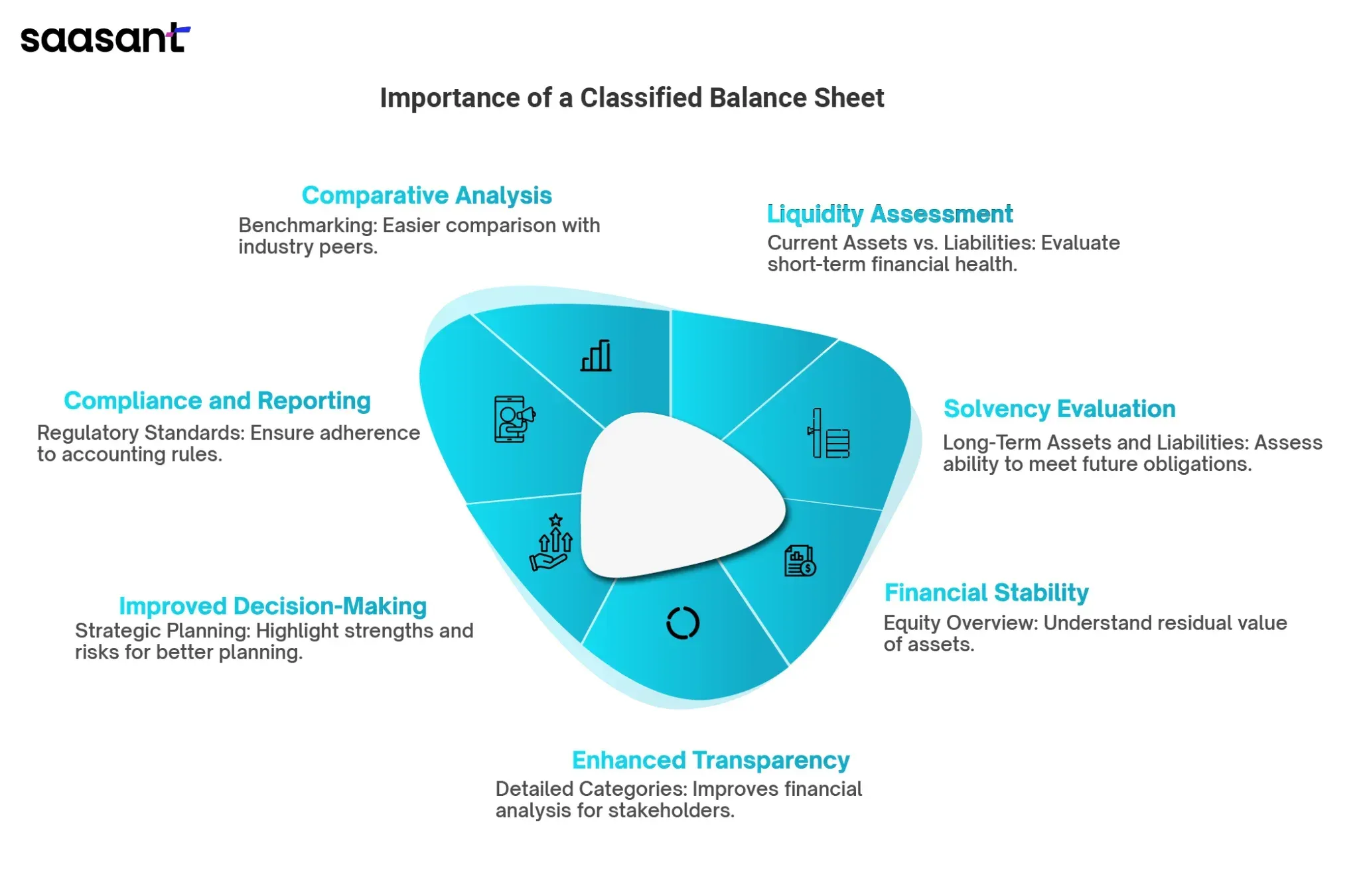

Importance of a Classified Balance Sheet

Classified balance sheets are essential for providing a clear and organized presentation of a company’s financial position. By categorizing assets, liabilities, and equity into distinct sections, they offer several key benefits:

Assessment of Liquidity:

Current Assets vs. Current Liabilities: Stakeholders can easily see whether the company has enough short-term assets to cover its short-term liabilities, aiding in evaluating liquidity.

Evaluation of Solvency:

Long-Term Assets and Liabilities: Separating long-term obligations and resources makes it easier to assess the company’s long-term financial health and ability to meet future obligations.

Financial Stability Analysis:

Equity Overview: By clearly presenting shareholders' equity, stakeholders can understand the residual value of the company’s assets after settling liabilities, which is crucial for evaluating financial stability.

Enhanced Transparency:

Detailed Categories: This format provides detailed information, enhancing transparency and making it easier for investors, creditors, and management to perform financial analysis.

Improved Decision-Making:

Strategic Planning: Accurate categorization and clarity enable better strategic planning and decision-making by highlighting the company’s strengths and potential risks.

Compliance and Reporting:

Regulatory Standards: A classified balance sheet helps ensure compliance with accounting standards and regulatory requirements, providing a reliable basis for financial reporting.

Comparative Analysis:

Benchmarking: The structured format allows for easier comparison with other companies, facilitating benchmarking and industry analysis.

How to Prepare a Classified Balance Sheet?

Gathering Financial Information:

Collect Data: Gather all necessary financial data from your accounting records. This includes information about assets, liabilities, and equity accounts.

Verify Accuracy: Cross-reference the data with supporting documents such as invoices, bank statements, and financial statements to ensure its accuracy and completeness.

Organizing Assets and Liabilities:

Current Assets: Categorize assets expected to be converted to cash or used up within one year. Examples include cash, accounts receivable, inventory, and prepaid expenses.

Long-Term Assets: Classify assets that provide value beyond one year, such as property, plant, and equipment (PP&E), intangible assets, and long-term investments.

Current Liabilities: Identify liabilities due within one year, including accounts payable, short-term loans, and accrued expenses.

Long-Term Liabilities: Group liabilities due after one year, such as long-term debt and deferred tax liabilities.

Creating the Balance Sheet:

List Current Assets: Itemize all current assets and calculate their total.

List Long-Term Assets: Itemize all long-term assets and calculate their total.

Total Assets: Sum the current and long-term assets totals to obtain the total assets.

List Current Liabilities: Itemize all current liabilities and calculate their total.

List Long-Term Liabilities: Itemize all long-term liabilities and calculate their total.

Total Liabilities: Sum the current and long-term liabilities totals to obtain the total liabilities.

Calculate Shareholders’ Equity: Include common stock, retained earnings, and additional paid-in capital.

Ensure Balance: Verify that total assets equal the sum of total liabilities and shareholders’ equity. This ensures that the balance sheet is balanced.

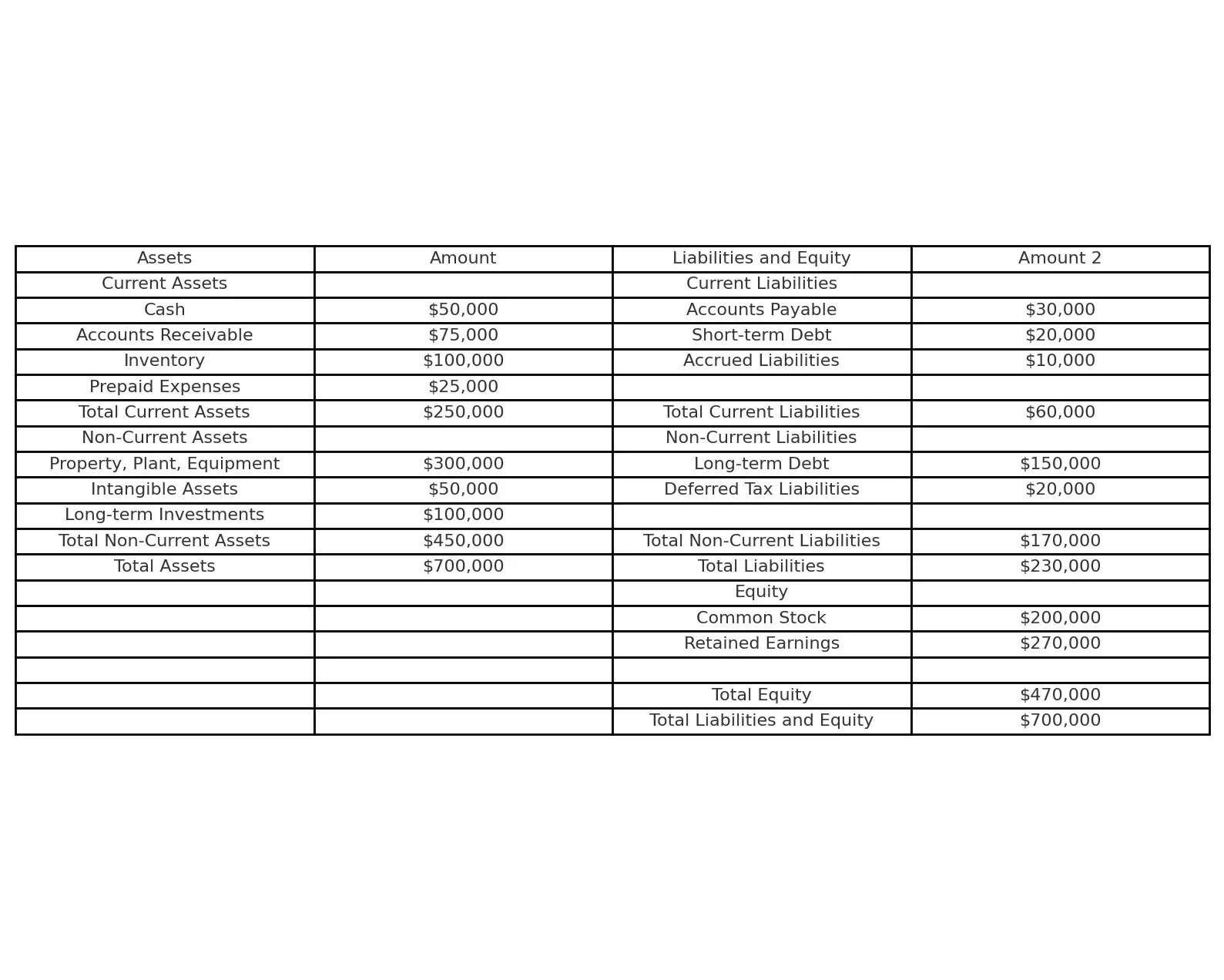

Classified Balance Sheet Example

Benefits of Using a Classified Balance Sheet

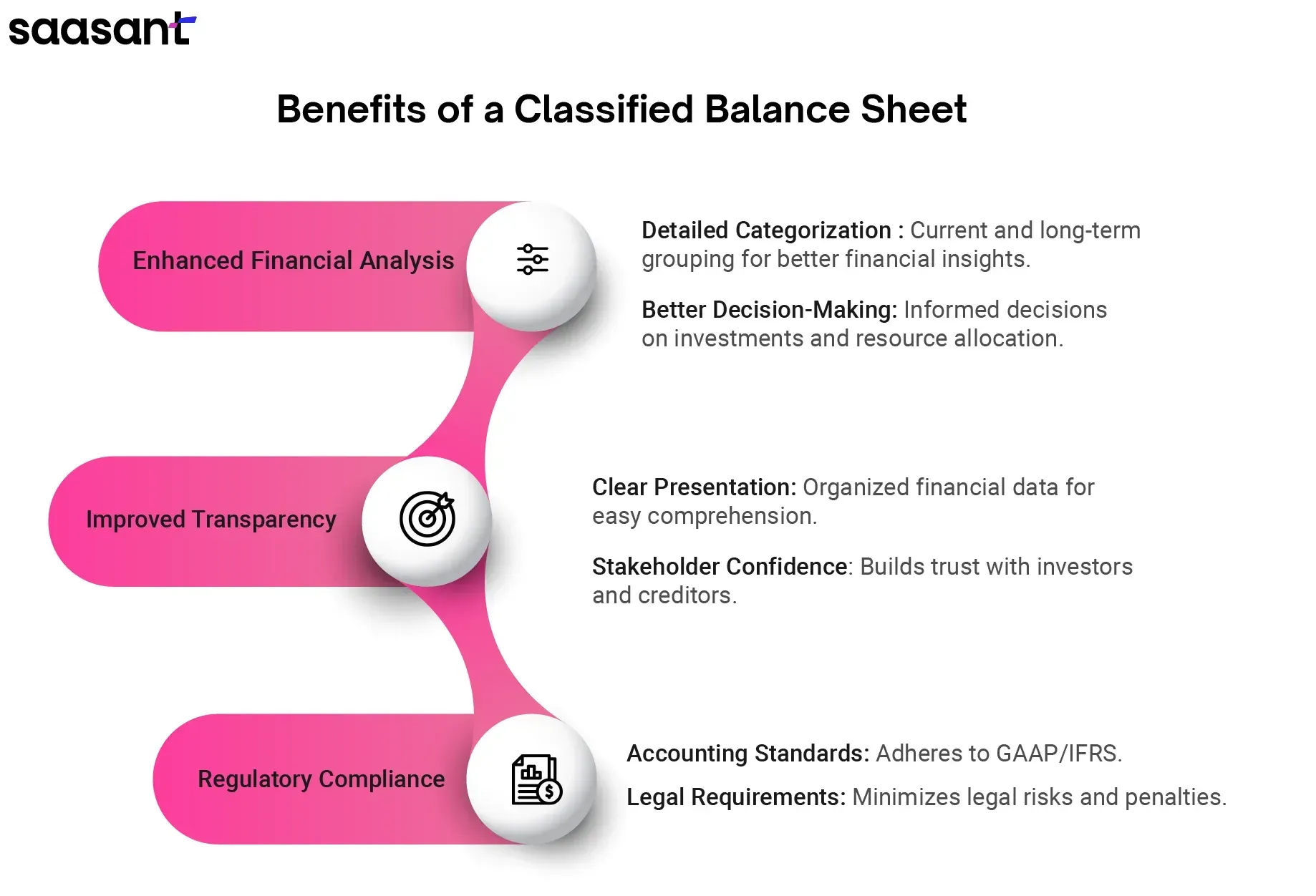

Benefits of Using a Classified Balance Sheet

Enhanced Financial Analysis

Detailed Categorization: A classified balance sheet groups assets and liabilities into current and long-term categories, providing a more nuanced understanding of the company’s financial health.

Better Decision-Making: This detailed view helps stakeholders make informed decisions regarding investments, resource allocation, and strategic planning.

Improved Transparency

Clear Presentation: A classified balance sheet's structured format presents financial data in a clear and organized manner, making it easier for stakeholders to comprehend the company’s financial position.

Stakeholder Confidence: Enhanced transparency fosters trust and confidence among investors, creditors, and other stakeholders, leading to stronger business relationships.

Regulatory Compliance

Accounting Standards: A classified balance sheet ensures that financial reporting adheres to generally accepted accounting principles (GAAP) or international financial reporting standards (IFRS).

Legal Requirements: Compliance with regulatory requirements reduces the risk of legal issues and penalties, ensuring the company operates within the law.

Common Mistakes to Avoid

Incorrect Classification:

Misclassifying Assets and Liabilities: One of the most common errors is incorrectly classifying assets and liabilities. For example, placing a long-term asset under current assets or vice versa can significantly distort the financial statements.

Impact on Financial Analysis: Misclassification leads to inaccurate ratios and metrics, such as the current and quick ratios, which can mislead stakeholders about the company’s liquidity and financial health.

Preventive Measures: Ensure proper training for accounting staff on classification criteria and regularly review classifications to maintain accuracy.

Omitting Information:

Incomplete Data: Please include all relevant financial information to ensure an accurate balance sheet. Omitting accrued expenses or unrecorded liabilities can skew the company’s financial position.

Comprehensive Reporting: To provide an accurate and fair view of the company’s financial health, ensure that all assets, liabilities, and equity items are recorded. This includes obvious items like cash and payables and less apparent ones like prepaid expenses, deferred revenue, and contingent liabilities.

Audit and Review: Implement regular audits and reviews to ensure all financial data is captured and accurately reported. This can involve cross-checking with other financial statements, bank reconciliations, and external confirmations.

Neglecting Updates:

Outdated Information: A balance sheet that is not regularly updated can quickly become obsolete and irrelevant. Financial decisions based on stale data can lead to significant errors and missed opportunities.

Reflecting Current Status: Regularly updating the balance sheet ensures it reflects the company's current financial status, incorporating the latest transactions, adjustments, and events that impact the financial position.

Scheduled Reviews: Establish a routine for updating the balance sheet, such as monthly or quarterly reviews. This practice ensures timely and accurate financial reporting, aiding in better decision-making and strategic planning.

Conclusion

Understanding and implementing a classified balance sheet is crucial for accurate financial reporting. It organizes a company's assets, liabilities, and equity into distinct categories, offering a clear view of its financial position. Separating these elements into current and long-term categories enhances clarity and comprehensiveness, aiding stakeholders in assessing liquidity, solvency, and overall financial stability. This structured format supports better decision-making and strategic planning while ensuring compliance with accounting standards like GAAP or IFRS. Enhanced transparency fosters trust among investors, creditors, and regulators, and effective communication of financial status aids in securing support. Regular updates streamline financial management, enabling proactive planning and operational efficiency, making it essential for maintaining financial health.

FAQs

What is a classified balance sheet?

A classified balance sheet organizes assets, liabilities, and equity into specific categories for clarity and detailed financial analysis.

How are deferred tax assets and liabilities classified on the balance sheet?

Deferred tax assets and liabilities are classified as non-current on the balance sheet.

Which assets of a classified balance sheet usually include the subgroups?

Current and non-current assets usually include cash, accounts receivable, inventory, property, plant, and equipment subgroups.

What is the difference between a consolidated and classified balance sheet?

A consolidated balance sheet combines the financials of parent and subsidiary companies, while a classified balance sheet organizes items into specific categories.

How often should a classified balance sheet be prepared?

A classified balance sheet should be prepared regularly, typically at the end of each accounting period (monthly, quarterly, or annually).

What does a classified balance sheet differ from?

A classified balance sheet differs from an unclassified balance sheet by organizing items into categories, and providing more detailed financial information.

Can small businesses use classified balance sheets?

Yes, small businesses can and should use classified balance sheets for better financial management and reporting.

How does a classified balance sheet improve financial reporting?

It improves financial reporting by providing a clear and detailed view of a company's financial position, aiding in analysis and decision-making.