How To Find Marginal Cost: Understanding Marginal Cost For Better Business Decisions

Imagine a high-wire act in the bustling marketplace. Businesses are constantly balancing innovation, quality, and affordability on a tightrope of competition. Product cost control becomes a vital skill in this environment, shaping a company's success. Let's delve into why it matters and how a strategic feature called marginal cost analysis can help businesses walk the tightrope with grace.

Customers are savvier than ever, constantly comparing options and seeking the best value. Here's how effective product cost control empowers businesses:

Enhanced Profitability: Businesses can maximize their profit margins by minimizing unnecessary expenses throughout the production cycle. This allows for reinvestment in innovation and growth.

Competitive Advantage: In a price-sensitive market, cost control enables businesses to offer competitive pricing strategies, attracting customers without sacrificing quality.

Financial Stability: Effective cost control safeguards businesses against economic fluctuations and unforeseen circumstances.

What is Marginal Cost? How To Find Marginal Cost?

Marginal cost is basically the extra cost it takes to produce just one more unit of something. Imagine you're a manufacturer of fitness trackers, a booming industry in today's health-conscious world. You've perfected your design and production process, but with increasing competition from overseas manufacturers, you must ensure your pricing remains competitive. Marginal cost analysis becomes your secret weapon.

In simpler terms, marginal cost refers to the additional cost incurred when you produce one extra unit of your fitness tracker. It's not the total cost of manufacturing all your trackers; it's the specific cost of making just one more.

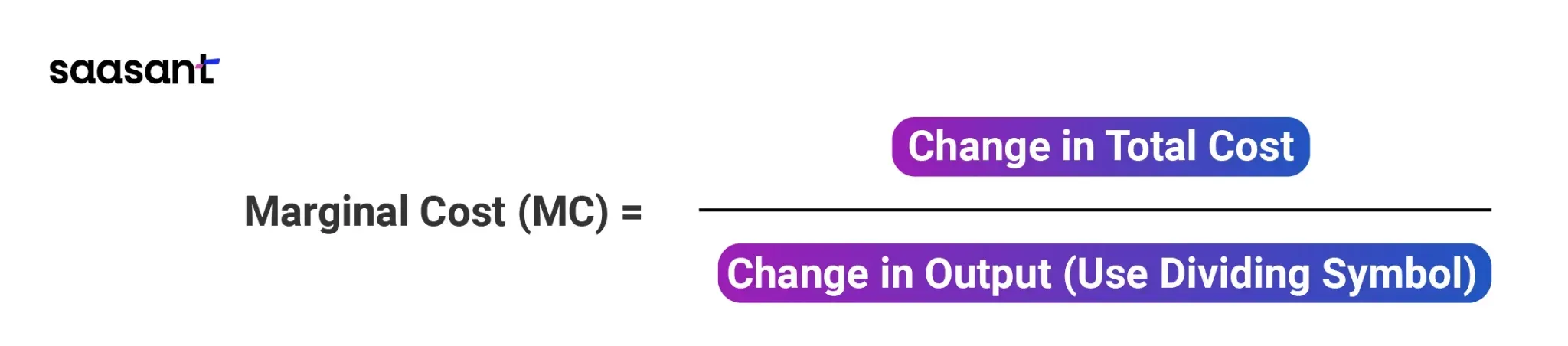

Marginal cost is determined by dividing the change in total cost by the change in quantity produced. Simply put, it represents the extra cost incurred to produce one additional unit of output.

Making More Money: The Secret of Marginal Cost

The global business landscape is undergoing a seismic shift. The rise of e-commerce giants and fierce competition across borders demand a laser focus on efficiency and cost optimization. In this dynamic environment, understanding marginal cost is no longer a niche concept; it's a strategic option for businesses of all sizes.

Understanding Marginal Cost: The Core Concept

At its core, marginal cost analysis focuses on the incremental cost of producing one additional unit of a good or service. It's not about the total cost of production but rather the change in price that occurs when output increases by one unit. This seemingly simple concept unlocks a wealth of valuable insights for businesses.

How Marginal Cost Analysis Empowers Businesses

Let's delve into the various ways marginal cost analysis empowers businesses:

Crafting Profitable Pricing Strategies

Market-Responsive Pricing: Businesses need to be agile and responsive to market fluctuations. Marginal cost analysis helps them set prices that cover production expenses and consider demand elasticity and competitor pricing. By understanding the impact of price changes on customer behavior and overall revenue, businesses can strike the perfect balance between competitiveness and profitability.

Dynamic Pricing Strategies: The rise of e-commerce platforms has ushered in an era of dynamic pricing, where prices fluctuate based on real-time factors like inventory levels, customer behavior, and competitor actions. Businesses can leverage marginal cost analysis to inform these dynamic pricing strategies, ensuring they optimize revenue while remaining competitive in a constantly evolving marketplace.

Optimizing Production Planning for Efficiency

Identifying the Production Sweet Spot: Wouldn't it be ideal to produce at a level that maximizes profit? Marginal cost analysis helps businesses pinpoint this optimal production volume, often called the ‘sweet spot.’ This is where the marginal cost of producing another unit outweighs the additional revenue generated. Operating at this sweet spot ensures efficient resource utilization and minimizes production costs.

Scaling for Growth: As businesses expand, it's crucial to anticipate how production costs might change with increased volume. Marginal cost analysis allows companies to forecast potential cost changes associated with scaling up production. This foresight empowers them to plan for resource allocation and identify cost-saving measures to maintain healthy profit margins during growth phases.

Making Informed Product Mix Decisions

Prioritizing Profit Powerhouses: Not all products within a company's portfolio contribute equally to the bottom line. Marginal cost analysis helps businesses identify which products have the highest profit margins. This allows them to prioritize production and marketing efforts for those items, maximizing overall profitability.

Resource Allocation Efficiency: Businesses can strategically allocate resources by understanding each product's marginal cost. This ensures they invest in production processes and marketing campaigns that generate the highest return on investment. Imagine focusing your marketing efforts on a product that yields significant profits with each additional sale – that's the power of informed resource allocation.

Aligning with Sustainable Business Practices

Minimizing Waste Reduction: The growing focus on environmental responsibility compels businesses to adopt sustainable practices. Marginal cost analysis encourages enterprises to identify areas where production processes can be streamlined, leading to less waste generation and a reduced environmental footprint. This benefits the environment and can lead to cost savings through minimized waste disposal expenses.

Optimizing Resource Consumption: Understanding the marginal cost of raw materials and energy consumption can motivate businesses to explore sustainable alternatives. This can involve using recycled materials, adopting energy-efficient technologies, or implementing lean manufacturing practices. By optimizing resource consumption, companies contribute to a sustainable future and achieve long-term cost savings through reduced resource dependence.

From crafting competitive pricing strategies to optimizing production and product mix, marginal cost analysis empowers businesses to navigate dynamic market conditions while prioritizing sustainability. By incorporating marginal cost analysis into their strategic planning, companies can ensure long-term success and gain a significant competitive advantage in the ever-evolving global marketplace.

How to Calculate Marginal Cost?

In today's ever-changing business world, grasping the concept of marginal cost is crucial for making well-informed decisions. Marginal cost essentially signifies the extra cost accrued when producing one more unit of a product or service.

The foundation of a robust marginal cost calculation lies in accurate data. Here's how to ensure reliable figures:

Total Cost Tracking: Implement a meticulous system for capturing all production costs. This encompasses fixed costs (rent, insurance) and variable costs (raw materials, direct labor). Utilize accounting software or detailed spreadsheets for comprehensive cost recording.

Production Volume Monitoring: Precisely track your output volume. This can involve units manufactured, services rendered, or digital products delivered. Integrate production data with your cost-tracking system for efficient analysis.

Calculating Marginal Cost: A Step-by-Step Approach

Once you have accurate data, follow these steps:

Define Your Production Range: Select a relevant production range for analysis. Depending on your business cycle, this could be weekly, monthly, or quarterly.

Gather Total Cost and Output Data: Collect total production costs and corresponding output volume data for at least two points within your chosen production range.

Calculate the Change in Cost: Subtract the total cost at the lower production level from the total cost at the higher production level.

Calculate the Change in Output: Subtract the output volume at the lower production level from the output volume at the higher production level.

Apply the Formula: Divide the change in total cost (step 3) by the change in output (step 4). This will yield your marginal cost per unit.

Marginal Cost (MC) = ΔTC/ΔQ

Where:

ΔTC = Change in Total Cost

ΔQ = Change in Output

Beyond the Basics: Modern Considerations

In the digital age, consider these additional factors:

Step Costs: Certain costs might increase in ‘steps’ rather than smoothly. For instance, hiring additional staff might only occur once a specific production threshold is reached. Account for these step changes when analyzing marginal cost.

Technology Integration: Leverage technology to streamline data collection and analysis. Cloud-based accounting tools and data visualization software can significantly enhance efficiency.

By following these steps and incorporating modern best practices, you can effectively calculate marginal costs in today's dynamic business environment. This valuable metric empowers you to make informed decisions regarding production levels, pricing strategies, and overall business optimization.

Example: Fitness Trackers and the Cost of "Scaling Up"

Let's say your fitness tracker's base components (electronics, display) cost $10 (fixed cost). Imagine you have an optimized production line and decide to manufacture one more unit. You might only need a few cents of extra materials (variable cost) like packaging and assembly. This additional cost of a few cents for that one extra tracker is your marginal cost.

Fixed vs. Variable Costs: Understanding the Nuances

While the core concept remains the same, the nature of costs in a globalized, e-commerce-driven world has evolved. Here's a breakdown with some modern-day examples:

Fixed Costs

These remain constant regardless of production volume. In the fitness tracker example, the $10 for base components is a fixed cost. Rent, salaries for product designers and depreciation of manufacturing equipment are other common examples. In the digital age, software licenses, and cloud storage for e-commerce platforms can also be considered fixed costs.

Variable Costs

These fluctuate directly with your production output. In the tracker example, the extra materials used for one more unit are a variable cost. For e-commerce businesses, variable costs might include:

Transaction fees: Paid to e-commerce platforms like Shopify for each online sale.

Shipping costs: Fluctuate based on weight, destination, and chosen shipping method.

Pay-per-click (PPC) advertising costs: These can vary depending on the number of clicks your online ads receive.

The Role of Fixed and Variable Costs in Marginal Cost

Fixed costs don't directly factor into marginal cost calculations because they remain the same no matter how much you produce. However, understanding them is essential because they contribute to the overall cost structure and influence your pricing strategy.

Beyond Basic Manufacturing: The Expanding Role of Marginal Cost Analysis in the Digital Age

In today's globalized marketplace, with a growing emphasis on e-commerce, marginal cost analysis extends beyond traditional manufacturing. Here's how it empowers businesses:

Optimizing Production for E-commerce: Businesses can identify the ideal production volume to meet online demand while minimizing costs. This is crucial for efficient inventory management and avoiding stock-outs that can damage customer satisfaction.

Strategic E-commerce Pricing: Knowing the actual cost per unit allows for data-driven pricing that considers production costs, competitor pricing, and global market trends. This is especially important during flash sales and promotions, where margins can be tight.

Informed Decisions on Online Marketing: Marginal cost analysis can guide decisions on online advertising budgets. Businesses can evaluate the cost-effectiveness of PPC campaigns and optimize their online marketing spend for maximum return on investment (ROI).

Businesses can optimize production, establish competitive pricing strategies, and allocate resources effectively across their global e-commerce operations by analyzing the additional cost of producing each unit. This strategic approach can be the key to unlocking a significant competitive edge in the ever-evolving global marketplace.

Fixed vs. Variable: A Practical Approach in the Digital Age

Separating fixed and variable costs can be more intricate in the digital era. Here are practical tips for the modern business:

Identify Core Fixed Costs: Rent, salaries, and utilities are classic examples of fixed costs that remain constant within a specific production scale.

Scrutinize Variable Costs: Raw materials and direct labor are traditional variable costs. In the digital age, cloud-based services often function as variable costs, scaling up or down with your usage. Analyze cloud service subscriptions to determine their variable nature.

Embrace Cost Allocation: Allocate certain costs that exhibit characteristics of both fixed and variable proportionally based on relevant metrics. For instance, internet bandwidth might be partially fixed and variable based on user activity.

Cost Control for Profits: Unlock the Power of Marginal Cost

The global marketplace is more interconnected than ever, with dynamic customer demands and fierce competition. To navigate this environment successfully, businesses require a sharp decision-making approach. Enter marginal cost analysis, a powerful technique that empowers businesses to optimize their operations and maximize profits.

Pitfalls of Marginal Cost Analysis

Marginal cost analysis is a cornerstone of informed business decision-making. It helps determine the impact of production changes on profitability by focusing on the cost of producing one additional unit. While a powerful strategy, marginal cost analysis has limitations that users should know to ensure effectiveness.

The Grey Area: When Fixed and Variable Costs Blur

A fundamental principle of marginal cost analysis (MCA) is the clear separation of fixed and variable costs. This seemingly straightforward categorization becomes murky when we encounter semi-variable costs. These costs defy the clean lines of traditional fixed and variable categories, posing a challenge for accurate marginal cost analysis.

The Fixed-Variable Dichotomy

Traditionally, fixed costs remain constant irrespective of production volume. Examples include rent, salaries, and insurance. Variable costs, on the other hand, fluctuate directly with output. Raw materials, direct labor, and utilities are classic examples.

The Messy Middle: Semi-Variable Costs

However, the natural world presents a spectrum of costs that don't fit neatly into these categories. Semi-variable costs, also known as mixed costs, exhibit a stepped pattern rather than a smooth linear relationship with production volume. Here's why they create difficulties:

Step Increases: Imagine a factory that hires additional workers only when production reaches a certain threshold. The cost of labor jumps in steps, not smoothly, as production increases.

Overtime: Salary expenses might be fixed to a certain point but then increase due to overtime pay as production demands rise.

Minimum Order Quantities: Utilities might have a fixed base charge but then increase in steps based on usage tiers.

The Impact on Marginal Cost Analysis

Semi-variable costs can lead to inaccurate marginal cost calculations, potentially derailing business decisions based on marginal cost analysis. Here's how:

Misallocation of Costs: If a semi-variable cost is misclassified as purely fixed or variable, it can distort the accurate cost picture. This can lead to underestimating costs at higher production levels or overestimating profitability at lower levels.

Suboptimal Decisions: Flawed cost data can lead to suboptimal pricing, production levels, or product mix choices. For instance, a business might decide to increase production based on underestimating costs, which could lead to financial strain.

Taming the Grey Area

Despite the challenges, there are ways to mitigate the impact of semi-variable costs on marginal cost analysis:

Cost Drivers: Identify the key factors that drive changes in semi-variable costs. Is it overtime hours, additional workers, or increased utility usage? Understanding these drivers allows for more accurate cost predictions.

High-Low Method: This accounting technique estimates a semi-variable cost's variable and fixed components by analyzing data from periods with high and low production levels.

Activity-Based Costing (ABC): This approach assigns costs to activities rather than departments. It can help identify the cost drivers of semi-variable expenses.

The External Cost Conundrum: When Profitability Doesn't Tell the Whole Story

Marginal cost analysis (MCA) is a valuable business strategy but often operates within a self-contained bubble. Traditional marginal cost analysis focuses on a company's internal costs, the expenses directly incurred during production, such as raw materials, labor, and utilities. However, a company's operations can generate significant external costs, impacting the environment and society. These external costs, like pollution or resource depletion, are borne by society and not reflected in the business's accounting records. While MCA might paint a rosy picture of profitability, it neglects the potential negative externalities a company's activities may create.

The Case for Considering External Costs

There are several compelling reasons why businesses should be mindful of external costs, even though they aren't directly captured in marginal cost analysis:

Ethical Responsibility: Businesses are responsible for operating in a way that minimizes their negative impact on the environment and society. Ignoring external costs can lead to unsustainable practices that harm the communities in which they operate.

Long-Term Sustainability: Environmental regulations and societal pressure increasingly hold businesses accountable for their external costs. Companies proactively addressing these costs can gain a competitive edge and ensure long-term sustainability.

The Future of Cost Accounting: As environmental concerns rise, regulators and accounting bodies might start incorporating external costs into traditional accounting frameworks. Businesses that are prepared for this shift will be better positioned to adapt.

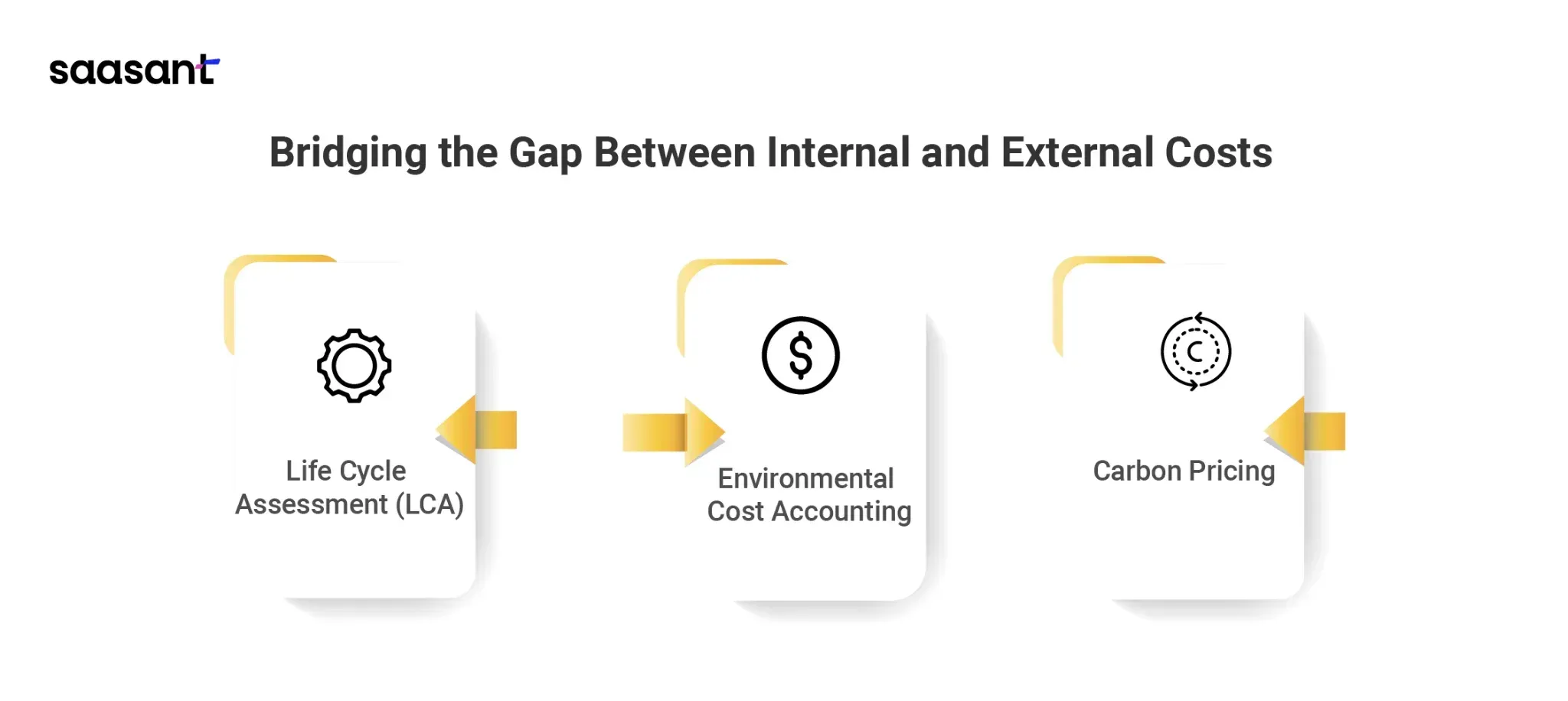

Bridging the Gap Between Internal and External Costs

While quantifying external costs can be challenging, there are steps businesses can take to bridge the gap:

Life Cycle Assessment (LCA): This technique assesses the environmental impact of a product or service throughout its lifecycle, from raw material extraction to disposal.

Environmental Cost Accounting: This approach integrates environmental costs into traditional accounting systems, providing a more holistic view of a company's impact.

Carbon Pricing: Companies can implement internal carbon pricing mechanisms to reflect the potential cost of their carbon emissions.

By understanding these limitations, businesses can leverage marginal cost analysis effectively. Here are some key takeaways:

Refine Cost Classification: Continuously evaluate cost behavior to ensure a clear distinction between fixed and variable cost categories.

Regular Cost Updates: Integrate cost updates into your analysis to account for market fluctuations.

Consider External Costs: While not directly factored in, acknowledge and strive to minimize your operations' environmental and social impact.

Wrap Up

Understanding how to optimize production, craft competitive pricing strategies, and make data-driven decisions is crucial for success. This is where marginal cost analysis comes in - a powerful strategy that empowers businesses of all sizes. By analyzing the incremental cost of producing one additional unit, companies can gain valuable insights to inform their strategy.

Marginal cost analysis hinges on the ability to distinguish between fixed costs and variable costs clearly. Fixed costs, like rent or salaries, remain constant regardless of production volume. Variable costs, on the other hand, fluctuate directly with output, such as raw materials or direct labor. Factors like fluctuating exchange rates and labor costs can influence cost structures in the globalized business landscape. Therefore, businesses must continuously evaluate cost behavior to ensure accurate categorization for practical marginal cost analysis.

Another key to success is embracing continuous improvement. The global market is dynamic, and so should your cost analysis. Regularly integrating cost updates into your analysis ensures your decisions are based on the most recent data. This adaptability is vital for global businesses navigating a constantly changing environment.

While marginal cost analysis focuses on a company's internal costs, responsible businesses acknowledge their operations' environmental and social impact. Though not directly factored into calculations, these external costs are borne by society and can have long-term consequences. Businesses that prioritize sustainability by minimizing their negative externalities not only contribute to a better future but can also gain a competitive edge. There are ways to bridge the gap between internal and external costs, such as life cycle assessments or environmental cost accounting.

By understanding the power and limitations of marginal cost analysis, businesses can leverage it for informed decision-making. Regularly refining cost classification, embracing continuous cost updates, and considering external costs are essential practices. When employed strategically, marginal cost analysis empowers businesses to thrive in a competitive environment and contribute to a more sustainable future. Explore resources on cost accounting best practices or consider contacting professionals to help you optimize your operations and achieve your strategic goals.

FAQs

How Do I Calculate Marginal Cost?

The core formula for marginal cost (MC) is:

Marginal Cost = Change in Total Cost (between two production levels) / Change in Output (between the same two production levels)

Here's a step-by-step approach:

Define your relevant production range (weekly, monthly, etc.)

Collect total cost and output data for at least two points within your chosen range.

Calculate the change in cost (ΔTC) and output (ΔQ).

Divide ΔTC by ΔQ to get the marginal cost per unit.

How to Find Marginal Cost From Total Cost?

While total cost reflects the overall expense of producing a certain quantity of goods, marginal cost focuses on the cost change for each additional unit. It provides a more granular view of production efficiency.

Finding Marginal Cost: The Formula

The formula for marginal cost (MC) is:

MC = ΔTC / ΔQ

Here's what each symbol represents:

MC: Marginal Cost

ΔTC: Change in Total Cost (the difference in total cost between producing one more unit and the previous quantity)

ΔQ: Change in Quantity (the additional unit produced)

How Is Marginal Cost Calculated?

Marginal cost is calculated by dividing the change in total cost by the change in quantity produced. In simpler terms, it's the additional cost incurred for producing one more unit of output.

How Does a Firm Calculate Marginal Cost?

Firms calculate marginal cost by analyzing the change in total production cost associated with producing one additional unit of a good or service.

Formula for Marginal Cost:

Marginal cost (MC) is calculated using the following formula:

MC = ΔTC / ΔQ

Where:

MC represents Marginal Cost

ΔTC signifies the Change in Total Cost (difference in total cost between producing one more unit and the previous quantity)

ΔQ represents the Change in Quantity (the additional unit produced)

What Is Marginal Cost Analysis?

Marginal cost analysis examines the additional cost incurred when producing one extra unit of a product or service. It goes beyond total production costs and focuses on the variable costs that fluctuate with output levels. This information helps businesses make data-driven pricing, production levels, and product mix decisions.

How Can Marginal Cost Analysis Help My Business?

Marginal cost analysis empowers businesses in several ways:

Crafting profitable pricing strategies: It helps you understand how cost changes impact price and profit, allowing you to set competitive yet profitable prices.

Optimizing production planning: You can minimize waste and production costs by identifying the production volume that maximizes profit (the "sweet spot").

Making informed product mix decisions: Analyze which products have the highest profit margins to prioritize production and marketing efforts.

Aligning with sustainable practices: Identify areas to streamline production processes, reducing waste and environmental impact.

What Are Some Challenges Of Using Marginal Cost Analysis?

Separating fixed and variable costs: Some costs exhibit characteristics of both, requiring careful analysis for categorization (e.g., semi-variable costs like overtime pay).

External costs: Traditional MCA focuses on internal production costs and might not consider environmental or social impacts (external costs).

How Can I Overcome The Challenges Of Marginal Cost Analysis?

Refine cost classification: Regularly evaluate cost behavior to ensure a clear distinction between fixed and variable categories.

Use cost allocation methods: To identify cost drivers for semi-variable costs, employ techniques like the high-low method or activity-based costing (ABC).

Consider external costs: While not directly included in calculations, acknowledge and strive to minimize your environmental and social impact. For a more holistic view, explore life cycle assessments (LCA) or environmental cost accounting.

Is Marginal Cost Analysis Only Relevant For Manufacturing Businesses?

No, marginal cost analysis is valuable for businesses of all sizes, including e-commerce companies.

In e-commerce, marginal costs can include:

Variable costs include transaction fees, shipping, and pay-per-click (PPC) advertising costs.

Analyzing these costs helps optimize your online advertising budget and set competitive pricing for e-commerce products.

How Can I Use Marginal Cost Analysis For E-commerce Product Pricing?

Marginal cost analysis helps you understand the actual cost per unit of your product, considering the following:

Production costs (if applicable).

Shipping costs.

Payment processing fees.

By factoring in these costs, you can set prices that cover your expenses while remaining competitive in the online marketplace.

Can Marginal Cost Analysis Help With Discounts And Promotions In E-commerce?

Yes, marginal cost analysis is crucial for planning and evaluating discounts and promotions.

Understanding your marginal cost allows you to:

Set minimum prices that ensure profitability even during sales.

Analyze the impact of discounts on your overall profit margin.

Identify the most cost-effective ways to structure promotions (e.g., free shipping vs. percentage discounts).

How Does Marginal Cost Analysis Affect Inventory Management In E-commerce?

By understanding your marginal cost, you can optimize your production or purchasing decisions to minimize excess inventory.

Knowing your ideal production volume (identified through marginal cost analysis) helps you avoid stock-outs that can damage customer satisfaction.

You can also manage inventory levels more effectively by understanding how storage costs impact your marginal cost per unit.

What Tools Or Resources Can Help Me With Marginal Cost Analysis?

There are several tools and resources available to help you with marginal cost analysis:

Accounting software: Most accounting software allows you to track and categorize costs, making data collection easier.

Spreadsheet templates: You can find online spreadsheet templates designed explicitly for marginal cost clculations.

Cost accounting professionals: Consulting with a cost accountant can guide cost classification and analysis methods.