Is Accounts Payable a Debit or Credit? Understanding AP in Accounting

Understanding whether accounts payable are recorded as a debit or a credit is essential for accurate financial documentation. Usually, when a company receives an invoice, the accounts payable amount increases, and this transaction is recorded as a credit. Conversely, when a payment is made towards the debt, the accounts payable decrease, which is recorded as a debit.

Understanding whether accounts payable are recorded as a debit or a credit is essential for accurate financial documentation. Usually, when a company receives an invoice, the accounts payable amount increases, and this transaction is recorded as a credit. Conversely, when a payment is made towards the debt, the accounts payable decrease, which is recorded as a debit.

This straightforward debit and credit system helps businesses track their debts and payments effectively, ensuring that their financial statements accurately reflect their financial health. This blog will further explain accounts payable, debit, or credit.

Contents

What is Accounts Payable?

Is Accounts Payable a Debit or Credit?

Understanding Debits and Credits in Accounting

Common Scenarios Involving Accounts Payable

Best Practices for Managing Accounts Payable: Ensuring Efficient Accounting and Cash Flow Management

Conclusion

FAQ’s

What is Accounts Payable?

Accounts Payable (AP) is a term used in accounting to denote the money a company owes to its suppliers or vendors for goods or services it has received but has not yet paid for. These are typically short-term debts that are due within a year.

When a company orders goods or services, the supplier usually issues an invoice that details the amount owed. This invoice creates an account payable, a liability on the company's balance sheet. Accounts payable are crucial to managing a company's cash flow. By effectively managing AP, a company can maintain good relationships with suppliers through timely payments, take advantage of potential discounts for early payments, and effectively manage its working capital.

Is Accounts Payable a Debit or Credit?

In accounting, Accounts Payable (AP) is classified as a credit. This classification is based on the double-entry accounting system, where every transaction affects at least two accounts, with a debit entry in one account and a corresponding credit entry in another.

Accounts payable are a company's liability, representing money the company owes to its suppliers or vendors for services or goods received but not yet paid for. In the double-entry system, liabilities are increased by credits and decreased by debits. Therefore, when an invoice is recorded, the accounts payable account is credited, indicating an increase in the company’s obligations.

Credit Entry:

When a company receives an invoice from a supplier, the purchase is recorded as an increase in accounts payable (a credit) because it increases the company's losses.

Debit Entry:

On the other hand, debit entry depends on the nature of the purchase. For example, if the purchase is for inventory, the Inventory account would be debited. If it's for an expense, the relevant expense account (like Office Supplies or Utilities) would be debited.

Examples and Scenarios of Account Payables

Scenario 1: Purchasing Inventory on Credit

Company A orders $5,000 worth of inventory from Supplier B on credit.

Debit Inventory Account: $5,000 (increases assets)

Credit Accounts Payable: $5,000 (increases liabilities)

In this scenario, the debit entry increases the company’s inventory, reflecting the receipt of physical goods. The credit entry in accounts payable reflects that the company now owes this amount to the supplier.

Scenario 2: Receiving Services on Credit

Company C receives marketing services valued at $2,000 from Service Provider D, to be paid later.

Debit Marketing Expense: $2,000 (increases expense)

Credit Accounts Payable: $2,000 (increases liabilities)

This entry shows the company receiving a service and agreeing to pay later, thus increasing its liabilities through a credit to Accounts Payable and recording the cost as an expense through a debit.

Scenario 3: Payment of Accounts Payable

When Company A pays off the $5,000 owed to Supplier B.

Debit Accounts Payable: $5,000 (decreases liabilities)

Credit Cash or Bank Account: $5,000 (decreases assets)

This transaction reflects the debt payment, decreasing accounts payable through debit and reducing cash through credit, as cash leaves the company to settle the obligation.

Understanding Debits and Credits in Accounting

Understanding how debits and credits function helps maintain balanced financial records, ensuring that every transaction is accurately represented in financial statements.

What is a Debit?

In accounting, a debit is an entry recorded on the left side of an account ledger. It represents an increase in assets or expenses or a decrease in liabilities or equity.

Examples:

Assets: When a company purchases office equipment, the Equipment account (an asset) is debited to reflect the increase in the asset.

Expenses: Paying for utilities increases the Utilities Expense account, which is debited.

Liabilities: When paying off a portion of a loan, the Loan Payable account (a liability) is debited to show a decrease in the amount owed.

What is a Credit?

A credit is an entry recorded on the right side of an account ledger. It signifies an increase in liabilities, equity, or revenue or a decrease in assets or expenses.

Examples:

Liabilities: When a company takes out a loan, the Loan Payable account (a liability) is credited to show the increased amount owed.

Revenue: Recording sales revenue involves crediting the Sales Revenue account to reflect the increase in income.

Assets: When a company sells equipment, the Equipment account (an asset) is credited to reflect the asset decrease.

How Debits and Credits Affect Financial Statements?

Impact on the Balance Sheet:

Assets and Liabilities: Debits increase asset accounts and decrease liability accounts, while credits decrease asset accounts and increase liability accounts.

Equity: Credits generally increase equity accounts, such as retained earnings, whereas debits decrease them.

Impact on the Income Statement:

Revenue and Expenses: Credits increase revenue accounts, reflecting higher income. Conversely, debits increase expense accounts, representing higher costs.

Net Income: Total revenues (credits) and expenses (debits) determine the period's net income or loss.

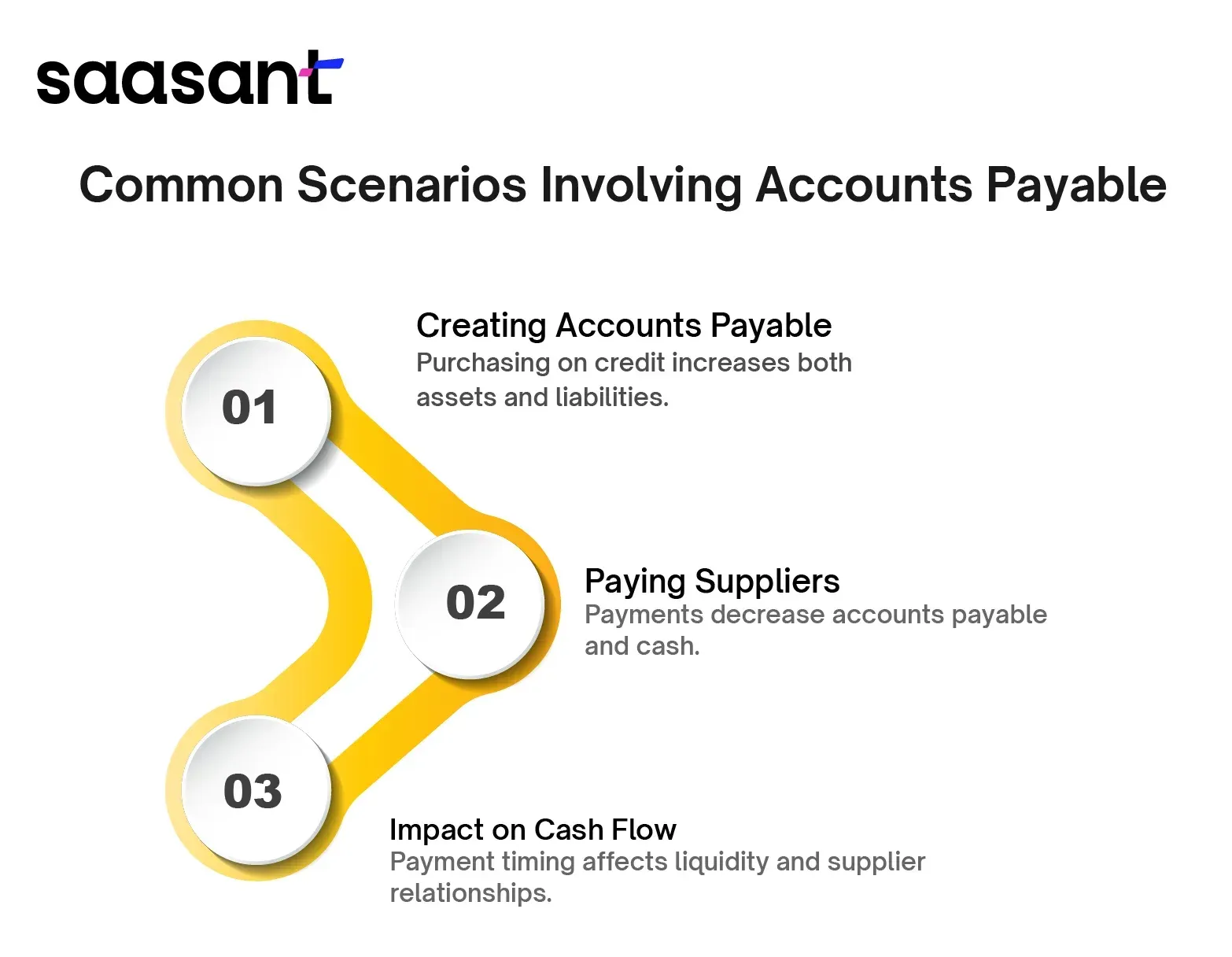

Common Scenarios Involving Accounts Payable

Understanding the below-given scenarios helps businesses manage their accounts payable effectively, balancing supplier relationships with cash flow needs.

How do Purchases on Credit Create Accounts Payable?

Scenario: When a company buys inventory or services from a supplier on credit, it agrees to pay the supplier later. This creates a liability, recorded as accounts payable.

Example: A business purchases $10,000 of office supplies but doesn't pay immediately. The company records the $10,000 increase in its inventory (asset) and an equivalent $10,000 increase in accounts payable (liability) on the balance sheet.

Accounting Entry:

Debit: Inventory or Office Supplies (asset) – $10,000

Credit: Accounts Payable (liability) – $10,000

Process of Paying Suppliers and Reducing Accounts Payable:

Scenario: When the company eventually pays the supplier, the payment reduces the amount owed, decreasing accounts payable and cash.

Example: The company pays the $10,000 owed to the supplier. This transaction decreases accounts payable and cash by the payment amount.

Accounting Entry:

Debit: Accounts Payable (liability) – $10,000

Credit: Cash or Bank Account (asset) – $10,000

Note:

Record Payment: Once payment is made, update the accounts payable ledger to reflect the reduction in liability.

Update Cash Account: Reduce the cash or bank account to reflect the outflow of funds.

Impact on Cash Flow

How Accounts Payable Affect a Business’s Cash Flow?

Delayed Payments: Extending the payment terms with suppliers (higher accounts payable) can improve short-term cash flow by keeping cash within the business longer. However, excessive delays might harm supplier relationships or result in penalties.

Payment Timing: Regularly paying off accounts payable on time ensures smoother operations and avoids late fees, but it requires careful cash flow management to avoid liquidity issues.

Cash Flow Statement: Accounts payable changes affect the cash flow statement under operating activities. An increase in accounts payable means cash is conserved, while a decrease signifies cash outflows for settling liabilities.

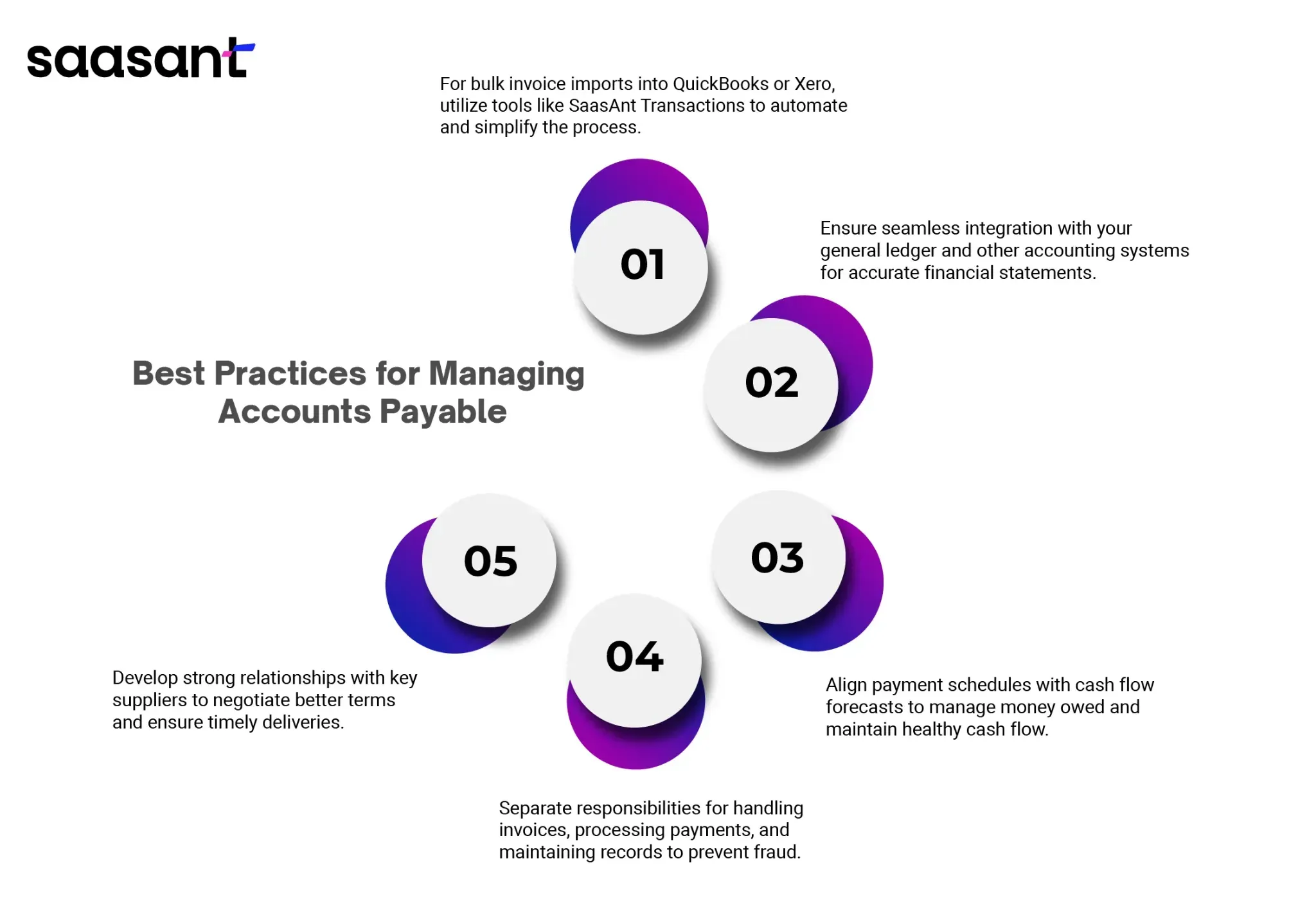

Best Practices for Managing Accounts Payable: Ensuring Efficient Accounting and Cash Flow Management

By following the below given best practices, you can ensure efficient account payable management, enhancing your company’s financial stability and operational efficiency.

1. Streamline Invoice Processing:

Use automated systems to handle invoices efficiently, reducing manual errors and speeding up the accounts payable workflow.

If you’re piled up with too many invoices and looking to import them into QuickBooks/Xero, you can use SaasAnt Transactions to speed up the process.

SaasAnt Transactions offers advanced features to automate bulk transactions, making managing and categorizing financial data easier.

2. Leverage Accounts Payable Automation:

Implement software to automate the import and categorization of bulk transactions.

Ensure seamless integration with your general ledger and other accounting systems for accurate financial statements.

3. Maintain Accurate Records and Monitor Cash Flow:

Regularly reconcile accounts payable with supplier statements to resolve discrepancies and ensure accuracy.

Align payment schedules with cash flow forecasts to manage money owed effectively and maintain healthy cash flow.

4. Establish Strong Internal Controls:

Separate responsibilities for handling invoices, processing payments, and maintaining records to prevent fraud.

Implement a multi-level approval process for large or unusual payments to ensure thorough oversight.

5. Negotiate and Build Relationships with Suppliers:

Secure favorable terms for services on credit and purchases of goods to optimize cash management.

Develop relationships with key suppliers to negotiate better terms and ensure timely deliveries.

6. Monitor Key Metrics:

Track the accounts payable turnover ratio to evaluate how quickly your company pays off its creditors.

Use this ratio to assess the efficiency of your accounts payable process and make necessary adjustments.

Conclusion

Accounts payable (AP) are recorded as a credit because they represent short-term liabilities owed to suppliers. This classification accurately reflects the company's obligations on the balance sheet. As a credit, AP indicates amounts owed to vendors, highlighting the company’s financial responsibilities. Effective AP management ensures healthy cash flow, strengthens supplier relationships, and maintains financial accuracy.

FAQ’s

Is Accounts Payable a Debit or Credit?

Accounts payable is classified as a credit on the balance sheet. This reflects the company's obligation to pay for goods or services received but not yet paid for.

What Type of Account is Accounts Payable?

Accounts payable is a liability account. It represents the amount a company owes its suppliers or vendors for products or services received on credit.

Is Accounts Payable Always a Credit?

Yes, accounts payable are always credits. They signify a liability that needs to be settled in the future.

Can Accounts Payable Ever Be a Debit?

Typically, accounts payable is never a debit. However, in rare cases, a debit entry may occur when an adjustment, such as a return or correction, reduces the amount owed.

How Does Accounts Payable Affect My Balance Sheet?

Accounts payable appear as a liability on the balance sheet, showing the total amount the company owes to creditors. It impacts the company's financial position and liquidity.

What Are the Best Practices for Managing Accounts Payable?

Use automated tools to handle invoices efficiently.

Implement software to manage bulk transactions and reduce manual errors.

Regularly reconcile accounts payable to ensure accuracy.

Separate duties and implement approval processes to prevent fraud.

Secure favorable terms and build strong relationships with vendors.

Read also

Can I Import Accounts Receivable Payments into QuickBooks Desktop?

Can I Import Accounts Receivable Payments into QuickBooks Online?

Accounts Receivable Aging Report: What It Is and How to Use It

How to Import Payments in QuickBooks Desktop?