How to Implement Accounting Automation? 5 Easy Steps

Accounting automation is necessary for streamlining business operations, reducing errors, and freeing up valuable time. Implementing automation in your accounting workflows can transform how you manage your financial data.

This blog will further explain the five easy steps to implement accounting automation. These steps will help you reduce manual tasks, improve accuracy, and gain deeper insights into your financial health.

Contents

What Is Accounting Automation?

How Does Accounting Automation Work?

Benefits of Accounting Automation

5 Steps to Implement Accounting Automation

Accounting Tasks Businesses Can Automate

Conclusion

FAQs

What Is Accounting Automation?

Accounting automation uses software to automatically perform traditional accounting tasks like invoicing, ledger management, reconciliation, payroll, and reporting. This software minimizes the need for manual entry, helping you save time and reduce errors.

With automation, financial data flows seamlessly between system tasks. Entry and calculation tasks are done automatically, and reports are generated quickly and accurately. This boosts efficiency and gives businesses real-time insights into their financial status, helping them make better decisions.

How Does Accounting Automation Work?

Automation allows businesses to concentrate on identifying and correcting errors instead of performing manual tasks. Accounting software collaborates with accountants to streamline their work. Once automated, accounting tasks can scan and analyze data much more rapidly than humans can, and updates to the numbers are made more swiftly as the software connects directly with expense management systems.

Platforms like QuickBooks/Xero can integrate with your expense management system or even directly with your company’s bank account. As a result, every transaction is automatically recorded in the books in real-time rather than being batched weekly, bi-weekly, or monthly. To understand how to implement accounting automation, you must also understand its benefits.

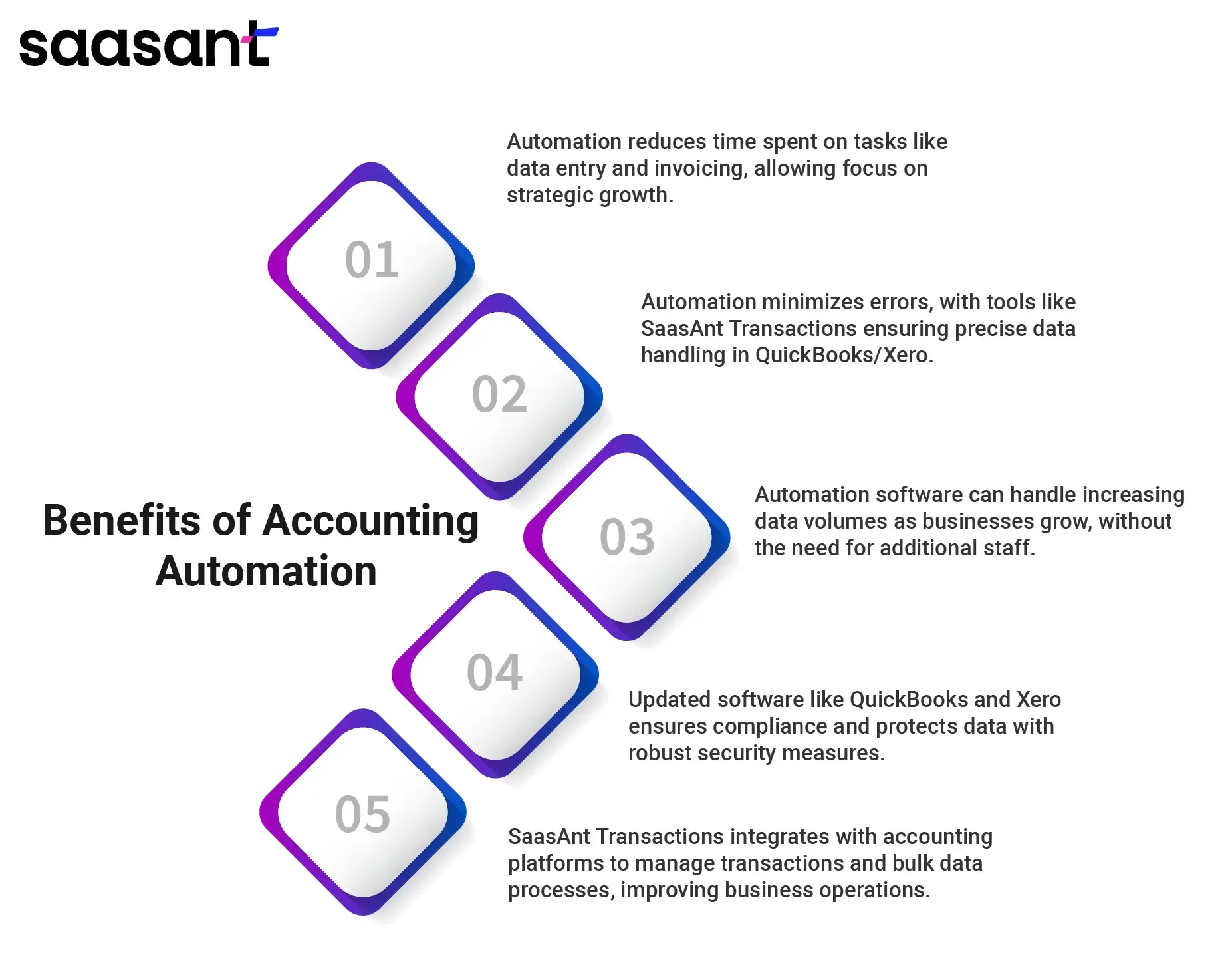

Benefits of Accounting Automation

Accounting automation is changing the way businesses handle their finances. By replacing traditional, manual accounting processes with automated applications, companies can enjoy many benefits that streamline financial operations and enhance overall business performance. Have a look at the benefits of accounting automation:

Enhanced Efficiency and Time Savings

Accounting automation significantly reduces the time spent on manual bookkeeping and data entry tasks. By automating repetitive tasks such as data entry, invoicing, and reconciliations, businesses can allocate more time to strategic activities that drive growth and profitability.

Improved Accuracy

Manual data handling is prone to errors, leading to costly discrepancies. Automation reduces the risk of human error by ensuring that transactions are recorded accurately and consistently. SaasAnt Transactions enhances this accuracy by enabling seamless bulk imports and exports of data into QuickBooks/Xero, ensuring that large volumes of data are handled correctly with no manual errors.

Scalability

As businesses grow, their financial data becomes more complex and voluminous. Accounting automation software easily handles the transactions without requiring proportional increases in accounting staff. This scalability is crucial for growing businesses that need to efficiently manage more significant amounts of data.

Enhanced Compliance and Security

Accounting software like QuickBooks and Xero are updated regularly to comply with the latest tax laws and financial regulations, reducing the risk of compliance issues. Furthermore, automated systems typically include robust security measures to protect sensitive financial data from unauthorized access and breaches.

Streamlined Workflows with Integrated Solutions

PaytraQer, for instance, helps you connect and sync your payment platforms with QuickBooks/Xero. With PayTraQer, you can easily sync your e-commerce and payment gateway transactions with QuickBooks or Xero for precise, real-time updates. This can eliminate manual data entry and enhance efficiency.

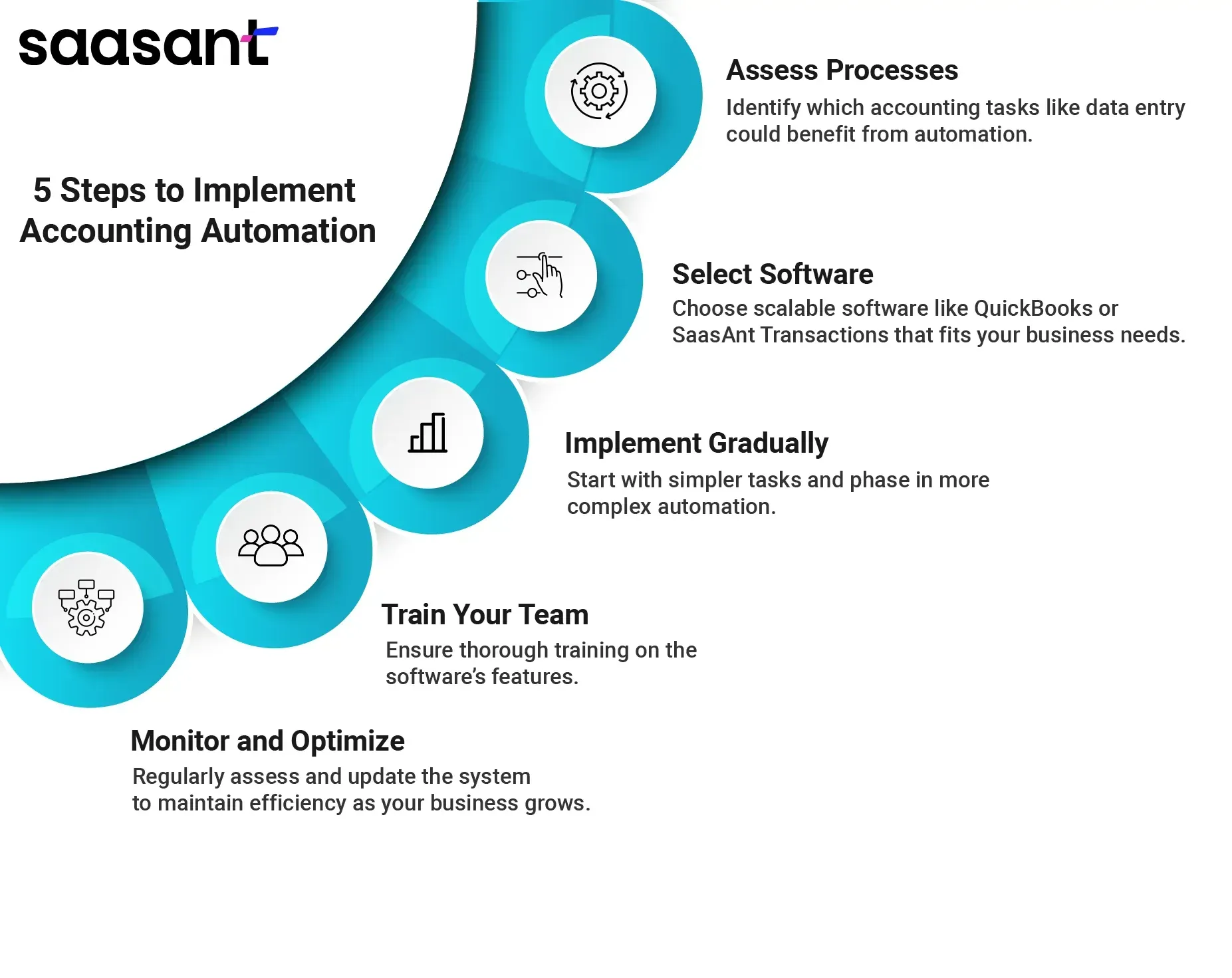

5 Steps to Implement Accounting Automation

Implementing accounting automation can streamline your financial operations, improve accuracy, and save time. Here are five key steps to effectively set up accounting automation:

Step 1: Assess Your Current Accounting Processes

Begin by conducting a thorough review of your existing accounting workflows. Identify which tasks are repetitive and time-consuming, such as data entry, invoicing, payroll, and financial reporting. Understanding where problems occur and where errors are most common can help pinpoint what processes will benefit most from automation. This assessment will serve as the foundation for identifying which automation tools and software will best suit your needs.

Step 2: Choose the Right Accounting Automation Software

The right accounting automation software is essential for effectively maintaining your financial processes. Choosing tools that integrate well with your existing systems and can scale alongside your business's growth is crucial. Popular options like QuickBooks and Xero are widely recognized for their robust features that cater to various business needs, including transaction recording, payroll management, and financial reporting.

Step 3: Plan and Execute a Gradual Implementation

Transitioning to an automated system should be a gradual process. Start by automating simple tasks such as data entry or invoice processing to minimize disruptions to your operations. This approach allows you and your team to adapt to the new system without overwhelming them. Create a timeline for implementing different automation phases and ensure ample time for training and adjustments as needed.

Step 4: Train Your Team

Practical training is essential for a smooth transition. Ensure that your accounting team is well-versed in using the new software. Training should cover the basics of operation and how to use the advanced features of the automation software. Consider having ongoing training sessions and providing resources for troubleshooting to help your team become proficient and confident in using the new applications.

Step 5: Monitor and Optimize the System

After the initial implementation, continuously monitor the performance of your automated processes. Check for any issues or bottlenecks and collect feedback from users. Use this information to optimize the system. Regularly update the software to take advantage of new features and improvements. Additionally, as your business grows and changes, adjust the automation settings to align with new accounting needs and regulations.

Accounting Tasks Businesses Can Automate

Every business begins its journey from a unique starting point and adopts accounting automation at its own pace. Some businesses automate numerous processes simultaneously, while others prefer a more methodical approach, automating tasks one at a time based on priority. Below are seven accounting tasks that businesses can automate:

Accounts Payable (AP): Automation simplifies the entire payment process, enhances tracking of invoice due dates, ensures timely vendor payments, and reduces the risk of fraud by flagging suspicious invoices.

Accounts Receivable (AR): Automating AR improves cash flow management, increases invoice accuracy, and significantly cuts processing costs. Automation opportunities span from scheduling invoice dispatch to collecting overdue payments.

Expense Management: By automating expense management, businesses can track and categorize expenses without manual effort, ensuring that spending aligns with budgetary constraints.

Sales Tracking: Automation tools can track sales transactions in real-time, providing up-to-date insights on sales trends and customer behaviors. This facilitates more accurate forecasting and strategic planning.

Payroll: Manual payroll is time-consuming for growing companies with limited accounting resources. Automating payroll ensures timely employee payments and helps teams manage payroll documentation efficiently.

Month-end Financial Closes: The month-end close is critical yet stressful. Automation helps relieve the pressure on finance teams to close faster and more accurately, ensuring quality without the rush.

Procurement: Traditionally heavy on paperwork, automating procurement processes like purchase order management reduces time and costs without compromising process integrity or supplier relationships.

Expense Reports: Automation transforms the complex task of manual expense reporting. Employees can digitally submit expenses, streamlining the approval process and reducing paper usage.

Sales Order Process: Automation ensures a consistent and reliable sales order process, helping businesses meet customer expectations through timely and accurate order fulfillment.

Conclusion

Automating your accounting process is a strategic move that can improve your financial operations' efficiency, accuracy, and scalability. Following the five steps mentioned, you can transform your accounting workflow and focus more on strategic growth opportunities.

FAQs

What is automation in accounting?

Accounting automation uses software to handle tasks like data entry, reconciliation, and reporting, increasing efficiency and accuracy.

How do I automate my accounting job?

To automate your accounting job, identify repetitive tasks, select appropriate software like QuickBooks/Xero, implement the software, train thoroughly, and continuously refine the system to suit your business needs.

What types of accounting tasks will be automated?

Many accounting tasks are suitable for automation. The most commonly automated tasks include accounts payable, accounts receivable, payroll, and expense management.

Is accounting easy to automate?

Automated accounting faces several hurdles, such as complex software interfaces, lengthy training durations, technical glitches, difficulties in data migration, complex integrations, and compliance with regulations. While automation in accounting systems does not eliminate the need for human input, it does free up time from routine tasks, allowing focus on more valuable activities.

How can automation transform the accounting process?

Automation enhances accounting by speeding up data processing, reducing errors, and cutting operational costs. It allows real-time financial reporting and improves regulation compliance, freeing accountants to focus on strategic analysis and decision-making.