What Effect Does Revenue Have on Retained Earnings?

Retained earnings are crucial to any company's financial statements, providing critical insights into its profitability and growth potential. Retained earnings represent the portion of a company's net income that is retained rather than distributed as dividends. This accumulated amount is vital for reinvesting in the business, funding expansion, and maintaining financial stability. For investors and analysts, retained earnings are a significant indicator of a company’s financial health and capacity to generate sustainable profits over time.

A fundamental relationship exists between revenue and retained earnings. Revenue, or the income generated from the sale of goods or services, plays a pivotal role in determining the overall growth of retained earnings. When revenue increases, it directly influences the company's net income, subsequently increasing retained earnings after deducting expenses, taxes, and dividends. This link highlights the importance of effective revenue generation strategies and their long-term impact on a company’s financial standing.

Understanding how revenue affects retained earnings is essential for anyone involved in financial management or analysis. By monitoring this dynamic, businesses can make informed decisions about resource allocation, investment, and dividend distribution. In the following sections, we will explore this relationship in more detail, shedding light on how companies can leverage revenue growth to boost their retained earnings and enhance their financial stability.

Contents

Understanding Retained Earnings: Definition, Role, and Key Components

Critical Components of Retained Earnings

Defining Revenue and Its Role in Business: A Key Driver of Financial Performance

The Relationship Between Revenue and Retained Earnings: Understanding the Financial Impact

The Role of Dividends in Retained Earnings: Impact on Financial Growth and Stability

How Revenue Affects Retained Earnings? A Real-World Example

Why Understanding the Effect of Revenue on Retained Earnings Matters?

Key Factors That Can Influence Retained Earnings Beyond Revenue

Common Mistakes to Avoid When Calculating Retained Earnings

FAQs

Understanding Retained Earnings: Definition, Role, and Key Components

Retained earnings represent the cumulative amount of a company’s net income retained in the business rather than paid out as dividends to shareholders. It is a critical financial metric, typically found on the balance sheet under the equity section, indicating the portion of earnings the company has reinvested in its operations or used to pay down debt. Retained earnings are the profits a company reinvests in its growth rather than distributing to its shareholders.

Critical Components of Retained Earnings

The calculation of retained earnings involves two key components: net income and dividends.

Net Income: This represents the company's total earnings after accounting for all expenses, taxes, and interest. Net income is the starting point in calculating retained earnings, reflecting a company's profitability over a specific period. The higher the net income, the greater the potential for retained earnings to increase.

Dividends: These are payments made to shareholders out of the company’s profits. Dividends reduce the retained earnings because they represent a distribution of earnings to shareholders rather than reinvestment into the company. Companies that aim to reinvest in their business typically pay out a smaller portion of their profits in dividends, allowing more to be retained for growth and expansion.

The Role of Retained Earnings in the Balance Sheet

On the balance sheet, retained earnings contribute to the shareholders' equity section, reflecting the portion of equity that has been reinvested in the business over time. The retained earnings balance provides insight into a company's financial health, reflecting how well it has managed its profits and how much it has accumulated for future growth. A consistent increase in retained earnings over time is often viewed as a sign of a well-managed company with solid earnings potential.

How do Retained Earnings Reflect a Company’s Ability to Reinvest Profits?

Retained earnings serve as a direct indicator of a company’s ability to reinvest profits back into the business. A higher retained earnings balance suggests that the company is maintaining a significant portion of its earnings, which can be used for various growth-related purposes, such as funding capital expenditures, expanding operations, or reducing debt. This reinvestment is crucial for companies looking to scale their operations and enhance shareholder value over the long term.

The retained earnings formula can be expressed as:

By tracking the retained earnings formula, businesses can monitor their ability to reinvest and ensure that profits are effectively utilized for growth rather than being excessively distributed to shareholders.

Defining Revenue and Its Role in Business: A Key Driver of Financial Performance

Revenue is the total income generated by a company from its primary business activities, such as selling goods or services. Often referred to as ‘sales�’ or ‘turnover,’ revenue is one of the most critical indicators of a company’s financial performance and is a fundamental component in assessing its growth potential and operational efficiency. Revenue is recorded at the top of a company’s income statement and serves as the starting point for determining profitability. Without a steady revenue stream, businesses would struggle to cover operating expenses, invest in growth, or return profits to shareholders.

Types of Revenue

Revenue can be broadly classified into two types: operating revenue and non-operating revenue. Understanding these categories is crucial for interpreting a company's financial health and its primary sources of income.

Operating Revenue: Operating revenue is the income generated from a company's core business activities, such as selling products or services. For example, a retail company's revenue from selling merchandise is considered operating revenue. Operating revenue is essential for assessing the company’s ability to sustain and grow its business over time, reflecting its capacity to generate income directly from its primary operations.

Non-Operating Revenue: Non-operating revenue refers to income generated from activities not part of the company’s core operations. This can include gains from investments, interest income, rental income, or one-time sales of assets. While non-operating revenue can contribute to a company's overall financial performance, it does not provide the same long-term growth potential as operating revenue. Non-operating income is typically considered less reliable for evaluating ongoing business success.

How does Revenue Affect Finances?

Revenue is critical in shaping a company's financial health and ability to sustain operations. A business's ability to generate consistent and growing revenue directly impacts its profitability, retained earnings, and cash flow. High revenue levels typically correlate with increased profitability as long as the business can manage its costs effectively. Additionally, growing revenue is often critical in attracting investment, as investors usually seek businesses with robust, sustainable income streams.

Revenue is also closely connected to other financial metrics, such as net and retained earnings. A significant increase in revenue can lead to higher net income, which, after accounting for expenses and taxes, boosts retained earnings, the profits the company chooses to reinvest into the business.

The effect of revenue on finances extends beyond profitability. Revenue influences a company’s financial strategies, including pricing decisions, product development, market expansion, and capital investment. Companies with strong revenue growth are often better positioned to take on new ventures, secure loans, and attract strategic partnerships that support their long-term objectives.

The Relationship Between Revenue and Retained Earnings: Understanding the Financial Impact

The connection between revenue and retained earnings is fundamental to understanding a company’s financial performance and ability to reinvest profits for growth. As previously discussed, retained earnings represent the accumulated net income a company has kept in the business rather than distributed to shareholders as dividends. Revenue, the income generated from core business activities, plays a pivotal role in determining the level of net income, which ultimately influences the retained earnings balance.

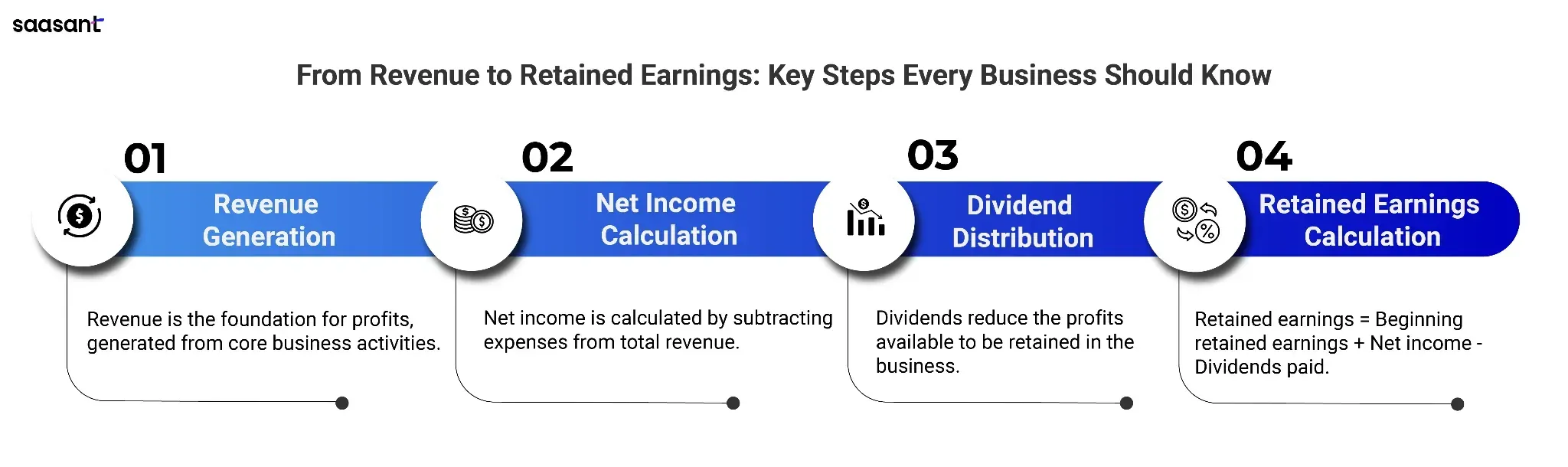

Step-by-Step Explanation: How Revenue Contributes to the Calculation of Retained Earnings?

The relationship between revenue and retained earnings can be broken down into a few straightforward steps:

Revenue Generation: The first step is revenue generation through the company’s primary business operations, such as sales of products or services. This revenue is recorded on the income statement and is the foundation for calculating the company’s net income.

Net Income Calculation: Once revenue is earned, expenses such as costs of goods sold (COGS), operating expenses, interest, and taxes are deducted. The result is net income, representing the company’s profit for the period. Net income is a critical component in determining retained earnings, as the portion of revenue remains after all costs are subtracted.

Dividend Distribution: If the company distributes dividends to shareholders, these payments reduce the amount of profit available to be retained. The remaining balance is retained earnings.

Retained Earnings Formula: The final step involves the calculation of retained earnings using the following formula:

Retained Earnings = Beginning Retained Earnings + Net Income - Dividends Paid

Thus, the net income derived from revenue is the key driver in increasing retained earnings, as it determines how much profit will be maintained in the business.

The Impact of Revenue on Net Income and How That Translates to Retained Earnings

A business's revenue directly impacts net income and, therefore, retained earnings. Higher revenue increases net income, assuming that expenses remain constant. When net income rises, retained earnings also grow, providing the company more capital to reinvest in its operations, pay down debt, or fund expansion efforts.

For example, if a company experiences an increase in sales revenue, the result is typically a higher net income (assuming costs are managed). This higher net income increases retained earnings, reinforcing the company’s ability to reinvest in growth initiatives. Conversely, net income may decrease if revenue declines, resulting in lower retained earnings unless the company adjusts its expenses or dividend payouts.

Effects of Increasing vs. Decreasing Revenue on the Balance Sheet

The effects of increasing or decreasing revenue on a company’s financial health are significant, especially when it comes to retained earnings:

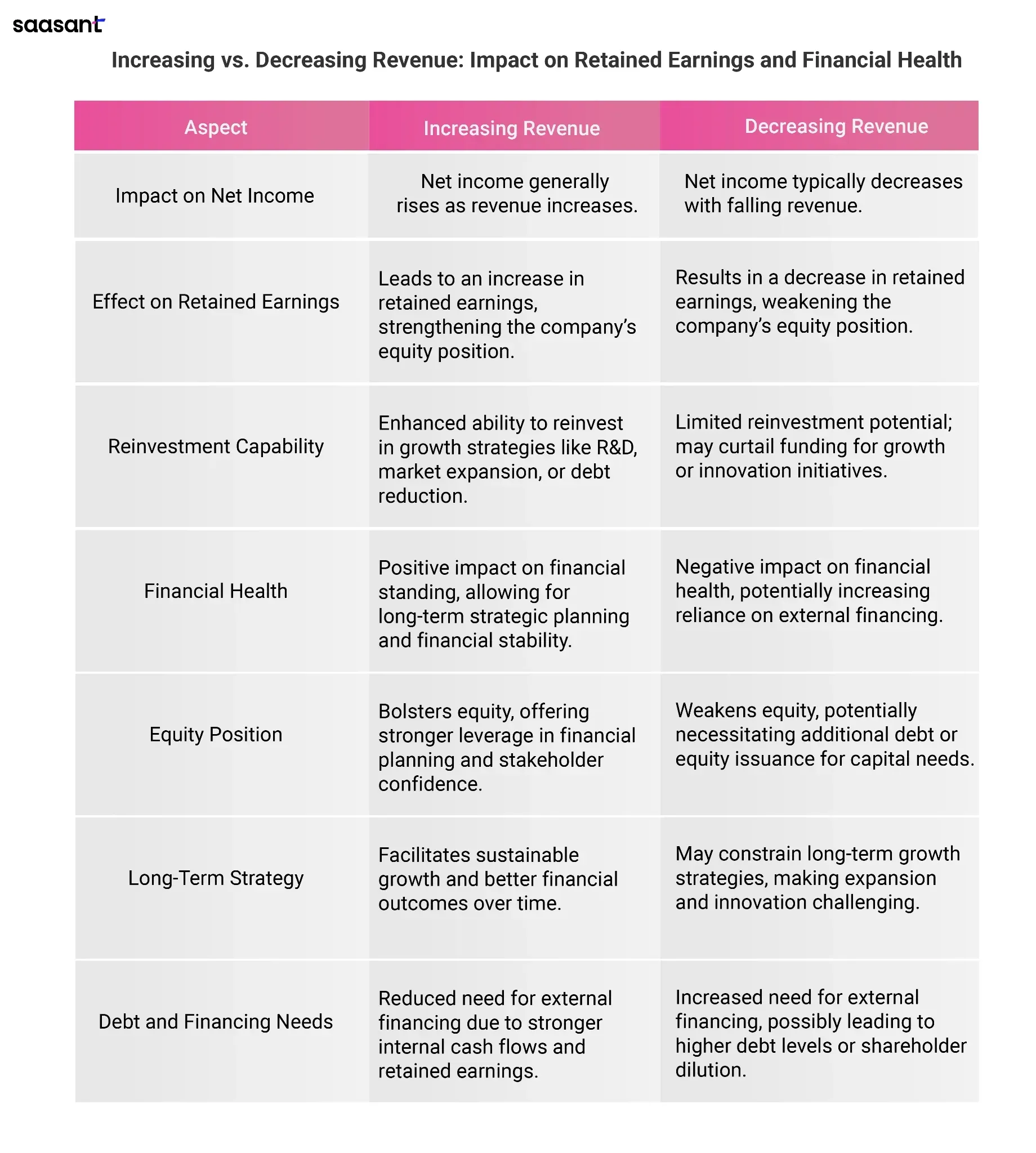

Increasing Revenue: An increase in revenue is generally positive for a company’s financial outlook. As revenue rises, net income typically follows, and when net income grows, retained earnings increase as well. This positive trend bolsters the company’s equity position, improving its financial standing and ability to reinvest. A steady increase in revenue, combined with effective cost management, can lead to exponential growth in retained earnings over time, enhancing the company’s capacity to fund long-term strategies such as research and development, market expansion, or debt reduction.

Decreasing Revenue: On the other hand, a decline in revenue can negatively impact retained earnings. If revenue falls, it can lead to reduced net income, which in turn reduces the amount of retained earnings. This can affect a company’s ability to reinvest profits and may limit opportunities for expansion or innovation. Decreased retained earnings can also lead to a higher reliance on external financing, which could increase debt levels or dilute shareholder equity by issuing new shares.

The Role of Dividends in Retained Earnings: Impact on Financial Growth and Stability

Dividends are critical to understanding how retained earnings evolve. Retained earnings represent the net income not distributed to shareholders but reinvested in the business. While revenue and net income are essential for growing retained earnings, paying dividends can significantly influence this balance. Understanding the interaction between dividends and retained earnings is crucial for business owners and investors who aim to gauge a company's financial health and growth potential.

How Dividend Distribution Influences Retained Earnings Despite Revenue?

The distribution of dividends directly affects the retained earnings balance, even though the company's revenue and net income may rise. While high revenue typically leads to increased net income, part of that income may be paid out to shareholders as dividends. When dividends are paid, they reduce the net income that would otherwise be retained within the business, lowering the retained earnings balance.

Even if a company is generating substantial revenue and has a solid net income, the decision to distribute dividends will decrease the profit the company keeps. This reduction in retained earnings could impact the company’s ability to reinvest in future growth initiatives, such as research and development, debt reduction, or expansion.

Explanation of the Formula for Retained Earnings with and without Dividends

Retained earnings calculation incorporates net income, influenced by revenue, and subtracts shareholder dividends. The basic formula for retained earnings can be expressed as:

Retained Earnings = Beginning Retained Earnings + Net Income - Dividends Paid

Here’s how the formula works in both scenarios:

With Dividends: If a company declares and pays dividends, these payments are subtracted from the net income to determine the retained earnings. This is the most common approach for companies that wish to distribute part of their profits to shareholders.

Example: If a company has $500,000 in net income, beginning retained earnings of $1,000,000, and pays out $200,000 in dividends, the retained earnings for the period will be:

$1,000,000 + $500,000 - $200,000 = $1,300,000 in retained earnings.

Without Dividends: If the company chooses not to pay dividends or retain all its profits, the retained earnings will grow by the total amount of net income. This approach helps in reinvesting profits for business growth.

Example: If the same company decides not to pay dividends, the retained earnings will be:

$1,000,000 + $500,000 = $1,500,000 in retained earnings.

Impact of Dividends on Retained Earnings

The decision to pay dividends or retain profits within the company is strategic and can profoundly impact the company’s financial position. Here's how dividends affect retained earnings:

Positive Impact on Shareholder Value: By distributing dividends, companies provide direct value to shareholders, making them more attractive to investors who seek regular income. However, while this improves shareholder satisfaction, it reduces the cash retained in the company, which could otherwise be reinvested.

Reduction in Retained Earnings: Dividend payouts decrease the net income retained within the business. This can affect a company’s ability to fund future growth without external financing, such as taking on debt or issuing more shares. If a company consistently pays high dividends, its retained earnings may stagnate or decline over time, potentially impacting its long-term expansion plans.

Balancing Growth and Shareholder Returns: Companies often face a balancing act when deciding the appropriate level of dividend payouts. While distributing dividends may appeal to investors looking for returns, retaining a portion of profits is equally crucial for sustaining business growth and maintaining financial flexibility.

While revenue and net income are crucial for increasing retained earnings, paying dividends directly reduces the company's profit. The retained earnings formula reflects this interaction, with dividends subtracted from net income to calculate the final retained earnings balance. The decision to pay dividends versus retaining profits is a critical financial decision that impacts a company’s ability to reinvest in future growth and achieve long-term success.

How Revenue Affects Retained Earnings? A Real-World Example

Understanding the relationship between revenue and retained earnings is essential for evaluating a company's financial health and long-term viability. In this case study, we will explore a simplified example to demonstrate how changes in revenue can directly impact retained earnings. This example uses real-world data to illustrate the dynamics at play and helps business owners, investors, and financial professionals understand the implications of revenue fluctuations on retained earnings.

Real-World Example: Company XYZ

Company XYZ is a hypothetical company that manufactures and sells consumer electronics. We will examine two scenarios: one in which revenue increases and another in which it decreases. Through this case study, we will observe how these changes in revenue affect the company's retained earnings over one fiscal year.

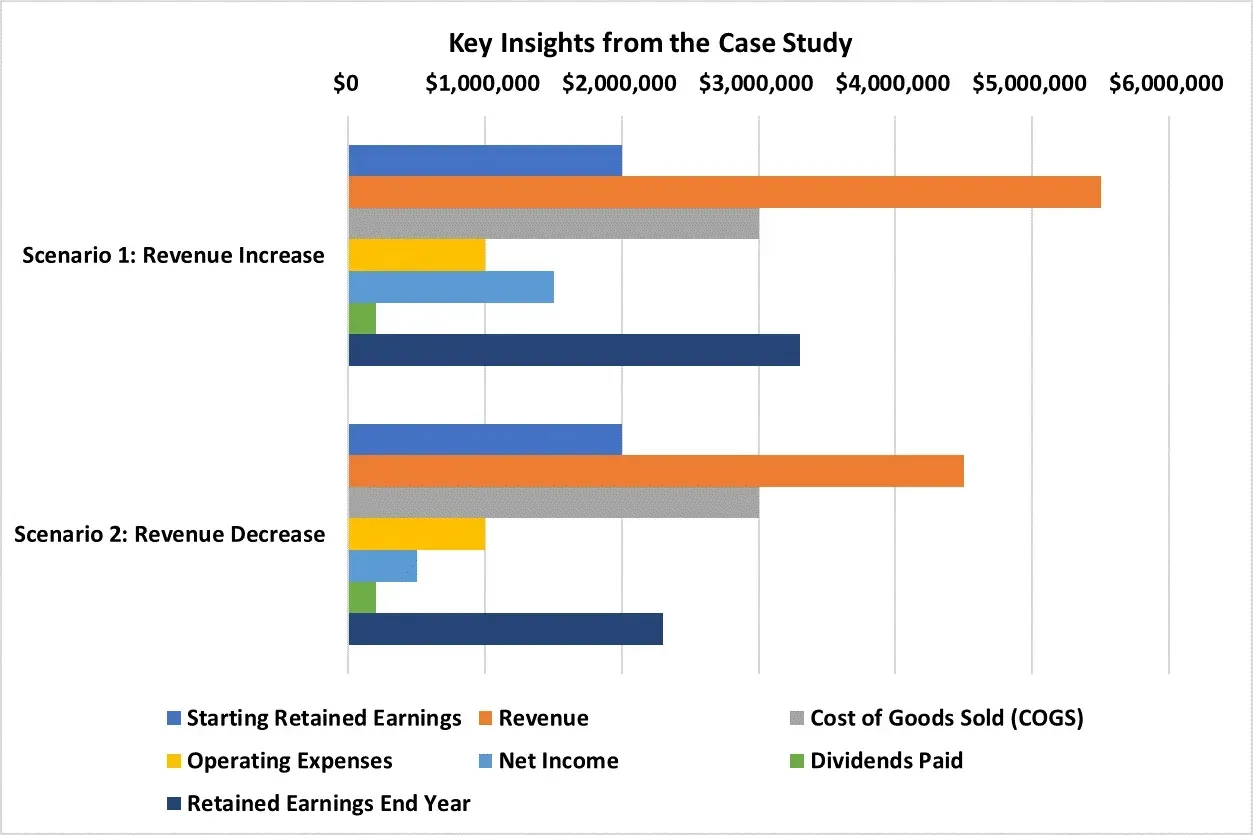

Initial Assumptions

Starting Retained Earnings: $2,000,000

Revenue for Year 1: $5,000,000

Cost of Goods Sold (COGS): $3,000,000

Operating Expenses: $1,000,000

Net Income: Revenue – COGS – Operating Expenses = $5,000,000 – $3,000,000 – $1,000,000 = $1,000,000

Dividends Paid: $200,000

Scenario 1: Revenue Increase

In the first scenario, assume that Company XYZ experiences a 10% increase in revenue due to a surge in demand for its new product line. The company’s latest revenue for Year 2 becomes $5,500,000.

Adjusting the Financials for Year 2:

Revenue for Year 2: $5,500,000

COGS and Operating Expenses remain constant at $3,000,000 and $1,000,000, respectively.

Net Income for Year 2: $5,500,000 – $3,000,000 – $1,000,000 = $1,500,000

Dividends Paid: The company continues to pay $200,000 in dividends.

Calculation of Retained Earnings for Year 2:

Using the formula for retained earnings:

Retained Earnings (Year 2) = Beginning Retained Earnings + Net Income – Dividends Paid

Retained Earnings (Year 2) = $2,000,000 + $1,500,000 – $200,000 = $3,300,000

Impact on Retained Earnings:

In this scenario, the 10% revenue increase results in a net income increase of $500,000. After accounting for the dividends, retained earnings rise from $2,000,000 to $3,300,000, a significant boost to the company’s ability to reinvest in future growth or pay down debt.

Scenario 2: Revenue Decrease

In the second scenario, Company XYZ faces a market downturn, resulting in a 10% decrease in revenue for Year 2. The company’s new revenue for the year is now $4,500,000.

Adjusting the Financials for Year 2:

Revenue for Year 2: $4,500,000

COGS and Operating Expenses remain unchanged.

Net Income for Year 2: $4,500,000 – $3,000,000 – $1,000,000 = $500,000

Dividends Paid: The company still distributes $200,000 in dividends.

Calculation of Retained Earnings for Year 2:

Using the same retained earnings formula:

Retained Earnings (Year 2) = Beginning Retained Earnings + Net Income – Dividends Paid

Retained Earnings (Year 2) = $2,000,000 + $500,000 – $200,000 = $2,300,000

Impact on Retained Earnings:

In this scenario, the decrease in revenue leads to a decline in net income of $500,000, and after paying dividends, retained earnings rise from $2,000,000 to only $2,300,000. This slower growth in retained earnings limits the company’s ability to reinvest and may impact its ability to take on new projects or pursue aggressive expansion strategies.

Key Insights from the Case Study

This case study demonstrates the direct link between revenue and retained earnings:

Increasing Revenue: A rise in revenue directly boosts net income, increasing retained earnings and allowing the company to reinvest more into its operations and future growth. In the case of Company XYZ, the 10% revenue increase resulted in a $1,300,000 growth in retained earnings.

Decreasing Revenue: Conversely, a drop in revenue negatively impacts net income, which leads to a more minor increase in retained earnings. Company XYZ's 10% revenue decrease resulted in a $700,000 lower increase in retained earnings compared to the previous scenario.

Dividends and Retained Earnings: Despite the changes in revenue, dividends continue to reduce the amount of profit retained within the company. This example highlights the delicate balance businesses must maintain between rewarding shareholders through dividends and retaining enough profits for reinvestment.

By showing the financial impact of both increasing and decreasing revenue, we better understand how changes in business performance can either enhance or limit the company’s ability to reinvest and grow. Companies that experience strong revenue growth can accumulate more retained earnings, providing them with the capital needed to fund future projects and ensure long-term success. However, when revenue decreases, the opposite effect occurs, emphasizing the importance of sustaining strong sales and managing expenses effectively.

Why Understanding the Effect of Revenue on Retained Earnings Matters?

Understanding how revenue impacts retained earnings is essential for anyone involved in a business's financial management or analysis. Retained earnings play a crucial role in shaping the company’s financial health and growth potential. They serve as a key indicator of how effectively a company reinvests its profits into the business, and understanding this relationship can provide valuable insights for investors, financial analysts, and business owners alike.

Importance for Investors, Financial Analysts, and Business Owners to Track Retained Earnings

Understanding retained earnings is vital for investors and financial analysts because it helps assess a company's long-term financial stability and growth potential. Here’s why it matters:

Indicator of Financial Health: Retained earnings represent the cumulative profits a company has kept for reinvestment instead of paying out as dividends. A growing retained earnings balance generally indicates that a company generates healthy profits and effectively manages its finances. This can be a positive signal to investors, showing that the company has the capital to fund future growth, repay debt, or weather economic downturns.

Evaluating Profitability: For business owners, tracking retained earnings helps assess the company’s overall profitability over time. A steady increase in retained earnings indicates that the company is consistently profitable and efficiently managing its revenue and expenses. Conversely, stagnation or decreased retained earnings may signal potential issues, such as declining revenue, high operating costs, or unsustainable dividend payouts.

Strategic Decision-Making: Retained earnings provide insights into how much capital is available for reinvestment. Understanding how their revenue impacts retained earnings is essential for business owners because it directly influences their ability to make strategic decisions. A higher retained earnings balance can provide the flexibility to reinvest in expansion, product development, and innovation, which can fuel further growth.

How Understanding Retained Earnings Helps in Assessing Business Growth, Profitability, and Reinvestment Opportunities?

Tracking retained earnings and understanding revenue's role provides crucial insights into a company’s financial trajectory and long-term success. Here's how it helps:

Assessing Business Growth: Retained earnings reflect a company’s growth ability without relying solely on external financing. By understanding the effect of revenue on retained earnings, stakeholders can gauge how well a company is using its profits to fund growth initiatives. For instance, a business that consistently maintains a significant portion of its profits is likely positioning itself for growth through reinvestment in capital projects, research and development, or market expansion.

Profitability Analysis: Retained earnings are a direct result of net income, which, in turn, is heavily influenced by a company’s revenue. Analyzing changes in retained earnings over time provides a clear picture of profitability trends. Revenue increases typically lead to a boost in net income, which, if not used for dividends, results in higher retained earnings. This is particularly important for investors and analysts who evaluate a company’s financial health and compare profitability across industry peers.

Reinvestment Opportunities: A company’s ability to reinvest in itself, whether through capital expenditures, acquisitions, or other growth initiatives, is often determined by the level of retained earnings. For business owners, understanding how revenue translates to retained earnings allows them to assess how much capital they have available for reinvestment. A higher retained earnings balance means the company has more resources to reinvest into its operations, expanding its capacity to innovate, improve efficiencies, or scale operations. This reinvestment is essential for sustaining long-term business growth.

Funding for Future Projects: Companies with strong retained earnings are often better positioned to fund future projects without depending on external financing sources, such as loans or stock issuance. By understanding how increasing revenue results in higher retained earnings, companies can strategize on allocating these funds to high-return projects that will drive business success. This self-funding mechanism gives companies more control over their financial decisions and future growth.

Tracking retained earnings offers valuable insights into a company’s profitability, growth potential, and ability to reinvest in future opportunities. For investors, it acts as a gauge for long-term financial health and the company’s ability to weather economic fluctuations. For financial analysts, it provides a lens through which to assess a company’s ability to generate sustainable returns. Finally, understanding the relationship between revenue and retained earnings enables more intelligent decision-making regarding capital allocation, reinvestment strategies, and growth plans for business owners.

Key Factors That Can Influence Retained Earnings Beyond Revenue

Retained earnings, a crucial financial metric for businesses, represent the portion of a company’s net income that is not distributed as dividends but reinvested in the company or kept as a reserve for future use. While revenue is significant in determining retained earnings, other factors can significantly influence this amount.

Taxes and Their Impact on Retained Earnings

The company's tax obligation is one of the most significant factors affecting retained earnings. Taxes directly reduce a business's available profits. Corporate income tax rates vary across jurisdictions, and businesses must factor this into their earnings calculations. Only the remaining amount can be added to retained earnings when taxes are deducted from net income.

For instance, a company with substantial taxable income will considerably reduce retained earnings due to tax payments. As a result, businesses must incorporate tax planning into their strategy to maximize retained earnings and ensure optimal tax efficiency.

Note: Effective tax management is crucial for boosting retained earnings, as high tax burdens can severely limit the funds available for reinvestment. |

Operating Expenses and Their Role in Reducing Retained Earnings

Operating expenses, including costs related to day-to-day business activities (such as salaries, rent, utilities, and materials), can significantly impact retained earnings. These expenses are subtracted from a company’s gross profit, thus reducing the net income.

An increase in operating expenses, whether due to inflation, higher wages, or unexpected operational costs, can lower profitability and, consequently, retained earnings. For example, if a company invests heavily in research and development (R&D) or scales up operations, these operational expenses can erode earnings, reducing the amount that can be retained.

Key Takeaway: Businesses must carefully monitor and control operating expenses to preserve their retained earnings, balancing growth and operational costs. |

Dividends and Their Direct Impact on Retained Earnings

Although not an operational factor, dividend payments are one of the most direct actions influencing retained earnings. When a company distributes profits to shareholders, those funds are deducted from retained earnings. The more substantial the dividend payout, the lower the amount that remains within the business.

A decision to pay higher dividends often reflects confidence in the company’s financial health but can also reduce the funds available for reinvestment. Companies must balance shareholders' needs with the long-term sustainability of retained earnings.

Note: Strategic decisions on dividend payouts are essential for ensuring a healthy retained earnings balance that supports future growth. |

Non-Recurring Events and Their Effects on Retained Earnings

Non-recurring events, such as one-time gains or losses from the sale of assets, litigation settlements, or extraordinary expenses (e.g., restructuring costs), can significantly, albeit temporarily, impact retained earnings. These events may cause a surge in earnings or a sudden reduction, but they do not reflect ongoing operational performance.

For example, a company selling off a piece of property might experience a one-time gain, temporarily increasing its retained earnings. Conversely, an unexpected legal settlement could lead to a significant decrease in retained earnings. Though these events are not regular, their financial effects should still be considered when assessing a company’s overall economic health.

Key Takeaway: While non-recurring events can distort retained earnings figures, they must be considered to understand a company’s true financial position. |

Depreciation and Amortization: Long-Term Effects on Retained Earnings

Depreciation and amortization, while non-cash expenses, reduce a company's taxable income, which can indirectly influence retained earnings. These expenses represent the allocation of the cost of assets over time and must be deducted from the gross profit. Though they don’t involve actual cash outflows, their impact on net income can significantly lower the amount added to retained earnings.

For businesses with substantial fixed assets, depreciation expenses can accumulate over the years, reducing retained earnings. However, the tax benefits that result from depreciation can offset this reduction, allowing businesses to maintain or even increase retained earnings over time.

Note: While depreciation and amortization reduce retained earnings in the short term, they can help businesses by offering tax advantages, ultimately influencing long-term financial strategy. |

Interest Expenses: The Cost of Borrowed Funds

Companies that finance their operations through debt may face interest expenses, which reduce net income and, consequently, retained earnings. The higher the debt level, the greater the interest expense, which can significantly affect profitability.

Interest expenses are particularly relevant for businesses with high leverage levels, representing a recurring financial obligation. Managing interest payments effectively while balancing the use of debt for growth is crucial for maintaining strong retained earnings over time.

Key Takeaway: Managing debt and interest costs is critical for protecting retained earnings and ensuring financial sustainability. |

Understanding the various factors influencing retained earnings beyond revenue is essential for effective financial management. Taxes, operating expenses, dividends, non-recurring events, depreciation, amortization, and interest expenses all play significant roles in determining the final amount of retained earnings a company can accumulate. By strategically managing these factors, businesses can enhance their financial flexibility and create a robust foundation for long-term growth.

Common Mistakes to Avoid When Calculating Retained Earnings

Retained earnings are a crucial financial metric that reflects a company’s accumulated profits minus any dividends distributed to shareholders. Accurately calculating retained earnings is essential for businesses to track their financial health and make informed decisions. However, several common mistakes can arise during this process, potentially leading to incorrect financial reporting and poor decision-making.

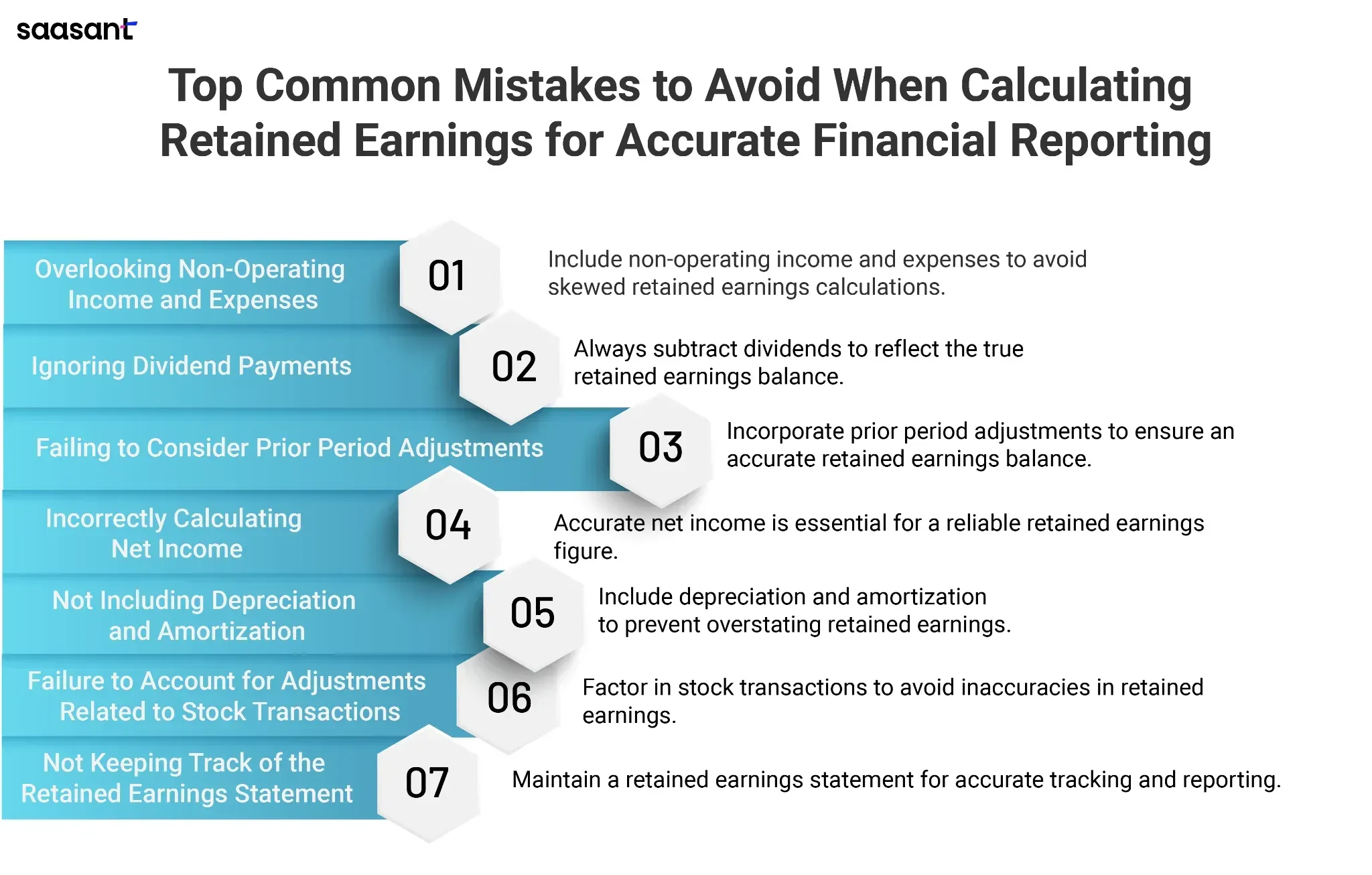

Overlooking Non-Operating Income and Expenses

One of the most common mistakes when calculating retained earnings is failing to account for non-operating income or expenses. These are revenues or costs that are not directly related to the company’s core business operations, such as income from investments, asset sales, or extraordinary gains or losses.

If non-operating income or expenses are excluded, it can lead to an inaccurate representation of the company’s actual financial performance, as they affect the net income. For instance, if a company sells an asset and generates a profit, this should be included in the retained earnings calculation. Neglecting this can overstate or understate the amount of earnings retained.

How to Avoid This Mistake: Ensure that all forms of income, including non-operating items, are considered when calculating retained earnings. Regularly review the income statement for extraordinary or non-recurring transactions and include them in your final calculations.

Key Takeaway: Always include non-operating income and expenses to ensure a comprehensive retained earnings calculation.

Ignoring Dividend Payments

Another significant error is overlooking dividend payments. Dividends are paid from the company’s earnings, and any dividends distributed directly reduce the retained earnings balance. Failing to subtract the dividend payments from net income will result in overestimating retained earnings.

Whether paid in cash or stock, dividends must be deducted from the net income to determine the actual retained earnings. Many companies, particularly those that distribute regular dividends, can experience substantial changes in their retained earnings balance due to these payouts.

How to Avoid This Mistake: Always ensure that the dividends, whether paid or declared, are subtracted from net income during the retained earnings calculation process. Double-check the dividend records in the company’s financial statements for accuracy.

Key Takeaway: Subtract all dividend payments from net income to avoid overstating retained earnings.

Failing to Consider Prior Period Adjustments

Retained earnings are carried over from one period to the next, and any adjustments or corrections to prior periods’ financials must be reflected in the current retained earnings calculation. Prior period adjustments could arise from accounting errors, changes in accounting policies, or reclassification of transactions.

Neglecting to incorporate prior-period adjustments could lead to inaccurate retained earnings balances and affect the company's overall financial health. For example, if an error in revenue recognition from the previous period is corrected, the adjustment must be accounted for in the retained earnings calculation.

How to Avoid This Mistake: Regularly review prior period adjustments and ensure they are properly reflected in the current period's retained earnings. Work closely with your accounting team to identify and address any discrepancies from previous financial periods.

Key Takeaway: Always account for prior period adjustments to maintain an accurate retained earnings balance.

Incorrectly Calculating Net Income

Since retained earnings are derived from net income, any errors in the net income calculation will inevitably lead to incorrect retained earnings figures. Mistakes such as miscalculating revenue, expenses, or taxes can distort the net income figure and, in turn, mislead the calculation of retained earnings.

For example, failing to account for tax liabilities or including unrecorded expenses can result in an inflated net income, which will carry over to an inflated retained earnings figure.

How to Avoid This Mistake: Ensure that net income is accurately calculated by properly accounting for all revenue streams, expenses, taxes, and non-recurring events. Use a well-defined process for reviewing financial statements and reconciling accounts to ensure all figures are correct.

Key Takeaway: Double-check net income calculations to ensure your retained earnings figure is based on accurate financial data.

Not Including Depreciation and Amortization

Depreciation and amortization are accounting processes that allocate the cost of tangible and intangible assets over time. These non-cash expenses reduce the net income and, consequently, the retained earnings.

Omitting depreciation and amortization expenses can lead to overestimating net income and overstating retained earnings. This is especially critical for businesses with significant investments in long-term assets, as depreciation and amortization can substantially impact retained earnings over time.

How to Avoid This Mistake: Ensure depreciation and amortization are appropriately calculated and deducted from net income. These figures should be clearly stated in the company’s financial statements and reflected in the retained earnings calculation.

Key Takeaway: Always include depreciation and amortization when calculating retained earnings to avoid inaccuracies in your financial reporting.

Failure to Account for Adjustments Related to Stock Transactions

Stock buybacks, stock splits, and other equity-related transactions can influence the retained earnings balance. For instance, if a company repurchases its shares, the expenditure reduces cash. Still, it doesn’t directly affect the retained earnings unless the transaction changes the Equity section.

A common mistake is neglecting to consider these stock transactions, which can distort the company’s financial standing.

How to Avoid This Mistake: Ensure that any stock changes, whether buybacks, splits, or dividends in stock form, are appropriately reflected in the retained earnings calculation. Review the company’s shareholder equity section to account for these adjustments.

Key Takeaway: Always incorporate stock-related adjustments in your retained earnings calculation to maintain accurate financial reporting.

Not Keeping Track of the Retained Earnings Statement

Some businesses need to pay more attention to the importance of maintaining a separate retained earnings statement. This document outlines changes to the retained earnings account throughout the accounting period and helps track adjustments, dividend payouts, and earnings accumulation.

Without a proper statement, reconciling retained earnings with net income can become challenging, especially during periods of significant financial change.

How to Avoid This Mistake: Create and maintain a detailed retained earnings statement that tracks the changes in retained earnings from one period to the next. This will ensure transparency and accuracy in the financial reporting process.

Key Takeaway: Regularly update and maintain a retained earnings statement to ensure all adjustments are accounted for and reported correctly.

Companies can ensure that their financial reports reflect their actual standing by avoiding common mistakes such as overlooking non-operating income, failing to account for dividends, and miscalculating net income. Attention to detail and thorough checks at each step of the calculation process will help companies avoid inaccuracies and support sound financial planning.

Wrap Up

In conclusion, understanding the relationship between revenue and retained earnings is vital for assessing a company’s financial health and making informed decisions. Revenue is the cornerstone of retained earnings, as it directly influences net income, which forms the basis for calculating retained earnings. However, it’s essential to recognize that other elements, such as operating expenses, taxes, dividends, and non-operating income, also significantly shape the retained earnings balance.

Revenue’s Direct Influence: Revenue plays a crucial role in boosting retained earnings. The higher your revenue, the greater the potential for retaining earnings, assuming expenses and taxes are effectively controlled.

Comprehensive Financial Tracking: While revenue is central to calculating retained earnings, tracking all factors influencing net income, including non-operating income and expenses, is essential. Regularly reviewing financial statements ensures that adjustments, including dividend payouts and tax obligations, are accurately reflected.

Ongoing Financial Accuracy: Accurate management of retained earnings requires ongoing tracking and adjustments to ensure figures remain precise. This is where integrated financial tools can be invaluable.

For businesses looking to streamline their accounting and ensure that every financial aspect is captured correctly, applications like SaasAnt Transactions can help simplify importing, categorizing, and exporting financial data. This enhances accuracy and allows businesses to maintain real-time visibility into their financial status, ensuring that retained earnings are calculated correctly.

Additionally, for companies dealing with cross-border transactions and managing multi-currency accounts, solutions like PayTraQer allow seamless importation of payments and transaction data, making tracking how international revenue impacts retained earnings easier.

By leveraging such applications, businesses can significantly reduce the complexities of managing retained earnings and financial reports, ensuring that your figures are as accurate and up-to-date as possible.

Take control of your business’s future by tracking your financial performance more efficiently. Start by ensuring your retained earnings are accurately calculated, considering all factors influencing net income. Applications like SaasAnt Transactions and PayTraQer can help simplify these processes, ensuring that your financial statements are always in order and that your retained earnings reflect the true financial health of your business.

Maintaining accurate financial records and reviewing your financial performance can provide valuable insights into your business's health. By integrating the right financial tools, you can make more informed decisions, optimize profitability, and foster long-term growth.

FAQs

How Does Revenue Affect Retained Earnings?

Revenue affects retained earnings by contributing to net income. A company's revenue covers operating expenses, taxes, and other costs. The leftover amount is net income, which is then added to retained earnings. Higher revenue generally means higher net income, thus increasing retained earnings if expenses and other deductions are well managed.

Why Is Revenue Important for Retained Earnings Growth?

Revenue is essential for retained earnings growth because it is a business's primary source of income. After deducting expenses, any remaining profit (net income) can be retained. Consistent revenue growth allows businesses to increase their retained earnings, which can be reinvested in the company for expansion or innovation.

What Happens to Retained Earnings If Revenue Decreases?

If revenue decreases, the company’s net income will likely decrease, provided expenses remain the same. Lower net income means less profit to retain, resulting in lower retained earnings. A sustained drop in revenue may even cause retained earnings to decline over time, impacting the company’s ability to invest or grow.

Can a Company Have High Revenue but Low Retained Earnings?

Yes, high revenue only sometimes leads to high retained earnings. If a company incurs high operating expenses, taxes, and significant dividend payouts, these deductions will reduce net income, leaving less to retain. For example, a company with $1 million in revenue but $950,000 in expenses and dividends will have only $50,000 for retained earnings.

How Are Net Income and Retained Earnings Related to Revenue?

Net income and retained earnings are both directly tied to revenue. Revenue is the starting figure from which a company deducts expenses, taxes, and dividends. The resulting amount is net income, which either increases retained earnings (if retained) or decreases (if paid out as dividends). Therefore, net income results from revenue after all costs, directly impacting the retained earnings balance.

Does an Increase in Revenue Automatically Result in Higher Retained Earnings?

An increase in revenue can lead to higher retained earnings, but only if other costs like operating expenses and dividends do not increase proportionally. For instance, if revenue rises by 20%, but operating costs and taxes increase by 25%, net income may not grow, resulting in no additional retained earnings. Only effective cost management alongside revenue growth will lead to higher retained earnings.

How Do Dividends Impact Retained Earnings Even If Revenue Is High?

Dividends reduce retained earnings because they are paid out from net income. Even if a company has high revenue, the amount added to retained earnings will be reduced if it issues large dividends. For example, if a company has $200,000 in net income but pays $150,000 in dividends, only $50,000 will be added to retained earnings, regardless of its revenue.

Is Revenue the Only Factor That Affects Retained Earnings?

No, while revenue is a significant factor, retained earnings are also affected by other elements such as operating expenses, taxes, non-operating income, and dividend payments. These components impact net income, determining the amount added to retained earnings.

Why Should Businesses Track Revenue’s Impact on Retained Earnings?

Tracking how revenue affects retained earnings provides insight into a company’s profitability. By understanding how much profit is retained versus paid out in expenses or dividends, businesses can make strategic decisions to optimize reinvestment, reduce unnecessary costs, and achieve financial growth.

What Steps Can Companies Take to Increase Retained Earnings Through Revenue Growth?

To increase retained earnings, companies can focus on strategies like boosting sales, reducing operating expenses, and managing dividends. For example, a company could expand its market presence to increase revenue, cut unnecessary operational costs, or retain a more significant portion of net income by limiting dividend payouts.

Does Revenue from Non-operating Activities Affect Retained Earnings?

Yes, revenue from non-operating activities, such as investment income or asset sales, does affect retained earnings by increasing net income. For instance, selling a company asset at a profit adds to net income, which boosts retained earnings. However, non-operating revenue is often irregular and less sustainable than core operations revenue.

How Can SaasAnt Transactions and PayTraQer Help Track Revenue’s Impact on Retained Earnings?

SaasAnt Transactions and PayTraQer facilitate accurate financial tracking by seamlessly importing, categorizing, and consolidating revenue data into accounting systems like QuickBooks. By integrating revenue and transaction data from various sources, these tools provide businesses with a clear, up-to-date picture of their net income and retained earnings. This helps manage financial data efficiently, reduce errors, and ensure accurate calculations for retained earnings.