Understanding the Unified Chart of Accounts (UCOA)

Do you know the crucial role a Chart of Accounts (COA) plays in organizing and tracking financial transactions for businesses and organizations? A Unified Chart of Accounts (UCOA) takes it further, standardizing financial reporting across departments and divisions.

A UCOA is even more critical for nonprofits, ensuring transparency and accountability to donors and grantors. Inaccurate or disorganized accounts can lead to poor decision-making and, in some cases, financial ruin.

On the other hand, a well-organized UCOA is essential for accurate financial reporting and analysis. It provides a framework for financial decisions and a means of understanding the financial health of an organization.

This article explains the importance and benefit of having a Unified Chart of Accounts for nonprofits. We will also discuss how to implement a UCOA for nonprofit organizations. Stick around for tips and insights to optimize your nonprofit's financial management.

Contents

Nonprofit Chart of Accounts

Standard Chart of Accounts

Implementing and Using a Chart of Accounts

Summing it Up

FAQs

Three critical features of a Chart of Accounts

The Unified Chart of Accounts (UCOA) standard Chart of Accounts allows for consistent reporting and comparison of financial data across different organizations. It is a standardized list of account codes that can classify financial transactions into a structured format. The UCOA provides a uniform method of recording and reporting financial information and simplifies the preparation of financial statements.

History of UCOA

The Unified Chart of Accounts (UCOA) was developed by the Financial Accounting Standards Board (FASB) in the 1990s to improve financial reporting. Before the introduction of UCOA, organizations had different charts of account structures, making it difficult to compare financial information across entities.

It meant that stakeholders such as investors, regulators, and analysts had difficulty analyzing financial data from different organizations, especially those operating in different industries.

In response to this challenge, the FASB began developing a standardized Chart of Accounts that would be uniform across different industries and organizations. The goal was to create a Chart of Accounts that would provide consistency and clarity in financial reporting, making it easier for stakeholders to analyze and compare financial data across different entities.

After years of consultation and stakeholder collaboration, the FASB eventually released the UCOA in the late 1990s. The UCOA is designed to be a flexible and scalable Chart of Accounts used by different organizations across various industries.

It is intended to provide a standardized format for organizing and reporting financial data to improve the quality and comparability of financial information.

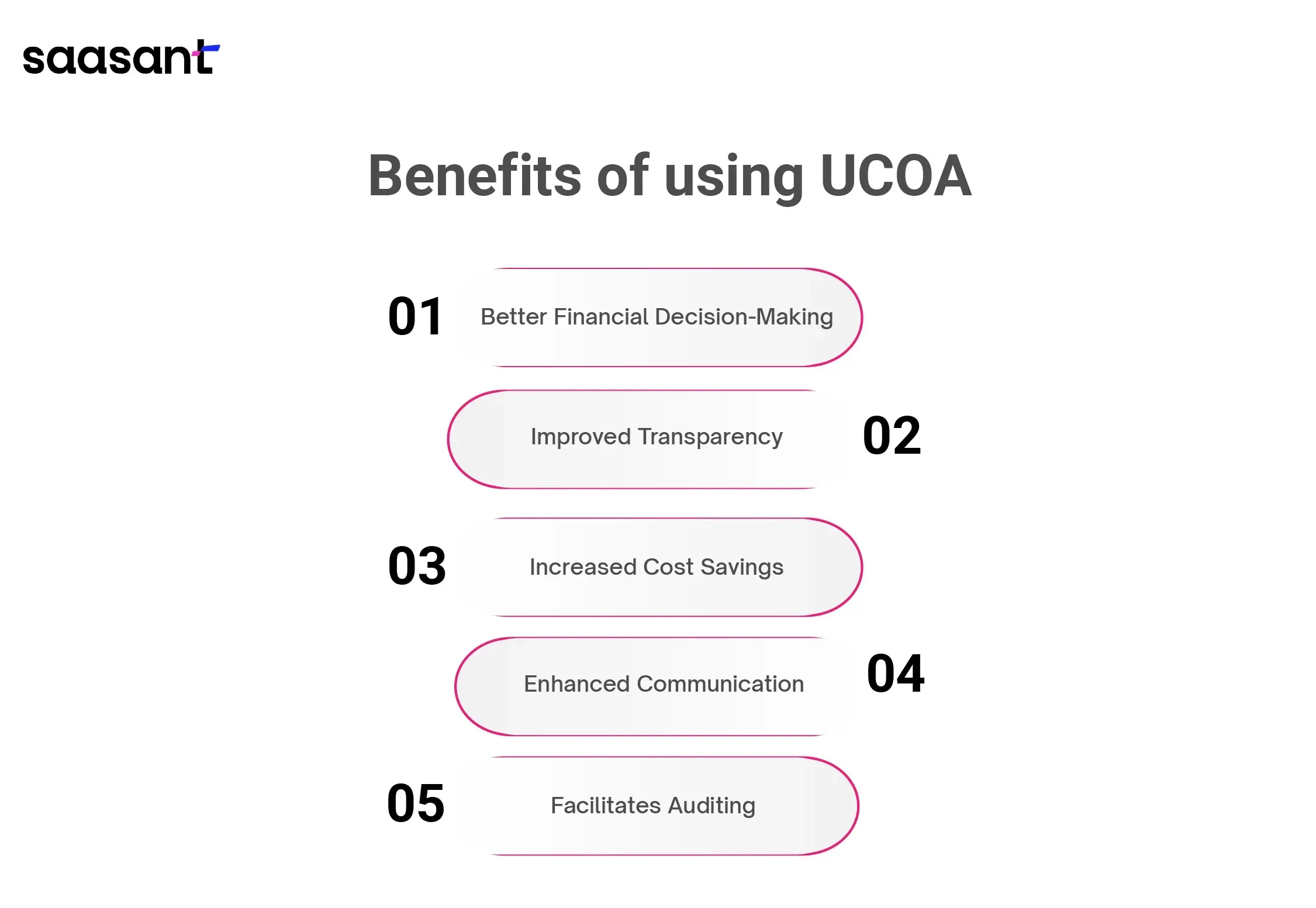

Benefits of Using UCOA

The benefits of using UCOA extend beyond the advantages of consistency, comparability, efficiency, accuracy, and compliance. Here are some additional benefits of using UCOA:

1. Better Financial Decision-Making: Organizations can make informed and data-driven decisions with standardized financial data. The UCOA enables organizations to quickly identify and analyze trends, track expenses, and forecast future financial performance.

2. Improved Transparency: Standardizing financial reporting using UCOA allows stakeholders to access and understand financial data easily. It promotes transparency and accountability, as stakeholders can track financial data and hold organizations accountable for their financial performance.

3. Increased Cost Savings: The UCOA can help organizations reduce costs associated with financial reporting. By streamlining the reporting process and reducing the need for customization, organizations can save time and money on financial reporting.

4. Enhanced Communication: A standardized Chart of Accounts facilitates communication between organizational departments and entities. It allows for better collaboration and coordination, promoting overall organizational efficiency.

5. Facilitates Auditing: Standardized financial reporting through UCOA makes it easier for auditors to review financial data, reducing the time and effort required for auditing. It can lead to more accurate and efficient auditing processes.

Nonprofit Chart of Accounts

Nonprofit organizations have unique accounting needs requiring a specific Chart of Accounts. The Chart of Accounts for nonprofits is designed to track various revenue streams, donations, grants, and other types of income.

It also records expenses related to the organization's mission, such as program, administrative, and fundraising expenses. The Chart of Accounts for nonprofits typically includes four main categories of accounts: assets, liabilities, income, and costs.

Under these categories, specific subcategories break down each account in more detail. For instance, under the assets category, there may be subcategories such as cash, accounts receivable, and investments.

Additionally, nonprofit organizations often have accounts specific to their mission, such as program expenses for particular programs or projects. For example, a nonprofit focused on providing education may have subcategories such as teacher salaries, classroom supplies, and educational materials.

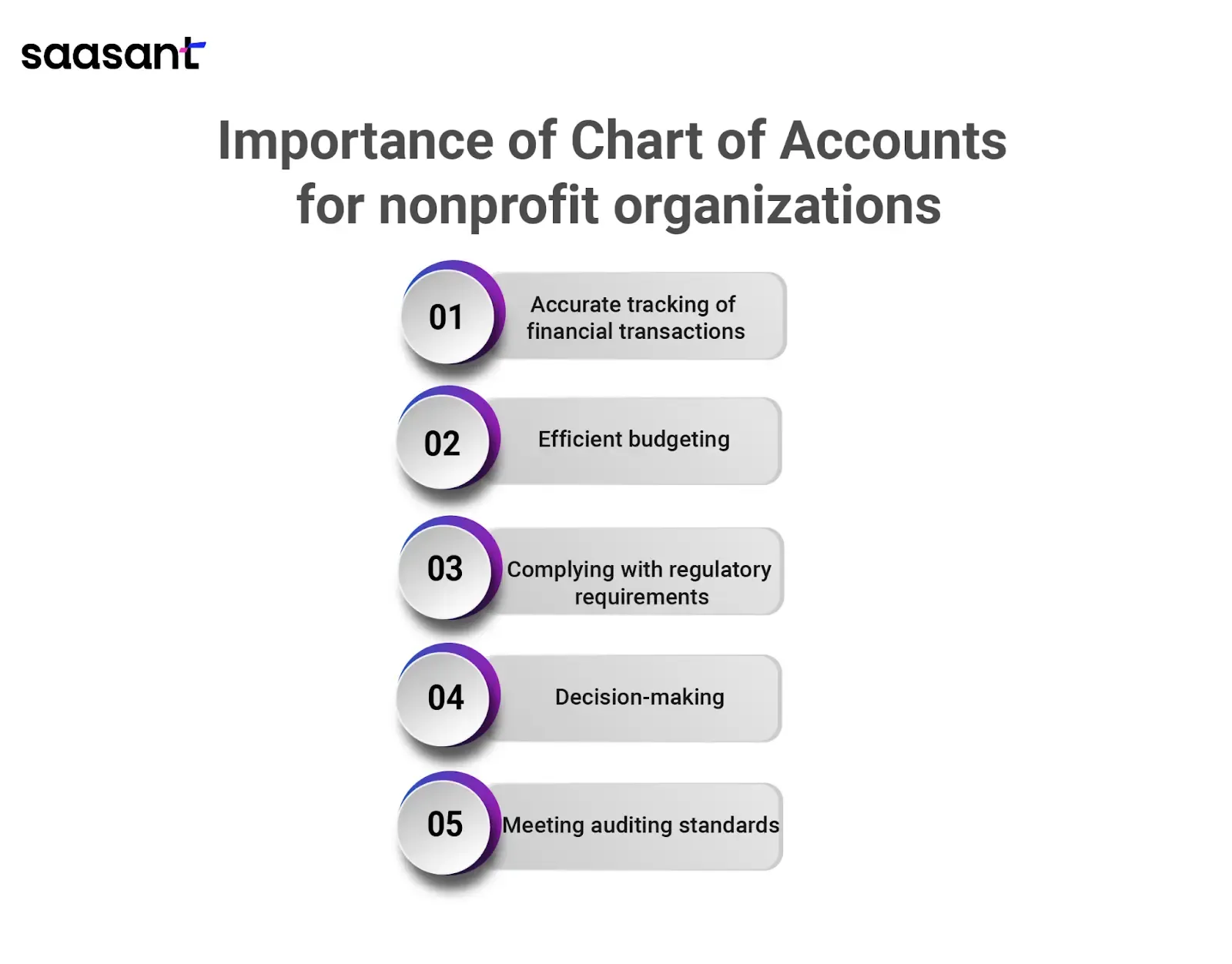

Importance of a Chart of Accounts for Nonprofit Organizations

A nonprofit organization's Chart of Accounts is essential for proper financial management. It allows the organization to accurately track income and expenses, vital for budgeting, forecasting, and making informed decisions.

A proper Chart of Accounts ensures consistency and accuracy in financial reporting, making it easier to comply with regulatory requirements and meet auditing standards.

Accurate tracking of financial transactions: A Chart of Accounts enables nonprofit organizations to track their financial transactions accurately. It helps them know their income sources and how the money is spent.

Efficient budgeting: A Chart of Accounts allows nonprofit organizations to budget effectively. They can create budget categories that reflect their organization's mission, goals, and objectives.

Decision-making: A Chart of Accounts provides vital information nonprofit organizations can use to make informed decisions. By analyzing financial data, they can identify areas where they need to cut costs, invest more, or implement better financial management practices.

Complying with regulatory requirements: Nonprofit organizations must comply with specific regulatory requirements, such as filing tax returns and adhering to accounting standards. A Chart of Accounts helps ensure they meet these requirements by providing accurate financial data.

Meeting auditing standards: A well-designed Chart of Accounts helps nonprofit organizations to meet auditing standards. It provides a clear overview of their financial position, making it easier for auditors to review their financial statements and assess their financial health.

FASB nonprofit Chart of Accounts

The Financial Accounting Standards Board (FASB) nonprofit Chart of Accounts is designed to help nonprofit organizations meet financial reporting requirements and provide transparency to stakeholders.

It includes a set of standard account codes and descriptions covering all the everyday financial transactions a nonprofit organization may encounter. The FASB nonprofit Chart of Accounts is an effective tool for nonprofits that want to maintain a comprehensive record of their financial activities and ensure compliance with regulatory requirements.

The FASB nonprofit Chart of Accounts is organized according to the four financial statements that nonprofits must produce, which are:

1. Statement of financial position

2. Statement of activities

3. Cash flow statement and

4. Functional Expense Statement of the organization

The Chart of Accounts includes account codes and descriptions for assets, liabilities, net assets, revenue, expenses, and other financial transactions. The FASB nonprofit Chart of Accounts also provides information on functional expenses, which is essential for nonprofits to demonstrate their programmatic and administrative costs.

Nonprofits can customize the FASB nonprofit Chart of Accounts to fit their needs, but the standard codes and descriptions provide a starting point for designing a comprehensive Chart of Accounts.

The FASB nonprofit Chart of Accounts is an essential resource for nonprofit organizations that want to improve their financial reporting and meet stakeholders' expectations.

AICPA Nonprofit Chart of Accounts

Another standard for nonprofit Chart of Accounts is the American Institute of Certified Public Accountants (AICPA). This Chart of Accounts is designed to provide nonprofits with a more detailed and comprehensive framework for organizing their financial transactions.

It includes a more extensive list of accounts, enabling nonprofits to track their expenses and revenues more accurately and to generate more detailed financial reports. The AICPA Chart of Accounts is organized into three sections:

1. Assets

2. Liabilities and net assets

3. Revenues and expenses

Under each section, numerous accounts allow nonprofits to track various transactions. For instance, there are cash, investments, grants receivable, and fixed assets accounts under the assets section.

Under the liabilities and net assets section, there are accounts for accounts payable, deferred revenue, and various types of net assets. The AICPA Chart of Accounts also includes sub-accounts that enable nonprofits to track transactions more granularly.

For instance, there are sub-accounts for salaries and wages, benefits, and office expenses under the expenses section. These sub-accounts allow nonprofits to track costs by department or function.

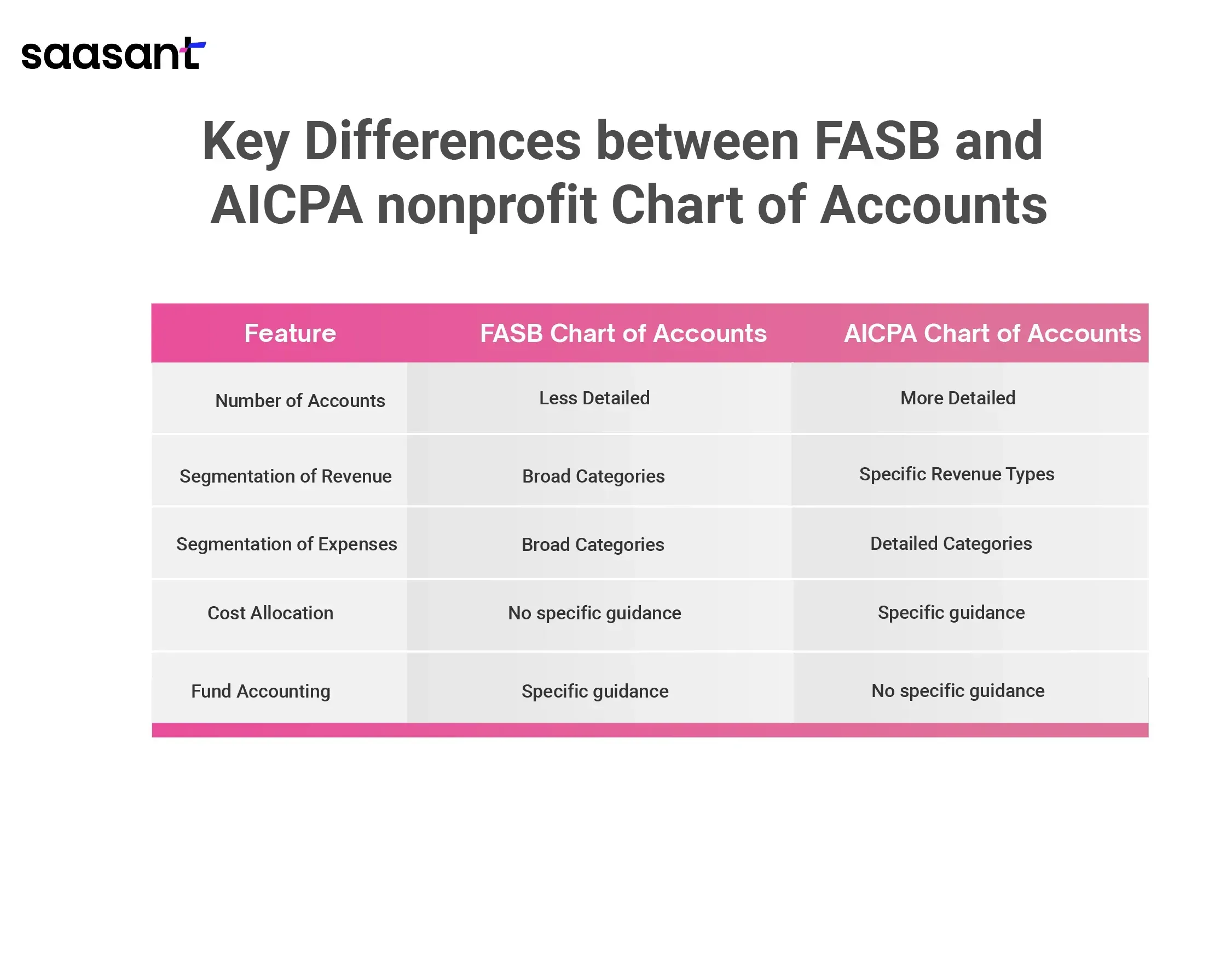

Here's a table outlining some critical differences between the FASB and AICPA Nonprofit Chart of Accounts:

Note that this is not an exhaustive list of differences but highlights some critical distinctions between the two Chart of Accounts. Organizations should consider their specific needs and consult their financial advisors before choosing a Chart of Accounts.

Note that this is not an exhaustive list of differences but highlights some critical distinctions between the two Chart of Accounts. Organizations should consider their specific needs and consult their financial advisors before choosing a Chart of Accounts.

Sample nonprofit Chart of Accounts in QuickBooks

QuickBooks is an accounting software designed to help small and medium-sized businesses manage their financial operations. Nonprofit organizations can use QuickBooks to track donations, grants, and other sources of income, as well as expenses related to fundraising, programs, and administrative activities.

QuickBooks provides a sample nonprofit Chart of Accounts that can be used as a starting point for setting up the organization's accounting system. The sample nonprofit Chart of Accounts in QuickBooks includes a standard set of accounts organized into assets, liabilities, equity, income, and expenses.

Under assets, for example, there may be sub-accounts such as cash, accounts receivable, and prepaid expenses. At the same time, liabilities may have sub-accounts such as accounts payable, loans payable, and deferred revenue.

The income category has sub-accounts such as contributions, grants, and program service fees, while expenses have sub-accounts such as salaries and wages, rent, and office supplies.

Nonprofits can customize the Chart of Accounts to reflect their specific financial transactions and reporting requirements. For example, they may add or delete accounts, create sub-accounts, and change account numbers or names.

QuickBooks also allows nonprofits to generate financial reports such as balance sheets, income statements, and cash flow statements based on the Chart of Accounts. It helps nonprofits to monitor their financial performance, make informed decisions, and meet regulatory requirements.

Chart of Accounts for nonprofit church

A Chart of Accounts for a nonprofit church is an essential tool for accurate financial reporting and management. The categories and subcategories included in the Chart of Accounts should be designed to reflect the unique financial transactions of a church.

The following are some of the key features that should be included in a Chart of Accounts for a nonprofit church:

![chart of accounts]-38.webp](https://images.saasant.info/chart_of_accounts_38_9e6c0182a0.webp)

1. Tithes and Offerings: This category should include all donations the church receives, including tithes, offerings, and special donations.

2. Missions: Churches often support local and global missions, and this category should include all expenses related to supporting missionaries and missions.

3. Building Maintenance: This category should include expenses related to maintaining and repairing the church's facilities, such as repairs, maintenance, and utilities.

4. Staff Salaries: This category should include salaries and benefits for all church staff members, including pastors, administrators, and support staff.

5. Programs and Ministries: A church's Chart of Accounts should also have subcategories for different programs and ministries, such as children's ministry, youth ministry, and music ministry. These subcategories will help track the expenses related to each program.

By using a well-organized Chart of Accounts tailored to a nonprofit church's unique needs, the organization can improve its financial reporting accuracy and efficiency, leading to better decision-making and resource management.

Donations in Chart of Accounts

Donations are integral to nonprofit organizations and must be appropriately recorded and tracked in their financial statements. A separate category for donations in the Chart of Accounts helps nonprofit organizations manage and understand the impact of donations on their financial health.

The donation category should include subcategories that distinguish between restricted and unrestricted donations. Restricted donations come with specific conditions, such as being used for a particular program or project.

On the other hand, unrestricted donations allow nonprofits to use the funds as needed. Another subcategory within donations could be for individual and corporate contributions. This differentiation helps to analyze and understand the organization's funding sources.

Tracking grants received can also benefit nonprofits, as they may come with specific reporting requirements or restrictions.

Properly tracking and reporting donations in the Chart of Accounts is critical for complying with regulatory requirements and meeting auditing standards. It also helps nonprofits make informed decisions about allocating funds and planning for the future.

Standard Chart of Accounts

Definition of Standard Chart of Accounts

A standard Chart of Accounts is an essential tool that organizations use to streamline their accounting processes. It is designed to provide a consistent and structured system that can be applied across different departments, business units, and industries.

It is a common language that enables stakeholders to communicate financial information effectively. A typical standard Chart of Accounts consists of a hierarchical structure of accounts that reflects the organization's financial activities.

It typically includes a range of accounts, such as assets, liabilities, equity, income, and expenses. Each account has a unique code, name, and description, which helps to identify the account and the financial transactions it represents.

The account codes are usually hierarchical, making grouping accounts and navigating through the Chart of Accounts easier. Organizations of all sizes and industries widely use the Standard Chart of Accounts, including private and public companies, government agencies, and nonprofit organizations.

Using a standard Chart of Accounts provides numerous benefits, including increased efficiency, accuracy, and comparability of financial information. It also simplifies the preparation of financial statements and ensures compliance with accounting standards and regulations.

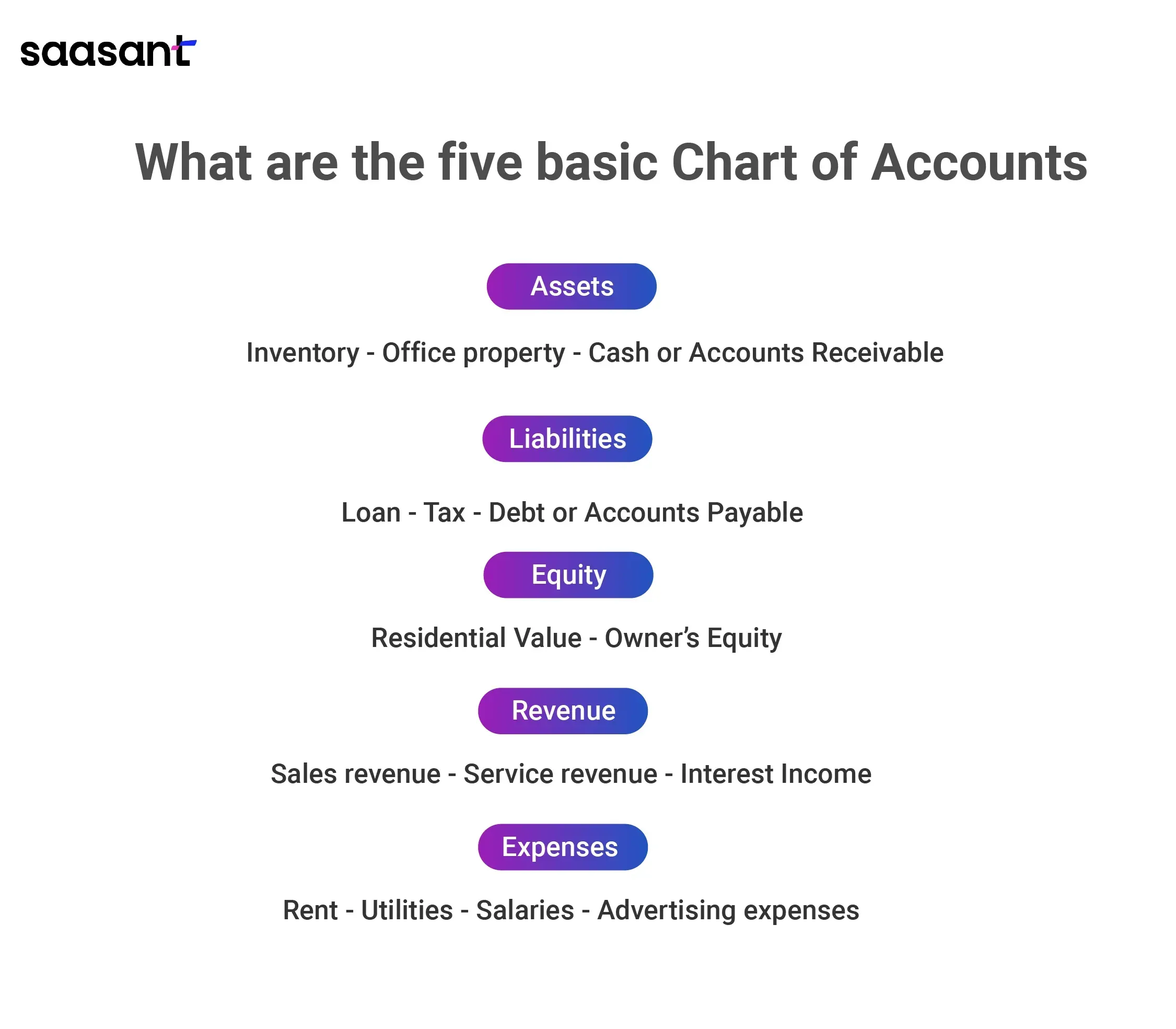

What are the five basic charts of accounts?

The five basic charts of accounts are the foundation of any organization's accounting system. These categories help to ensure consistency and accuracy in financial reporting across the organization.

1. Assets - This category includes all an organization's resources, such as cash, accounts receivable, inventory, equipment, and property. Assets are typically listed in order of liquidity, with the most liquid assets appearing at the top.

2. Liabilities - This includes all the debts the organization owes, such as accounts payable, loans, and other liabilities. Liabilities are also listed in order of maturity, with the most immediate liabilities at the top.

3. Equity - Equity accounts include all the transactions related to the organization's ownership, such as retained earnings, contributions, and other equity-related transactions. Equity accounts help show the organization's financial health and ability to generate profits.

4. Revenue - This category includes all the organization's income, such as sales, grants, and donations. Revenue accounts help to track the organization's sources of income and ensure that all income is properly recorded.

5. Expenses - Accounts in this category include all the organization's costs and expenses, such as salaries, rent, utilities, and office supplies. Expense accounts help track the organization's spending and record all costs correctly.

These five categories are essential for any organization's Chart of Accounts and provide a comprehensive framework for financial reporting. By adequately organizing financial information, organizations can make informed decisions, comply with regulatory requirements, and improve their financial health.

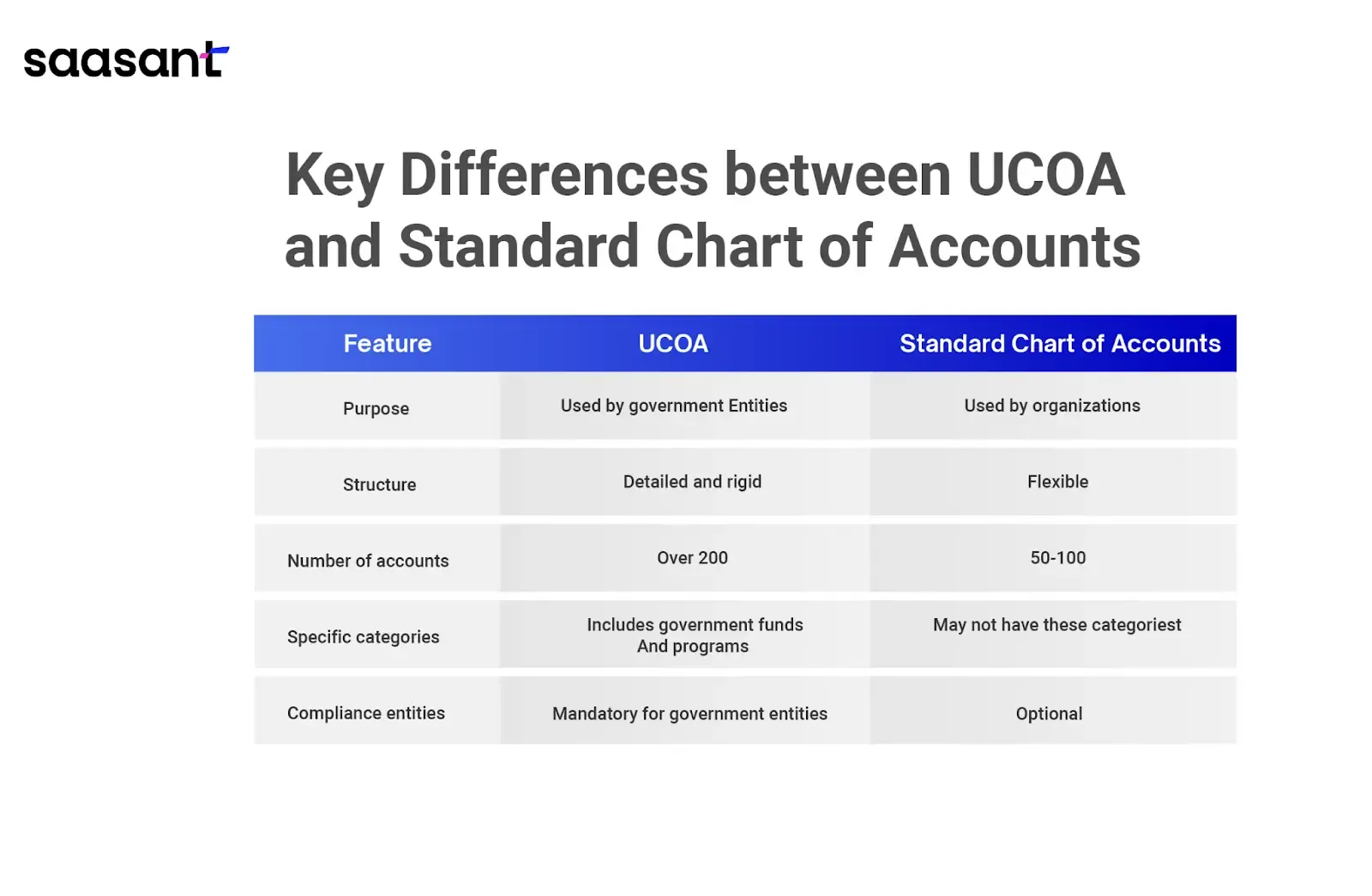

Differences between UCOA and the standard Chart of Accounts

The Uniform Chart of Accounts (UCOA) and a standard Chart of Accounts are both used to organize financial transactions, but there are some notable differences between the two:

Purpose:

Government entities primarily use the UCOA, while organizations across industries use a standard Chart of Accounts.

Structure:

The UCOA has a more detailed and rigid structure than a standard Chart of Accounts. The UCOA has over 200 accounts, while a standard Chart of Accounts typically has between 50 and 100 accounts.

The UCOA includes specific codes and categories for government funds and programs, while a standard Chart of Accounts may not have these categories.

Compliance:

The UCOA is designed to comply with specific government regulations, while a standard Chart of Accounts is not necessarily designed for regulatory compliance.

Compliance with the UCOA is mandatory for government entities, while compliance with a standard Chart of Accounts is optional.

The UCOA is a specialized Chart of Accounts designed for government entities. In contrast, a standard Chart of Accounts is a more general framework that can be adapted to different industries and organizations.

Here is a table to further highlight the differences:

Implementing and Using a Chart of Accounts

How to set up a nonprofit Unified Chart of Accounts in QuickBooks

Setting up a Unified Chart of Accounts in QuickBooks is critical in managing a nonprofit organization's finances. The process involves creating a structured list of accounts that enables the organization to record, categorize, and report its financial transactions accurately.

Let's say a nonprofit organization wants to set up a Unified Chart of Accounts in QuickBooks:

1. They can customize the sample Chart of Accounts provided by QuickBooks to fit their specific needs. For instance, they may add accounts to particular programs or grants, modify account names, and delete irrelevant accounts.

2. They will assign account numbers to accurately identify and categorize each account. They can use a numbering system that reflects each account's category and subcategory.

One could represent assets, 2 for liabilities, 3 for equity, 4 for revenue, and 5 for expenses. The second digit could represent the subcategory within each category, such as 41 for fundraising expenses and 42 for program expenses.

3. They will also establish the account type for each account. QuickBooks provides account types such as assets, liabilities, equity, income, and expenses. For example, they may assign "Cash" as an asset account, "Accounts Payable" as a liability account, "Retained Earnings" as an equity account, "Donations" as a revenue account, and "Salaries" as an expense account.

4. They will set up sub-accounts to provide more detailed information on how funds are spent and earned. For instance, they can set up subaccounts for "Salaries" such as "Executive Director Salaries" and "Program Staff Salaries."

5. They can create rules for each account in the Chart of Accounts to set up default values and preferences, such as tax codes, payment terms, and payment methods.

They may set up a default tax code of "Exempt" for donations, a payment term of "Net 30" for accounts payable, and a payment method of "Check" for all expenses.

6. Finally, they will assign account numbers and types to each transaction entered into QuickBooks to ensure accurate recording and reporting.

When they receive a donation, they assign it to the "Donations" revenue account, including 4100. When they pay for salaries, they assign it to the "Salaries" expense account and include the account number 5200.

Also read:

How to download Chart of Accounts from QuickBooks

How to implement a Unified Chart of Accounts in QuickBooks

Implementing a Unified Chart of Accounts in QuickBooks can benefit nonprofit organizations by providing a standardized framework for tracking financial transactions. Here are some steps to follow when implementing a Unified Chart of Accounts in QuickBooks:

![chart of accounts]-37.webp](https://images.saasant.info/chart_of_accounts_37_84cc42a445.webp)

1. Define the organization's financial reporting needs: Determine the specific information to be tracked to meet financial reporting requirements. It includes identifying the accounts that must be included in the Chart of Accounts.

2. Create the Chart of Accounts: Once the reporting needs have been identified, create a customized Chart of Accounts that meets those needs. It includes defining account categories and subcategories, assigning account numbers, and setting up the Chart of Accounts in QuickBooks.

3. Train staff: Train staff members responsible for recording financial transactions on how to use the Chart of Accounts effectively. It includes understanding account categories and subcategories, selecting the appropriate account for each transaction, and accurately recording transactions in QuickBooks.

4. Establish policies and procedures: Develop policies and procedures for using the Chart of Accounts consistently throughout the organization. It includes guidelines for recording transactions, ensuring the accuracy and completeness of data, and monitoring compliance with regulatory requirements.

5. Regularly review and update the Chart of Accounts: It is essential to review and update the Chart of Accounts to ensure it remains accurate and relevant to the organization's financial reporting needs.

Implementing a Unified Chart of Accounts in QuickBooks can help nonprofit organizations streamline their financial management and improve their reporting accuracy. By tracking financial transactions standardized, nonprofit organizations can quickly generate reports and comply with regulatory requirements.

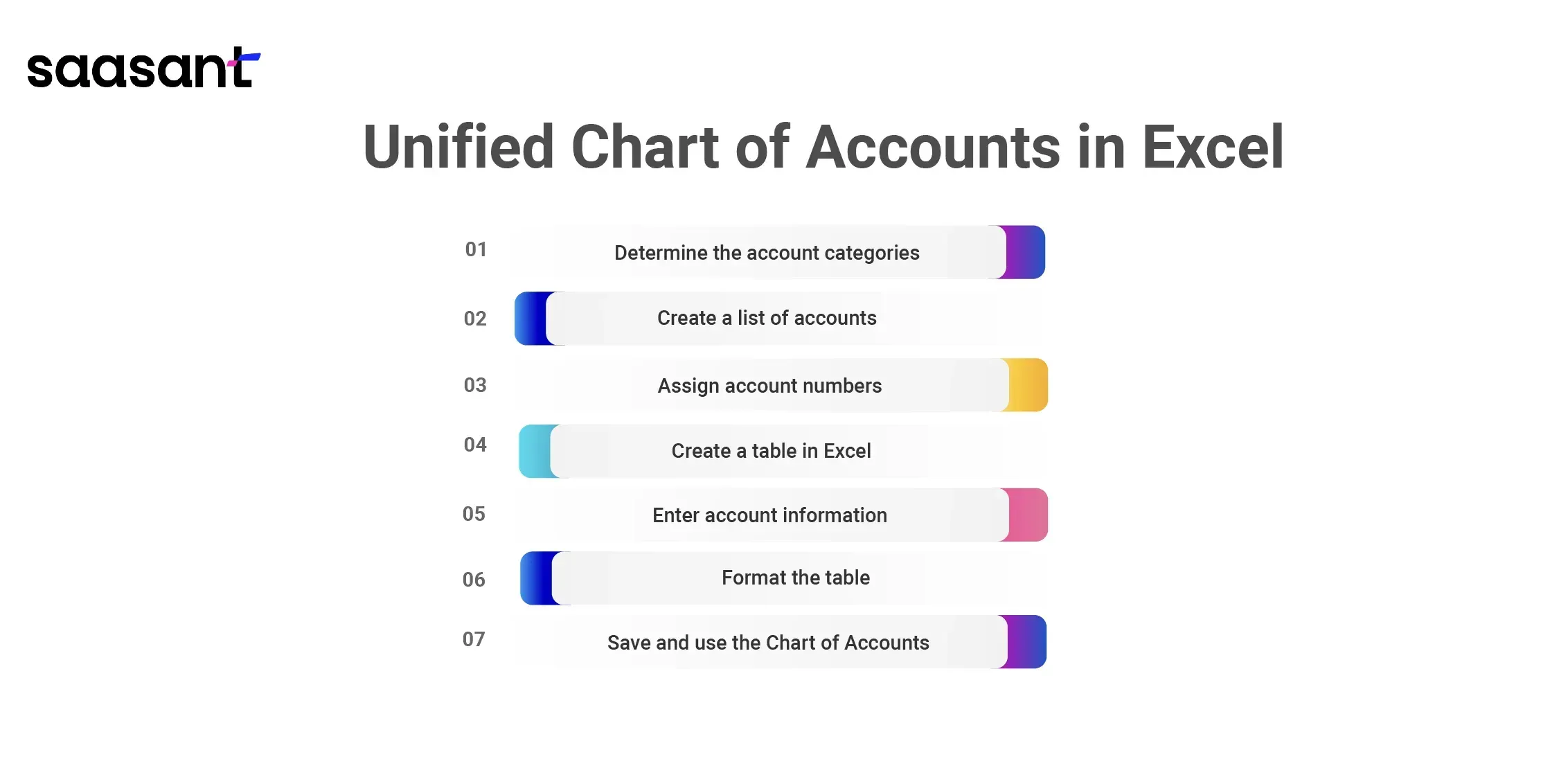

Unified Chart of Accounts in Excel

Excel is a popular tool for managing financial information and can also be used to create a Unified Chart of Accounts. To implement a Unified Chart of Accounts in Excel, follow these steps:

Creating a Unified Chart of Accounts in Excel can be done by following these steps:

1. Determine the account categories: Start by determining the categories of accounts included in the chart. Common categories include assets, liabilities, equity, revenue, and expenses.

2. Create a list of accounts: For each category, create a list of accounts that will be included. Be sure to use clear and descriptive names for each account.

3. Assign account numbers: Assign a unique account number to each account on the list. A standard numbering system uses a four-digit number, with the first two digits representing the account category and the second two representing the specific account within that category.

4. Create a table in Excel: Open a new Excel workbook and create a table with columns for account number, name, and category. You can also include additional columns for account descriptions or other relevant information.

5. Enter account information: Enter the account information into the table, including the account number, name, and category. Be sure to use consistent formatting and data validation to ensure data accuracy.

6. Format the table: Format the table to make it easy to read and navigate. You can use conditional formatting to highlight specific account categories or add filters to allow for sorting and searching.

7. Save and use the Chart of Accounts: Save the Chart of Accounts as a separate Excel file or worksheet and use it as a reference when recording transactions in your accounting software.

Using Excel for a Unified Chart of Accounts can be cost-effective for smaller organizations or those with limited financial management needs. However, it may provide a different level of functionality or integration with other systems than dedicated accounting software like QuickBooks.

Intuit Unified Chart of Accounts for Nonprofits

Intuit, the company behind QuickBooks, has developed a standardized Chart of Accounts for nonprofits. The Intuit Unified Chart of Accounts for Nonprofits includes over 100 account codes organized into six categories: assets, liabilities, net assets, revenue, expenses, and functional expenses.

Using the Intuit Unified Chart of Accounts for Nonprofits provides several benefits, including:

1. Compliance with regulatory reporting requirements.

2. Consistency in financial reporting across the nonprofit sector.

3. Ease of use and compatibility with QuickBooks Online and other financial management tools.

Nonprofits can customize the Intuit Unified Chart of Accounts to meet their needs, but the standard chart provides a solid financial reporting and management foundation.

Unified Chart of Accounts and Technology Expenses

With the increasing use of technology in nonprofits, it is essential to have a separate category for technology expenses in the Chart of Accounts. This category should include subcategories for software, hardware, and related costs.

By tracking technology expenses separately, nonprofits can analyze their technology spending, identify opportunities to reduce costs and ensure that technology spending is aligned with organizational goals.

Additionally, a separate category for technology expenses makes it easier to prepare financial reports and comply with regulations. Nonprofits can use the Unified Chart of Accounts to track technology expenses and ensure they are appropriately recorded in their financial statements.

Which category do bank fees belong to in the Unified Chart of Accounts

Bank fees are typically classified as expenses and should be included in the Chart of Accounts under the operating expenses category. The specific account to use may depend on the nature of the bank fees, but it could be labeled as "Bank Fees" or "Bank Charges."

In a Unified Chart of Accounts, the account number for bank fees should be determined based on the numbering system adopted by the organization, which should be consistent and well-defined.

The account number should also align with the Chart of Accounts hierarchy and be grouped with other accounts with similar characteristics. It helps to maintain consistency and ensure accurate financial reporting.

Fund Accounting Chart of Accounts

Fund accounting is a specialized accounting system used by nonprofits to track and manage funds for specific purposes. The fund accounting Chart of Accounts includes a separate category for each fund and subcategories for revenues, expenses, assets, and liabilities related to each fund.

Nonprofits use the fund accounting Chart of Accounts to track how funds are spent and ensure that they are used in compliance with donor restrictions. It helps organizations demonstrate accountability and transparency to donors and stakeholders. Fund accounting also simplifies financial reporting by enabling nonprofits to prepare separate financial statements for each fund.

Essential elements of a Chart of Accounts

A Chart of Accounts is crucial to a company's financial infrastructure. It provides a comprehensive list of all the accounts used to record financial transactions and facilitates the preparation of financial statements, tax returns, and audits. The following are essential elements of a Chart of Accounts:

1. Account code: Each account has a unique code number that identifies it within the Chart of Accounts. The code number allows for easy and accurate tracking of transactions.

2. Account name: A clear and concise name for each account that accurately describes its purpose is essential. It ensures that the account is easily identifiable and understandable to all users.

3. Account type: Accounts are categorized into assets, liabilities, equity, revenue, and expenses, determined by financial characteristics. This categorization allows for quick identification and easy grouping of accounts.

4. Account balance: The balance of each account is critical in determining the financial position of an organization. The balance can be positive or negative, indicating whether the account represents an asset or liability.

5. Sub-accounts: Sub-accounts provide further detail and break down an account into smaller components. It enables organizations to track transactions more granularly, which is helpful for budgeting and financial reporting.

6. Restrictions: If an account has any restrictions, such as donor restrictions or regulatory requirements, they should be clearly identified and tracked separately.

7. Hierarchy: A Chart of Accounts should be organized in a hierarchical structure to make it easy to navigate and understand. This hierarchy may be based on account type or other relevant factors.

Summing it Up

The Unified Chart of Accounts (UCOA) is a valuable tool for nonprofits to manage their finances and communicate financial information to stakeholders effectively. By implementing the UCOA, nonprofits can standardize their financial reporting and improve transparency and accountability.

SaasAnt Transactions provides an easy-to-use feature for importing financial transactions, like Chart of Accounts, into popular accounting software such as QuickBooks and Xero.

Utilizing this software solution can help nonprofits streamline their financial management processes and leverage the benefits of the Unified Chart of Accounts maximally.

FAQs

What is the power of the Chart of Accounts?

The power of the Chart of Accounts lies in its ability to provide structure and organization to an organization's financial information. It allows for easy classification and grouping of financial transactions, facilitating accurate and timely financial reporting.

Why do we use the Chart of Accounts?

We use a Chart of Accounts to organize financial transactions and create a structure for financial reporting. It provides a systematic way to categorize transactions, which makes it easier to analyze financial data and prepare financial statements.

A Chart of Accounts also helps to ensure that financial records are accurate and consistent and facilitates compliance with accounting standards and regulations.

What is a Chart of Accounts template?

A Chart of Accounts template is a pre-designed framework that provides a standardized structure for organizing and categorizing financial transactions. The template typically includes a predefined set of account codes, names, descriptions, and guidelines on how to use the Chart of Accounts effectively.

This template can save time and effort in setting up a new Chart of Accounts and ensure consistency in financial reporting across organizations.

Three critical features of a Chart of Accounts

The three essential features of a Chart of Accounts are:

1. Consistency - A Chart of Accounts should provide a consistent framework for categorizing financial transactions across an organization. It ensures that financial reports are accurate, comparable, and can be used for decision-making.

2. Flexibility - A Chart of Accounts should be flexible enough to accommodate changes in the organization's financial structure, such as adding new accounts or changes in account names and codes.

3. Relevance - A Chart of Accounts should be relevant to the organization's financial reporting needs and comply with regulatory requirements. It means that accounts should be structured to reflect the organization's operations and financial transactions.

What is the Unified Chart of Accounts (UCOA), and why is it crucial for nonprofits?

The UCOA is a standardized list of account codes developed by the Financial Accounting Standards Board (FASB) in the 1990s. It plays a vital role in organizing and tracking financial transactions, ensuring consistency in reporting, transparency, and accountability for nonprofits.

How does the UCOA benefit nonprofit organizations beyond consistency and comparability?

The UCOA offers advantages such as better financial decision-making, improved transparency, increased cost savings, enhanced communication between departments, and facilitates efficient auditing processes.

What are the specific features and history of the UCOA?

The UCOA, with over 200 accounts, was developed by FASB to standardize financial reporting. It provides a uniform method of recording and reporting financial information, simplifying the preparation of financial statements.

How does the UCOA comply with regulatory requirements, and what are its benefits for auditing?

The UCOA is designed to comply with specific government regulations, making auditing more efficient. Its structured format enables auditors to review financial data, reducing time and effort in the auditing process.

What are the essential elements of a Chart of Accounts, and how do they contribute to effective financial management?

The elements include account code, name, type, balance, sub-accounts, restrictions, and hierarchy. These elements help accurately track transactions, provide a clear financial position, and ensure compliance and transparency.