What is a Journal Entry in QuickBooks?

A journal entry in QuickBooks is a powerful tool for recording financial transactions that don’t fit into other forms, like invoices or checks. These entries allow you to move money between accounts, ensuring your books are balanced and accurate.

What is Considered a Journal Entry?

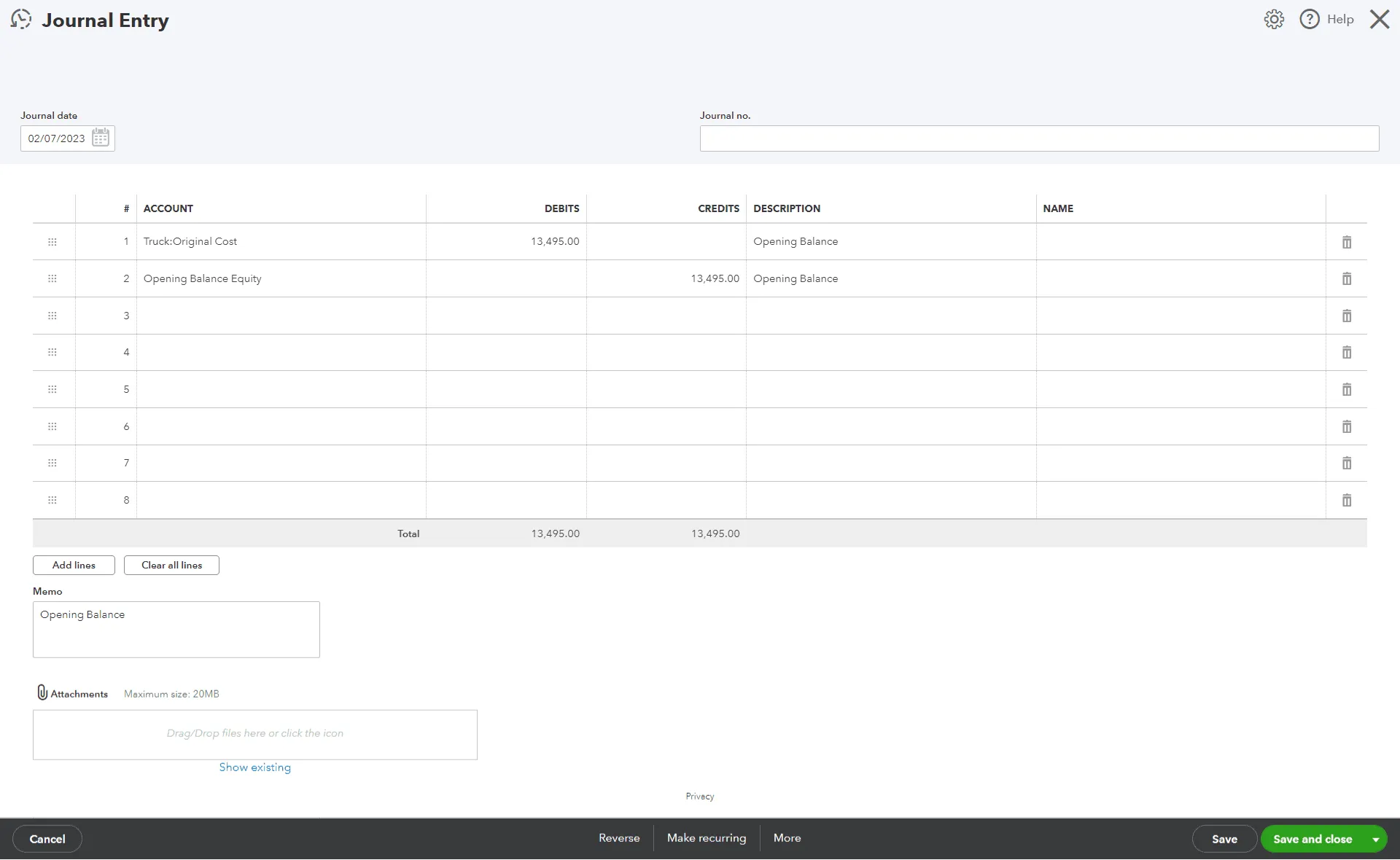

A journal entry typically includes:

Date: The transaction date.

Entry Number: A unique identifier for tracking.

Accounts: The accounts that will be debited and credited.

Amounts: The monetary values for each account.

Memo: A description of the transaction.

Example of a Journal Entry in Accounting

Imagine you mistakenly recorded a $100 payment to your insurance company under utilities. To correct this, you would create a journal entry to debit the utilities account by $100 and credit the insurance account by the same amount. This ensures your financial records accurately reflect your expenses.

The Main Purpose of a Journal Entry

A journal entry's primary purpose is to record every business transaction accurately in your general ledger. This is crucial for maintaining the integrity of your financial statements, affecting your business’s financial health and compliance with accounting standards.

When Should You Do a Journal Entry?

Journal entries are necessary in several situations:

Adjusting Entries: To update account balances before preparing financial statements.

Depreciation Entries: To allocate the cost of an asset over its useful life.

Accrual Entries: To record revenues and expenses incurred but still need to be recorded.

Tax Adjustments: To record tax liabilities or credits.

Error Corrections: To fix mistakes in previous entries.

What Requires a Journal Entry?

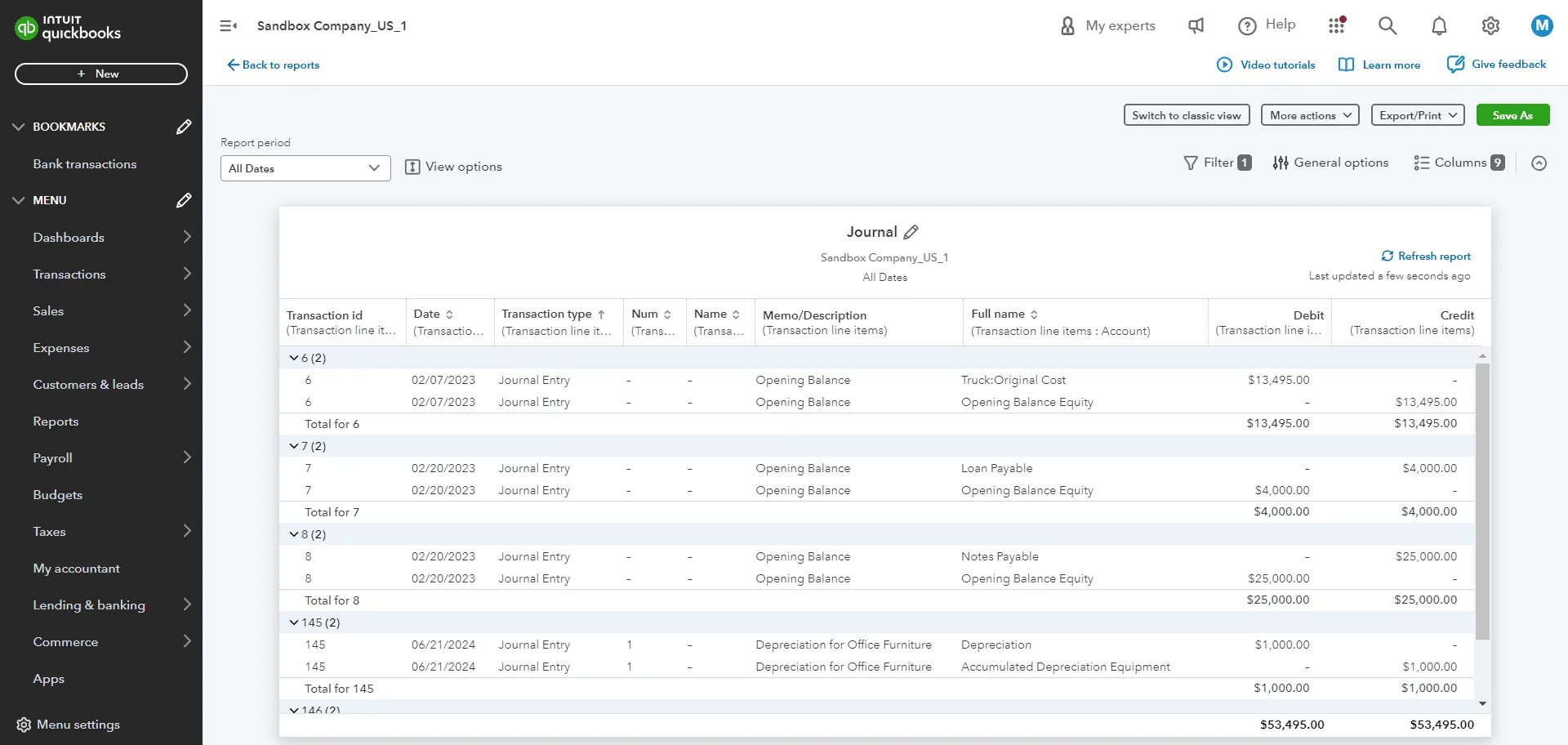

Journal entries are needed for transactions that affect multiple accounts or cannot be recorded through standard forms. Examples include:

Income and Expense Allocation: Distributing costs and revenues across different departments or projects.

Owner’s Draws: Recording funds withdrawn by the business owner.

Stock Adjustments: Updating inventory levels and values.

Capital Contributions: Recording investments made into the business.

During tax season, the volume of necessary journal entries can be overwhelming. Many small business owners are buried under these entries, struggling to meet the demand. This is where tools like SaasAnt Transactions can be invaluable. SaasAnt automates importing bulk journal entries into QuickBooks, saving time and reducing errors. This tool is handy for recurring entries, such as monthly depreciation or loan interest adjustments, which can be set up to recur automatically.

Related articles:

How to Find Journal Entries in QuickBooks

Streamline Your Accounting with SaasAnt Transactions

SaasAnt Transactions can significantly ease the burden of managing journal entries. It allows you to upload large volumes of transactions in one go, eliminating the need to enter each one manually. This speeds up the process and reduces the risk of errors, ensuring your financial records are accurate and up-to-date. Whether you’re preparing for tax season or managing daily accounting tasks, SaasAnt can help streamline your workflow.

By mastering using journal entries in QuickBooks and leveraging automation tools like SaasAnt, you can ensure your business’s financial health is accurately reported and managed. This will save you time and give you the peace of mind that your financial records are precise and reliable.