What Are Non-Depreciable Assets?

In finance and accounting, depreciation is pivotal in allocating the cost of assets over their useful lives. It's a fundamental principle that helps businesses accurately reflect the value of their assets on financial statements and navigate tax obligations. Understanding depreciation is essential for any business owner or financial professional, but equally crucial is comprehending which assets can and cannot be depreciated.

Contents

Definition of Depreciation

Importance of Understanding Depreciable Assets

Definition and Purpose of Depreciation: Maximizing Asset Value

Assets That Can Be Depreciated

Assets That Cannot Be Depreciated

Types of Non-Depreciable Assets

Alternatives to Depreciation for Non-Depreciable Assets

Importance of Proper Asset Classification

Conclusion

FAQs

Definition of Depreciation

Simply put, depreciation allocates the cost of tangible assets over their useful lives. This accounting method acknowledges that assets such as machinery, equipment, and buildings gradually lose value over time due to wear and tear, obsolescence, or other factors. By spreading out the cost of these assets over their expected lifespan, businesses can more accurately reflect their actual economic value on financial statements.

Importance of Understanding Depreciable Assets

Knowing which assets can and cannot be depreciated is paramount for several reasons. Firstly, it ensures compliance with accounting standards and tax regulations, preventing potential errors or discrepancies in financial reporting. Secondly, it enables businesses to make informed asset management, capital budgeting, and tax planning decisions, whether optimizing depreciation deductions for tax purposes or evaluating the actual cost of long-term investments; a solid understanding of depreciation is indispensable for sound financial management.

This article delves into the often-overlooked realm of assets that cannot be depreciated. While depreciation is expected for tangible assets with determinable valuable lives, certain assets fall outside this scope. We'll explore the characteristics of these non-depreciable assets, why they are excluded from depreciation, and alternative accounting treatments. By shedding light on this topic, we aim to equip business owners, finance professionals, and aspiring accountants with the knowledge to navigate the complexities of asset classification and financial reporting.

Join us as we unravel the mystery of non-depreciable assets and uncover the nuances of accounting for these vital business operations components. Understanding the intricacies of depreciation and asset classification is not just about compliance—it's about empowering businesses to make informed financial decisions and thrive in today's dynamic economic landscape.

Definition and Purpose of Depreciation: Maximizing Asset Value

In finance and accounting, depreciation is a cornerstone concept that is pivotal for accurately reflecting the value of assets over time. Let's delve into what depreciation entails, its significance for financial reporting and tax obligations, and the various methods used to calculate it.

Explanation of Depreciation

Depreciation is a systematic method used to allocate the cost of tangible assets over their useful life. When businesses invest in assets like machinery, equipment, or buildings, they recognize that these assets gradually lose value due to wear and tear, technological advancements, or other factors. Depreciation acknowledges this decrease in value and spreads out the asset's cost over its expected lifespan, reflecting a more accurate representation of its value on financial statements.

Importance of Depreciation for Financial Reporting and Tax Purposes

Depreciation plays a crucial role in both financial reporting and tax planning. For financial reporting purposes, depreciation helps businesses accurately depict their financial health by matching the cost of assets with the revenues they generate over time. This ensures that the income statement reflects the actual cost of using assets to generate revenue, improving the accuracy of financial statements and facilitating better decision-making for investors, creditors, and other stakeholders.

Moreover, depreciation is instrumental in tax planning as it allows businesses to deduct the cost of assets over time, reducing taxable income and lowering tax liabilities. By utilizing depreciation deductions, companies can optimize their tax strategy, maximize cash flow, and improve profitability. However, adhering to tax regulations and depreciation guidelines is essential to avoid potential compliance issues or audit risks.

Overview of Different Depreciation Methods

Several methods are used to calculate depreciation, each with advantages, disadvantages, and applicability to different types of assets. Two standard methods include:

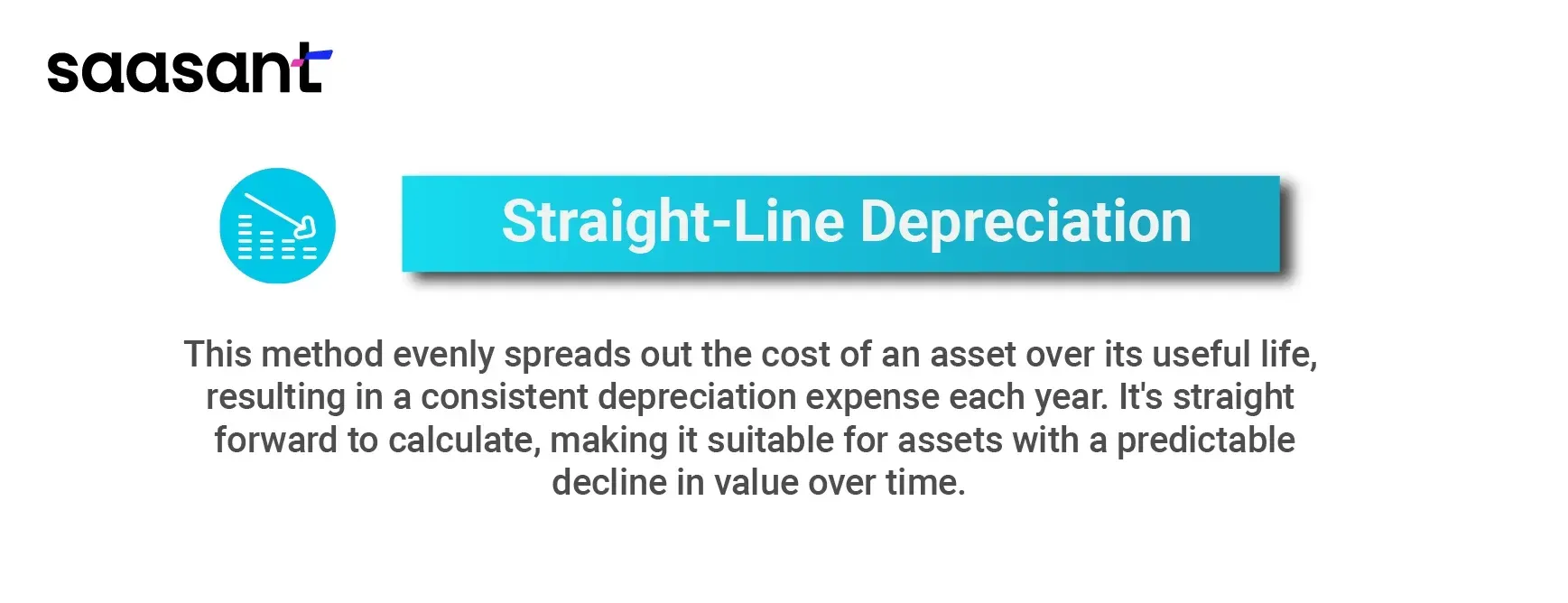

Straight-Line Depreciation: This method evenly spreads out the cost of an asset over its useful life, resulting in a consistent depreciation expense each year. It's straightforward to calculate, making it suitable for assets with a predictable decline in value over time.

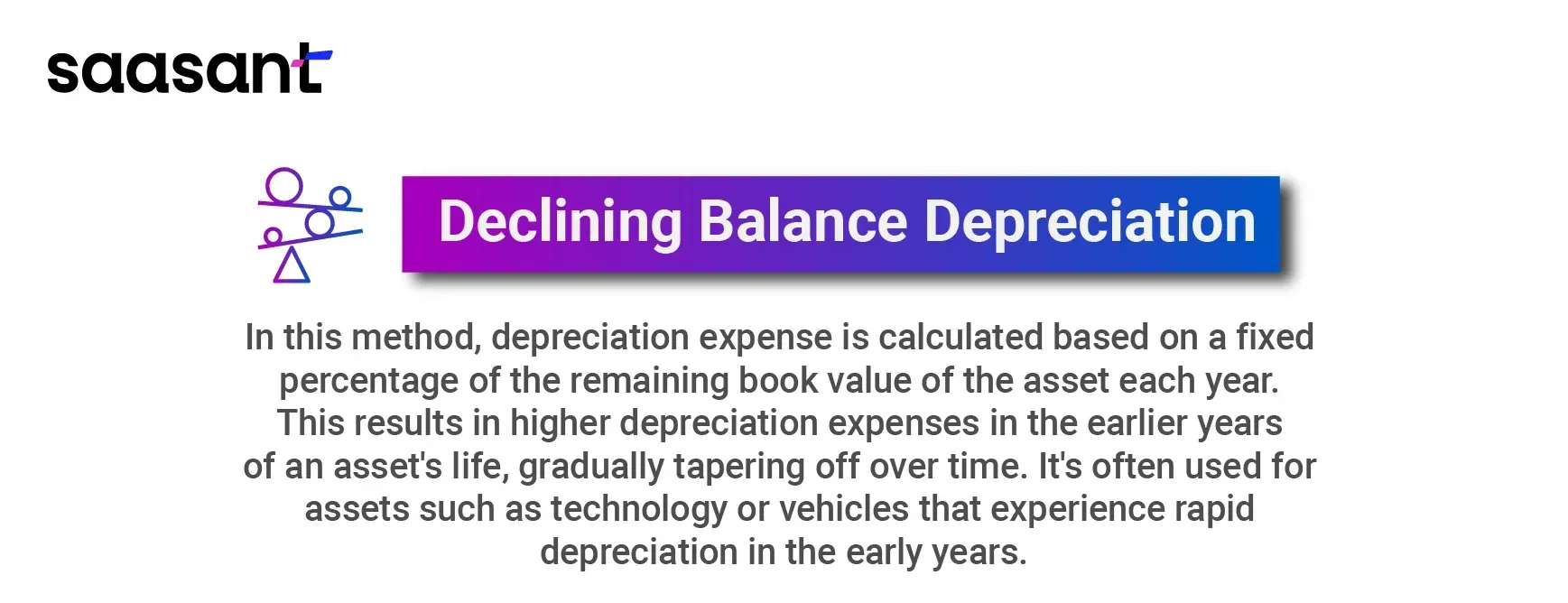

Declining Balance Depreciation: In this method, depreciation expense is calculated based on a fixed percentage of the remaining book value of the asset each year. This results in higher depreciation expenses in the earlier years of an asset's life, gradually tapering off over time. It's often used for assets such as technology or vehicles that experience rapid depreciation in the early years.

Understanding the nuances of these depreciation methods is essential for businesses to accurately reflect their assets' value, comply with accounting standards, and optimize tax planning strategies.

Assets That Can Be Depreciated

Depreciable assets are crucial in business financial management, influencing everything from budgeting to tax liabilities. This article aims to understand the types of assets eligible for depreciation and amortization and provides insights into the depreciation process and its impact on financial statements.

Tangible Assets Eligible for Depreciation:

Tangible assets encompass physical assets with a determinable lifespan and can depreciate over time. Examples include machinery, vehicles, buildings, furniture, and equipment. These assets are integral to business operations but undergo wear and tear or obsolescence, decreasing value over time. By depreciating tangible assets, businesses can accurately reflect their diminishing value on financial statements, aligning with accounting principles and providing stakeholders with an accurate picture of asset value.

Overview of Intangible Assets Eligible for Amortization:

Though lacking physical presence, intangible assets hold significant value for businesses. Examples include patents, copyrights, trademarks, goodwill, and software. While intangible assets do not depreciate traditionally, they undergo amortization. Amortization spreads the cost of intangible assets over their useful life, reflecting their diminishing value over time. This allows businesses to accurately account for the consumption of intangible assets and assess their impact on profitability and financial health.

Explanation of the Depreciation Process and its Financial Statement Impact:

Depreciation involves several key steps, including determining an asset's useful life and salvage value. Various depreciation methods exist, including straight-line, declining balance, and units of production, each suited to different asset types and business requirements. Depreciation expenses are recorded on the income statement, reducing net income and taxable income, while accumulated depreciation is recorded on the balance sheet, offsetting the asset's original cost. This reflects the declining value of assets over time, providing stakeholders with accurate financial information and aiding in decision-making processes.

Understanding the concept of depreciable assets, both tangible and intangible, is essential for effective financial management. By incorporating depreciation and amortization into financial reporting, businesses can accurately portray the value of their assets, assess profitability, and make informed decisions about asset management and investment. Moreover, transparent and accurate financial statements enhance stakeholder confidence and trust, fostering long-term success and sustainability for businesses.

Assets That Cannot Be Depreciated

Not all assets are subject to depreciation in finance and accounting. Understanding which assets fall into this category is essential for accurate financial reporting and decision-making. This article aims to illuminate assets that cannot be depreciated, providing insights into their nature, characteristics, and business implications.

Definition and Explanation of Assets Not Subject to Depreciation:

Non-depreciable assets are those that do not experience a decrease in value over time due to wear and tear, obsolescence, or expiration. Unlike depreciable assets with a finite useful life, non-depreciable assets retain their value or appreciate over time. These assets are typically long-term investments that contribute to a company's growth and value proposition without diminishing in value on financial statements.

Overview of Assets Typically Excluded from Depreciation:

Several categories of assets are commonly excluded from depreciation calculations. These include land, investments such as stocks and bonds, and inventory. Land, for example, has an indefinite useful life and does not experience physical deterioration, making it ineligible for depreciation. Similarly, investments represent financial instruments with fluctuating values based on market conditions rather than physical assets subject to wear and tear. While essential for business operations, inventory is considered a current asset and is accounted for differently from depreciable assets.

Explanation of Why Certain Assets Cannot Be Depreciated:

Assets that cannot be depreciated typically fall into one of two categories: those with an indefinite useful life and those that do not undergo physical deterioration. Land, for instance, is considered to have an indefinite useful life, as it does not wear out or become obsolete over time. On the other hand, investments derive their value from market conditions and economic factors rather than physical attributes, making them unsuitable for depreciation. While subject to depletion or obsolescence, inventory is classified as a current asset and is expensed through the cost of goods sold rather than depreciated.

Non-depreciable assets play a crucial role in the financial landscape of businesses, representing long-term investments and strategic assets that contribute to growth and value creation. By understanding the characteristics of these assets and their exclusion from depreciation calculations, businesses can accurately portray their financial position and make informed decisions about resource allocation and investment strategies. Moreover, transparent and accurate financial reporting enhances stakeholder confidence and trust, fostering long-term success and sustainability for businesses.

Types of Non-Depreciable Assets

Certain assets defy the conventional rules of depreciation in the intricate finance landscape. Understanding the nuances of these non-depreciable assets is crucial for accurate financial reporting and strategic decision-making. This article delves into the different types of non-depreciable assets, highlighting their characteristics and implications for businesses.

Land as a Non-Depreciable Asset:

Land is a prime example of a non-depreciable asset. Unlike buildings or machinery, land does not deteriorate over time due to wear and tear. Its value typically appreciates or remains stable, making it ineligible for depreciation. Land holds intrinsic value and is often a cornerstone of real estate investments. Its enduring nature makes it a secure and valuable asset for businesses and investors, from prime commercial lots to sprawling agricultural land.

Investments and Securities Exempt from Depreciation:

Investments and securities represent another category of assets exempt from depreciation. These financial instruments, including stocks, bonds, and mutual funds, derive value from market fluctuations and economic conditions rather than physical deterioration. While their market value may fluctuate over time, they are not subject to depreciation in the traditional sense. Instead, their valuation reflects broader market dynamics and investor sentiment, making them integral components of diversified investment portfolios.

Inventory and its Treatment in Financial Accounting:

While subject to depletion or obsolescence, financial accounting typically does not depreciate inventory. Instead, it is treated as a current asset and expensed through the cost of goods sold (COGS) when sold or used in production. Inventory management is essential for businesses to optimize working capital and maintain efficient operations. While inventory may decline in value over time due to spoilage or technological obsolescence, it is not depreciated on financial statements like long-term assets.

Non-depreciable assets encompass diverse valuable resources that defy the conventional depreciation model. From land holdings to financial investments and inventory, these assets play vital roles in businesses' growth and value-creation strategies. By understanding the distinct characteristics and treatment of non-depreciable assets, companies can enhance their financial reporting accuracy and make informed decisions about resource allocation and investment strategies. Moreover, transparent and reliable financial reporting fosters stakeholder confidence and trust, paving the way for long-term success and sustainability in today's dynamic business environment.

Alternatives to Depreciation for Non-Depreciable Assets

In finance, not all assets follow the traditional path of depreciation. Non-depreciable assets, such as land and certain investments, require alternative accounting methods to reflect their value accurately. This article delves into alternative approaches for accounting for non-depreciable assets, offering insights into impairment testing, investment valuation, and inventory management strategies.

Explanation of Alternative Methods for Accounting Non-Depreciable Assets:

For assets like land and investments, alternative accounting methods are employed to reflect changes in their value over time. One such method is revaluation, where assets are periodically assessed to adjust their carrying value based on current market prices. Revaluation ensures that the balance sheet accurately reflects the true worth of these assets, providing stakeholders with a more realistic view of the organization's financial position. Additionally, non-depreciable assets may undergo impairment testing to assess whether their carrying value exceeds their recoverable amount, necessitating adjustments to reflect any impairments in their value.

Overview of Impairment Testing for Long-Lived Assets with Indefinite Useful Lives:

Long-lived assets with indefinite useful lives, such as goodwill and certain intangible assets, are subject to impairment testing to ensure their carrying value aligns with their recoverable amount. Impairment testing involves comparing the asset's carrying value to its fair value or value in use, with any excess indicating impairment. For example, goodwill acquired through business combinations is tested for impairment annually or whenever there are indicators of potential impairment, such as adverse economic conditions or declining cash flows. By conducting impairment testing, organizations can prevent overstatement of asset values and maintain the accuracy of their financial statements.

Discussion of Accounting Treatments for Investments and Inventory:

While not subject to depreciation, investments and inventory require careful accounting treatments to reflect changes in value and usage. Investments in equity securities are typically measured at fair value, with changes in value recognized in the income statement. Similarly, investments in debt securities may be classified as held-to-maturity, available-for-sale, or trading securities, each with distinct accounting treatments. Conversely, inventory is valued at a lower cost or net realizable value, ensuring conservative valuation and prudent financial reporting.

Non-depreciable assets pose unique challenges for financial accounting, requiring alternative methods to reflect their value and usage accurately. From revaluation and impairment testing to specialized accounting treatments for investments and inventory, organizations must adopt appropriate strategies to maintain transparency and reliability in their financial reporting. By effectively understanding and implementing these alternative accounting methods, businesses can enhance stakeholder confidence, facilitate informed decision-making, and navigate the complexities of today's dynamic financial landscape with clarity and precision.

Importance of Proper Asset Classification

Proper asset classification is paramount for businesses to accurately represent their financial health, meet regulatory requirements, and optimize tax liabilities. This article explores the significance of accurate asset classification, highlighting its impact on financial reporting, tax liabilities, and the role of accountants and financial professionals in maintaining compliance.

Impact of Misclassifying Assets on Financial Reporting and Tax Liabilities:

Misclassification of assets can significantly distort financial statements and mislead stakeholders about an organization's actual financial position. For instance, misclassifying a long-term investment as a current asset may inflate liquidity ratios, leading to erroneous assessments of a company's short-term solvency. Moreover, improper asset classification can distort tax liabilities, potentially resulting in underpayment or overpayment of taxes. Failure to accurately classify assets may trigger audits, penalties, and legal repercussions, undermining the organization's financial integrity and reputation.

Overview of the Role of Accountants and Financial Professionals in Asset Classification:

Accountants and financial professionals ensure accurate asset classification through diligent record-keeping, adherence to accounting standards, and thorough asset characteristics analysis. They classify assets based on their nature, intended use, and expected economic benefits, considering helpful life, depreciation methods, and regulatory requirements. By employing their expertise and leveraging accounting software and tools, these professionals help organizations maintain compliance with financial reporting standards and mitigate the risks associated with misclassification.

Importance of Adhering to Accounting Standards and Regulations:

Adhering to accounting standards and regulations is essential for fostering transparency, consistency, and comparability in financial reporting. Standards such as Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) provide guidelines for asset classification, ensuring uniformity and accuracy across industries and jurisdictions. Compliance with these standards enhances the credibility of financial statements, instills investor confidence, and facilitates informed decision-making by stakeholders. Adherence to regulatory requirements also mitigates the risk of penalties, sanctions, and reputational damage, safeguarding the organization's financial integrity and sustainability.

Proper asset classification is a cornerstone of effective financial management, with far-reaching implications for financial reporting, tax liabilities, and regulatory compliance. Accurate classification ensures transparency, reliability, and adherence to accounting standards, bolstering stakeholder confidence and enabling informed decision-making. Accountants and financial professionals are pivotal in maintaining compliance with classification standards, leveraging their expertise to navigate complex asset structures and regulatory frameworks. Organizations can enhance financial transparency, mitigate risks, and sustain long-term economic health in an increasingly competitive and regulated business environment by prioritizing accurate asset classification and adhering to accounting standards and regulations.

Conclusion

In the intricate finance and accounting world, proper asset classification is a guiding beacon for businesses navigating their financial journey. As we conclude our exploration of the mysteries surrounding non-depreciable assets, it's imperative to recap the key insights and emphasize the significance of understanding which assets can and cannot be depreciated.

Recap of Key Points Covered:

Throughout this article, we've unraveled the complexities of non-depreciable assets, shedding light on their characteristics, implications, and alternative accounting treatments. Each asset category, from land holdings to investments and inventory, presents unique challenges and considerations for accurate financial reporting and strategic decision-making.

Significance of Understanding Depreciable Assets:

Understanding which assets can and cannot be depreciated is not merely an academic exercise; it's a fundamental aspect of financial management with profound implications for business operations, compliance, and stakeholder trust. Accurate asset classification ensures transparency, reliability, and adherence to accounting standards, enabling businesses to make informed decisions about resource allocation, investment strategies, and tax planning.

Encouragement for Further Consultation:

While this article provides valuable insights into non-depreciable assets, the complexities of asset classification may require additional guidance from accounting professionals. We encourage readers to consult with experienced accountants and financial advisors to navigate the nuances of asset classification, ensure compliance with regulatory requirements, and optimize financial performance.

In conclusion, proper asset classification is not just a matter of compliance—it's a strategic imperative for businesses seeking to thrive in today's dynamic economic landscape. By understanding the intricacies of asset depreciation, non-depreciable assets, and alternative accounting treatments, organizations can enhance their financial transparency, mitigate risks, and lay the foundation for sustainable growth and success. Let's continue to unlock the mysteries of asset classification, empowering businesses to navigate the complexities of finance with confidence and clarity.

If you want to learn more about finding marginal cost, check out this guide how to find marginal cost.

FAQs

What is depreciation, and why is it important?

Depreciation is allocating the cost of tangible assets over their useful lives. It's crucial because it helps businesses accurately reflect the value of their assets on financial statements and navigate tax obligations.

Why is understanding which assets can and cannot be depreciated essential?

Understanding which assets can and cannot be depreciated ensures compliance with accounting standards and tax regulations, prevents errors in financial reporting, and enables informed asset management and tax planning decisions.

What are some examples of depreciable assets?

Depreciable assets include machinery, equipment, buildings, vehicles, furniture, and intangible assets like patents and copyrights.

Can you explain why land is considered a non-depreciable asset?

Land is considered a non-depreciable asset because it does not deteriorate over time due to wear and tear. Its value typically appreciates or remains stable, making it ineligible for depreciation.

What are some examples of non-depreciable assets?

Land, investments such as stocks and bonds, and inventory are examples of non-depreciable assets. These assets retain their value or appreciate over time and are not subject to traditional depreciation.

How are non-depreciable assets accounted for in financial reporting?

Non-depreciable assets may be accounted for through alternative methods such as revaluation, impairment testing, or specialized accounting treatments for investments and inventory.

What is the role of accountants and financial professionals in asset classification?

Accountants and financial professionals are crucial in ensuring accurate asset classification through diligent record-keeping, adherence to accounting standards, and asset characteristics analysis.

Why is adherence to accounting standards and regulations essential for asset classification?

Adherence to accounting standards and regulations ensures transparency, consistency, and comparability in financial reporting, enhancing the credibility of financial statements and facilitating informed decision-making by stakeholders.

How can businesses optimize financial performance through accurate asset classification?

Accurate asset classification enables businesses to make informed decisions about resource allocation, investment strategies, and tax planning, ultimately enhancing financial transparency and mitigating risks.

Where can I seek further guidance on asset classification and depreciation?

For further guidance on asset classification and depreciation, it's recommended to consult experienced accountants and financial advisors who can provide tailored advice based on specific business needs and circumstances.