14 Ways to Improve Small Business Cash Flow

Managing cash flow is crucial for the success and stability of any small business. Efficient small business cash flow management ensures you meet obligations, seize growth opportunities, and navigate economic uncertainties. This guide will provide practical strategies for managing cash flow effectively, from understanding the fundamentals to implementing best practices for maintaining a healthy cash flow.

Whether you want to improve your revenue, boost profit, or achieve positive cash flow, mastering small business cash flow can make all the difference. Dive in to learn how to keep your finances in check and your business thriving.

Contents

What Is Cash Flow?

14 Ways to Improve Cash Flow

Common Small Business Cash Flow Mistakes to Avoid

Wrapping Up

FAQ

What Is Cash Flow?

Cash flow is the movement of money in and out of a business, encompassing all incoming revenues and outgoing expenses. It reflects the company’s financial health and ability to manage operating costs, investments, and debts.

Positive cash flow indicates that a business has more money coming in than going out, which supports growth and stability. Conversely, negative cash flow, where expenses exceed revenues, poses a significant problem. It can lead to financial strain, hinder the ability to pay bills, invest in opportunities, and ultimately threaten the business's survival. Managing cash flow is essential to avoid these challenges and ensure long-term success.

14 Ways to Improve Cash Flow

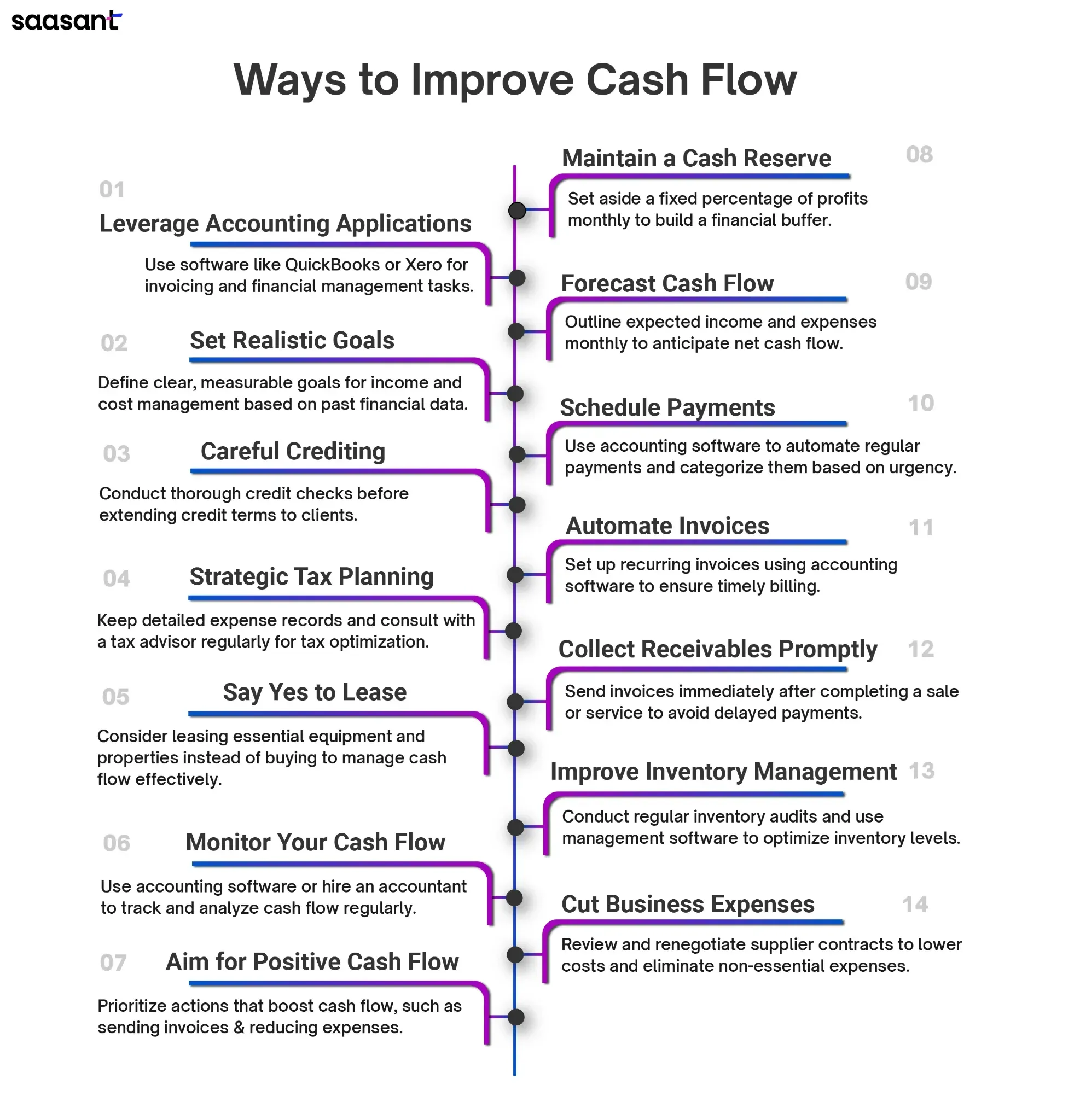

1. Maintain a Cash Reserve

A cash reserve is an emergency savings fund that acts as a financial buffer, ensuring your business can handle unexpected expenses without relying heavily on business credit. By setting aside a portion of your profits, you can safeguard your business against cash flow fluctuations and avoid the pitfalls of negative cash flow. This practice strengthens your financial stability and enhances overall company cash flow management.

Set aside a fixed percentage of monthly profits for your cash reserve.

Automate transfers to a dedicated savings account to ensure consistency.

Review and adjust your reserve goals quarterly based on business performance and needs.

2. Forecast Cash Flow

Forecasting expenses and earnings allow you to anticipate your net cash flow and identify your break-even point. This proactive approach helps you manage operational costs and plan for future financial needs. Accurately forecasting your cash flow ensures you can cover expenses, invest in growth opportunities, and maintain a healthy financial position, ultimately leading to better business stability and success. Additionally, it enables you to address potential cash flow problems before they escalate.

Outline expected income and expenses monthly.

Review and adjust your cash flow forecast weekly or bi-weekly.

Use historical financial data to predict future trends and identify patterns in earnings and expenses.

3. Set a Schedule for Payments

Setting a schedule for payments is vital to prevent cash flow issues. By promptly addressing accounts payable and categorizing payments based on urgency, you can ensure that payment due dates are met regularly. This proactive approach helps maintain smooth cash flow and avoids late fees or penalties. Managing payments reduces financial strain and contributes to overall business plan stability.

Use accounting software like QuickBooks or Xero to automate regular payments, ensuring they are made promptly and reducing the risk of missed deadlines.

Categorize payments based on urgency and due dates, focusing on high-priority bills first to avoid late fees and maintain good vendor relationships.

Schedule monthly reviews of your accounts payable to adjust payment schedules as needed, ensuring your cash flow remains stable and responsive to changes.

4. Automate Invoices

Automating invoices is a powerful strategy for improving small business cash flow management. Using accounting software to invoice customers automatically reduces the chances of delays and errors. This ensures timely billing, helping you stay on top of outstanding invoices. Streamlining this process saves time and enhances your small business cash flow by providing a steady inflow of payments.

Use accounting software like QuickBooks or Xero to set up recurring invoices for regular customers.

Enable automated payment reminders to notify clients of upcoming or overdue payments.

Integrate online payment options to make it easier for customers to pay promptly.

5. Collect Receivables Promptly

Delayed payments can lead to cash flow issues, hindering your ability to cover expenses. To avoid this, follow up on due receivables regularly and reduce outstanding receivables. Timely collection ensures steady sales revenue and strengthens overall small business cash flow management, helping your business remain financially stable with enough cash.

Send invoices immediately after a sale or service is completed.

Implement a systematic follow-up process for overdue payments.

Offer incentives for early payments, such as small discounts or benefits.

6. Cut Business Expenses

As a small business owner, you should identify ordinary expenses that exceed your business budget to improve cash flow and avoid potential cash flow problems. Focus on eliminating non-essential or redundant expenses. Streamline daily operating expenses by negotiating better rates with suppliers and reducing waste. Effective expense management ensures a healthier business cash flow, allowing you to allocate resources more efficiently and support growth.

Review and renegotiate supplier contracts to lower costs.

Switch to energy-efficient solutions to reduce utility bills.

Eliminate or downsize non-essential subscriptions and services.

7. Improve Inventory Management

Keep up-to-date records of purchased inventory and sold inventory to avoid idle inventory. Regularly monitor inventory levels to prevent understocking and overstocking. Efficient management ensures you only buy what’s needed, reducing excess costs and optimizing cash flow. This balanced approach supports small business cash flow's financial stability and operational efficiency.

Conduct regular inventory audits to maintain accurate, up-to-date records.

Use inventory management software to track purchased and sold inventory in real-time.

Implement a just-in-time (JIT) ordering system to minimize idle inventory and prevent overstocking.

8. Leverage Accounting Applications

Leveraging accounting software is an intelligent way to manage cash flow for small businesses. You can automate many financial tasks using applications such as QuickBooks and Xero. These platforms help track expenses invoicing and manage accounts payable and receivable. Specifically, SaasAnt Transactions allows bulk import and export of financial data, saving time and reducing errors. By streamlining these processes, small business cash flow becomes more accessible to manage, ensuring you have a clear picture of your finances. This automation leads to better financial decisions and a healthier cash flow, helping your business thrive.

Use QuickBooks or Xero to send invoices and accept payments online, reducing delays.

Utilize SaasAnt Transactions for quick bulk import and export of financial data, ensuring up-to-date records.

Regularly track and categorize expenses to identify savings opportunities and manage cash flow efficiently.

9. Set a Realistic Goal

Setting realistic goals is essential for effective cash flow management. Small businesses can better predict income and expenses by establishing achievable targets, leading to more accurate financial planning. This proactive approach helps ensure there is enough cash to avoid shortages, ensures timely bill payments, and allows for strategic investments. Realistic goals provide a clear roadmap to enhance small business cash flow stability and foster sustainable growth. Consistently reviewing and adjusting these goals ensures ongoing financial health and agility. Additionally, it enables you to create a reliable cash flow forecast for future planning.

Review past financial data to understand revenue patterns and expenses.

Define clear, measurable goals for income and cost management.

Schedule frequent check-ins to track progress and adjust goals as needed.

10. Careful Crediting

Careful crediting is crucial for improving cash flow. Small business owners should prioritize upfront payments to maintain a steady revenue stream. Offering credit terms requires assessing the current cash flow rate to ensure sustainability. Only extend credit to reliable clients to minimize default risks. Additionally, monitor interest rates to avoid high borrowing costs that strain small business cash management. Implementing stringent credit policies helps maintain a healthy balance between receivables and payables, ultimately enhancing the business's overall financial stability and growth potential.

Conduct thorough credit checks on clients before extending credit.

Define and communicate payment terms clearly, including due dates and penalties for late payments.

Regularly review and follow up on outstanding invoices to ensure timely payments.

11. Strategic Tax Planning

Businesses can reduce their tax burden by understanding and utilizing tax deductions, credits, and incentives the IRS offers. Planning allows businesses to time their expenses and income to maximize tax benefits. For example, making early payments or deferring income can optimize tax liabilities. Regularly consulting with a tax professional ensures compliance and uncovers new savings opportunities. Effective tax planning helps small businesses retain more revenue, enhancing their financial health and stability.

Keep detailed records of all business expenses to maximize deductions.

Regularly meet with a tax advisor to stay updated on IRS regulations and opportunities.

Time major purchases and income to align with tax benefits, reducing taxable income.

12. Say Yes to Lease

Investing in real estate, equipment, and raw materials often seems overwhelming. It is wise to lease on these supplies and properties. Leasing provides you with smaller installments taxed on a monthly or quarterly basis. It is easier to allocate small chunks of cash on business investments regularly. Buying a property/supply can dissolve huge capital at once, making it challenging to pay your monthly bills. Therefore, switch to intelligent leasing for better cash flow management.

Identify essential equipment and properties suitable for leasing instead of buying.

Research and compare leasing terms from multiple providers to get the best deal.

Integrate lease payments into your monthly budget to ensure consistent cash flow management.

13. Monitor Your Cash Flow

Regularly reviewing your income and expenses helps identify trends and potential issues early. Effective cash flow management ensures you can cover your obligations, invest in growth opportunities, and avoid shortfalls. Utilize accounting software or hire an accountant to track and analyze your cash flow statement. Set up weekly or monthly reviews to stay on top of your finances. By keeping a close watch on your cash flow, you can make informed decisions that enhance the stability and growth of your business.

Implement reliable accounting software to track and analyze cash flow in real time.

Schedule weekly or monthly cash flow reviews to stay informed about financial status.

Monitor expenses and cut unnecessary costs to improve cash flow management.

14. Always Aim for Positive Cash Flow

Positive cash flow means more money is coming in than going out, allowing you to cover expenses, invest in growth, and build a financial cushion. To achieve enough cash, focus on timely invoicing, reducing unnecessary costs, and increasing sales. Regularly review your finances to identify and address any cash flow issues early. Maintaining positive small business cash flow ensures you can meet your financial obligations and seize new opportunities. It provides stability and flexibility, helping your business thrive even during tough times. Prioritize actions that boost your cash flow and keep your business financially healthy, avoiding negative cash flow scenarios.

Send invoices promptly to ensure quicker payments and maintain a steady cash flow.

Identify and cut unnecessary expenses to keep more cash within the business.

Implement strategies to increase sales, such as promotions or upselling, to generate more revenue.

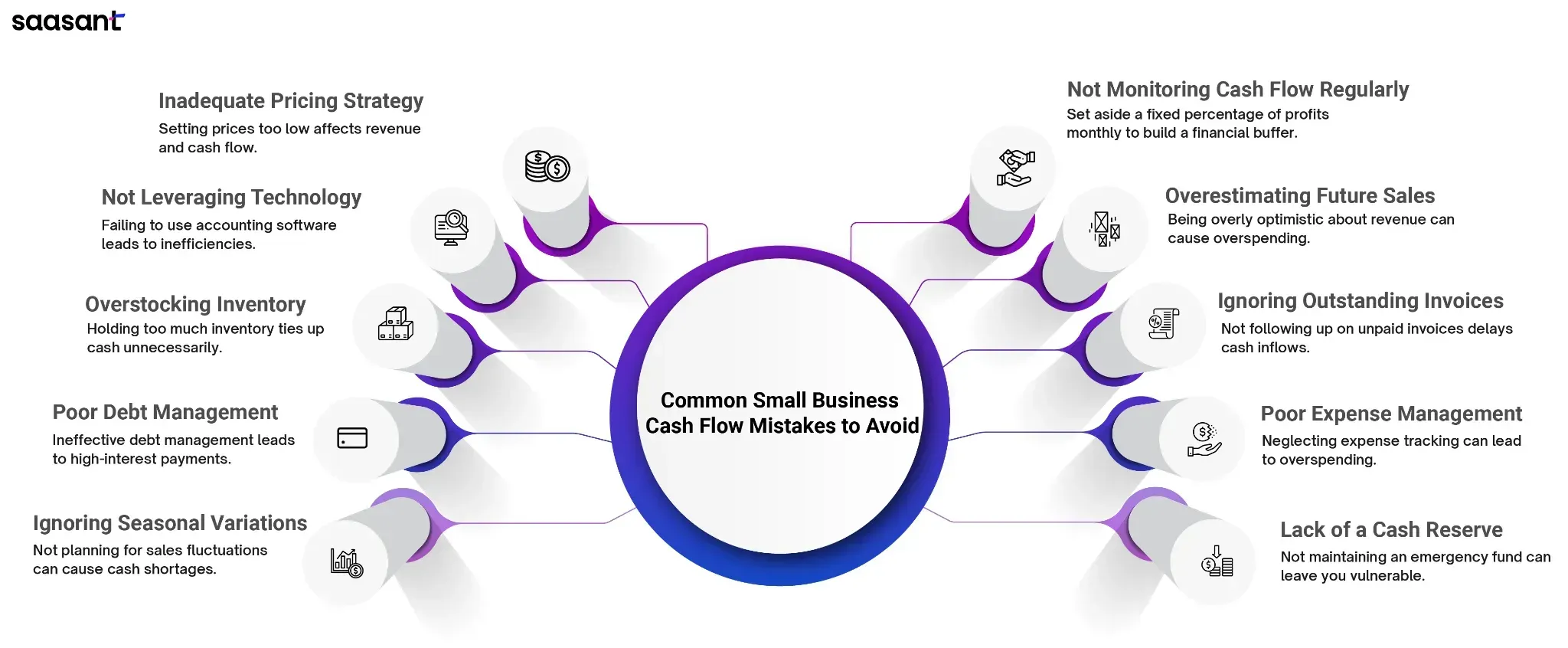

Common Small Business Cash Flow Mistakes to Avoid

1. Not Monitoring Cash Flow Regularly: Failing to track cash flow consistently can lead to unexpected shortages and financial stress.

2. Overestimating Future Sales: Being overly optimistic about future revenue can result in overspending and cash shortages.

3. Ignoring Outstanding Invoices: Not following up on unpaid invoices can delay cash inflows and disrupt your cash flow.

4. Poor Expense Management: Not keeping track of expenses can lead to overspending and reduced cash availability.

5. Lack of a Cash Reserve: Maintaining a cash reserve for emergencies can ensure your business can avoid unexpected expenses.

6. Inadequate Pricing Strategy: Setting prices too low can result in insufficient revenue to cover costs and affect cash flow.

7. Not Leveraging Technology: Failing to use accounting software for automation and accuracy can lead to inefficiencies and errors in cash flow management.

8. Overstocking Inventory: Too much inventory ties up cash that could be used elsewhere.

9. Poor Debt Management: Not managing debt effectively can lead to high interest payments and strain on cash flow.

10. Ignoring Seasonal Variations: Not planning for seasonal fluctuations in sales can result in cash shortages during slow periods.

Wrapping Up

For small business owners, maintaining a positive cash flow is crucial for sustained growth and stability. You can ensure a smooth cash flow cycle by understanding and avoiding common cash flow mistakes. Implementing strategies like leveraging accounting software, setting realistic goals, and careful credit management can significantly improve your financial health.

Regularly monitoring your cash flow and making informed adjustments will keep your business thriving, enabling you to seize new opportunities and navigate challenges effectively. Prioritize these practices to build a solid foundation for your business's financial success.

FAQ

How much cash flow is suitable for a small business?

A positive cash flow where monthly inflows exceed outflows by 10-20% is generally considered suitable for a small business.

What is an example of a cash flow in a small business?

An example of cash flow in a small business is revenue from sales minus expenses like rent, salaries, and utilities, resulting in a net cash balance.

How to manage cash flow in a small business?

To manage cash flow, regularly monitor financial statements, forecast cash needs, control expenses, and maintain a cash reserve for emergencies.

Why do small businesses struggle with cash flow?

Small businesses often need help with cash flow due to delayed customer payments, high operating costs, poor financial planning, and seasonal fluctuations.

What is the rule of thumb for business cash flow?

The rule of thumb is to have a cash reserve equal to three to six months of operating expenses to cover unexpected shortfalls.