Which is Not a Temporary Account in Accounting?

In accounting, understanding the roles of temporary and permanent accounts is essential for managing a company's financial transactions and preparing comprehensive financial statements. Temporary accounts, also termed nominal accounts, are pivotal for recording revenue, expenses, gains, and losses within a specific accounting timeframe, typically a fiscal year. At the close of each period, temporary accounts undergo closure, wherein their balances are shifted to the retained earnings or income summary account, ensuring a fresh start for the subsequent period. Conversely, alternatively known as real accounts, permanent accounts encapsulate balance sheet elements like assets, liabilities, and equity. These accounts exhibit a contrasting characteristic to temporary ones, maintaining their balances across accounting periods and providing a continuous snapshot of the company's financial standing. This perpetual nature of permanent accounts is fundamental in upholding the ongoing precision and credibility of a company's financial records, furnishing a steadfast long-term perspective on its economic well-being.

In accounting, understanding the roles of temporary and permanent accounts is essential for managing a company's financial transactions and preparing comprehensive financial statements. Temporary accounts, also termed nominal accounts, are pivotal for recording revenue, expenses, gains, and losses within a specific accounting timeframe, typically a fiscal year. At the close of each period, temporary accounts undergo closure, wherein their balances are shifted to the retained earnings or income summary account, ensuring a fresh start for the subsequent period. Conversely, alternatively known as real accounts, permanent accounts encapsulate balance sheet elements like assets, liabilities, and equity. These accounts exhibit a contrasting characteristic to temporary ones, maintaining their balances across accounting periods and providing a continuous snapshot of the company's financial standing. This perpetual nature of permanent accounts is fundamental in upholding the ongoing precision and credibility of a company's financial records, furnishing a steadfast long-term perspective on its economic well-being.

Contents

Why Is It Important to Understand the Difference between a Temporary Account and a Permanent Account?

Understanding Temporary Accounts:

Understanding Permanent Accounts:

Specific Accounts Analysis

Practical Application in Accounting

Conclusion

FAQs

Why Is It Important to Understand the Difference between a Temporary Account and a Permanent Account?

Distinguishing between temporary and permanent accounting accounts is crucial for comprehensively understanding a company's financial health and performance. Temporary accounts cover revenue, expenses, gains, and losses and provide valuable insights into short-term financial activities. These insights are essential for evaluating profitability within specific accounting periods. In contrast, permanent accounts, which include assets, liabilities, and equity, maintain a continuous record of the company's financial standing. This constant record supports long-term strategic decision-making and financial planning efforts. Differentiating between temporary and permanent accounts allows stakeholders to distinguish between short-term fluctuations and enduring financial trends, ensuring accurate analysis and informed decision-making processes. By recognizing the distinct roles of temporary and permanent accounts, businesses can effectively manage their finances, uphold transparency, and foster sustainable growth strategies.

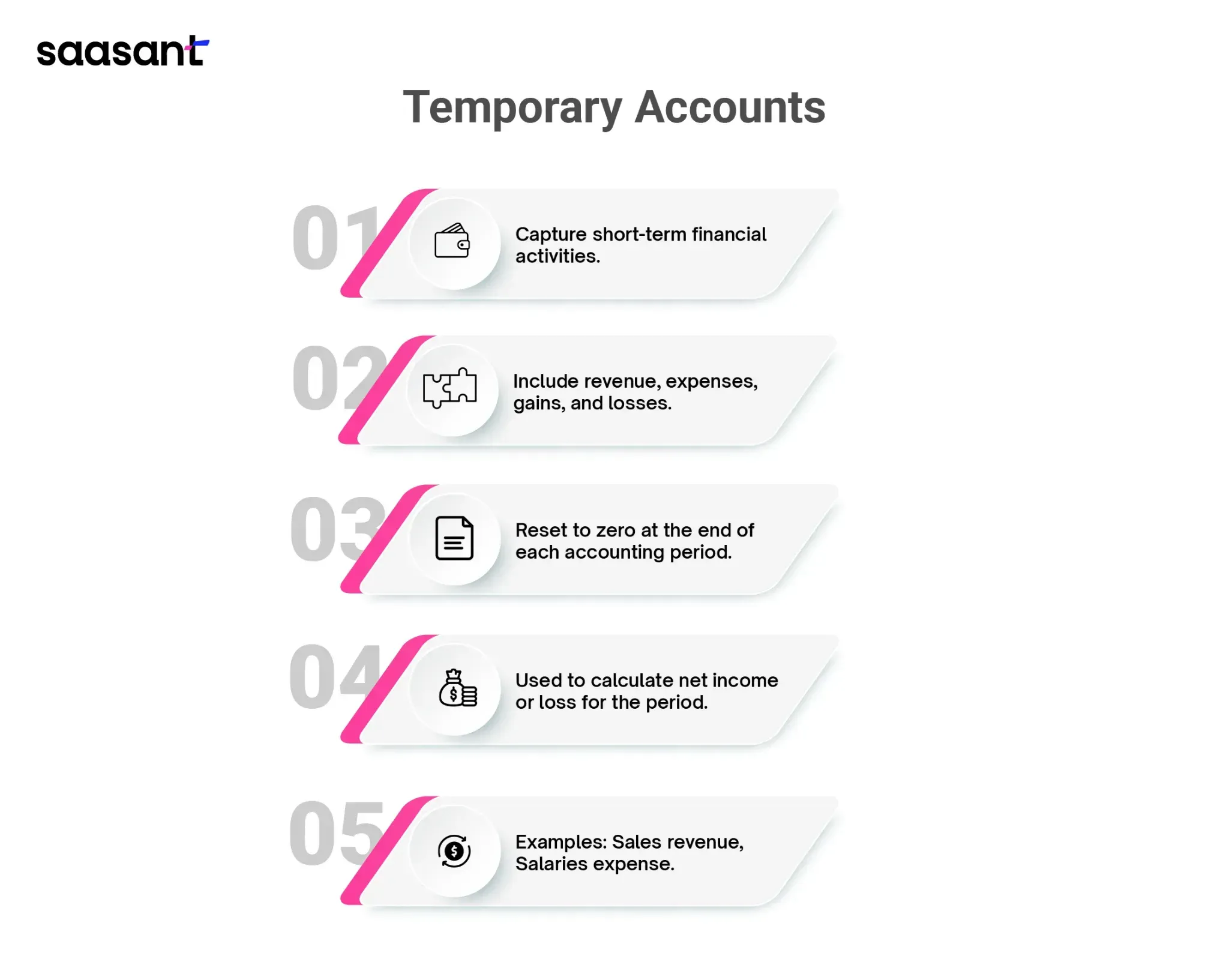

Understanding Temporary Accounts:

Temporary accounts are vital in accounting, capturing revenue, expenses, gains, and losses within a specific period and assessing a business's financial performance. These accounts are crucial for tracking financial activities over defined timeframes, such as months, quarters, or fiscal years. At the beginning of each accounting period, temporary accounts are opened to monitor the flow of revenues and expenses. Subsequently, they are closed at period-end to pave the way for the next reporting cycle.

The primary objective of temporary accounts is to gauge a business's net income or net loss during the accounting period. Revenue accounts, such as sales or service revenue, document income generated from core operations, while expense accounts, like salaries or utilities, track costs linked to revenue generation. Companies ascertain their net income or loss by deducting total expenses from revenues.

Temporary accounts offer structured categorization of financial transactions, simplifying income and expense tracking and aiding in profitability assessment. They furnish valuable insights into a company's financial health, assisting management in resource allocation, budgeting, and strategic planning endeavors.

Examples of temporary accounts encompass revenue accounts and expense accounts.

Revenue accounts document various income sources, such as sales revenue, service revenue, interest income, rental income, and royalties. These accounts are pivotal for evaluating a company's revenue generation capability and financial well-being. At period-end, balances in revenue accounts are closed to prepare for the subsequent reporting cycle, ensuring precise financial reporting and analysis.

Expense accounts track costs incurred by a business in its day-to-day operations. These accounts cover a broad spectrum of costs, including operating expenses (e.g., rent, utilities, salaries), cost of goods sold (e.g., materials, labor), depreciation and amortization, and interest expenses. By monitoring expenses, companies can identify areas for cost optimization and enhance profitability. Like revenue accounts, expense account balances are closed at the end of the accounting period, ensuring accurate financial reporting and analysis.

Income Summary accounts are temporary accounts employed in the closing process of the accounting cycle. They summarize revenues and expenses before transferring the net income or loss to permanent accounts like retained earnings or owner's equity. Income Summary accounts serve as transitional entities to facilitate accurate financial reporting and seamless transition between accounting periods.

In essence, temporary accounts are instrumental in capturing a business's financial performance, organizing financial data, and supporting decision-making processes. Closing these accounts at period-end ensures accurate financial reporting and primes the business for subsequent accounting periods.

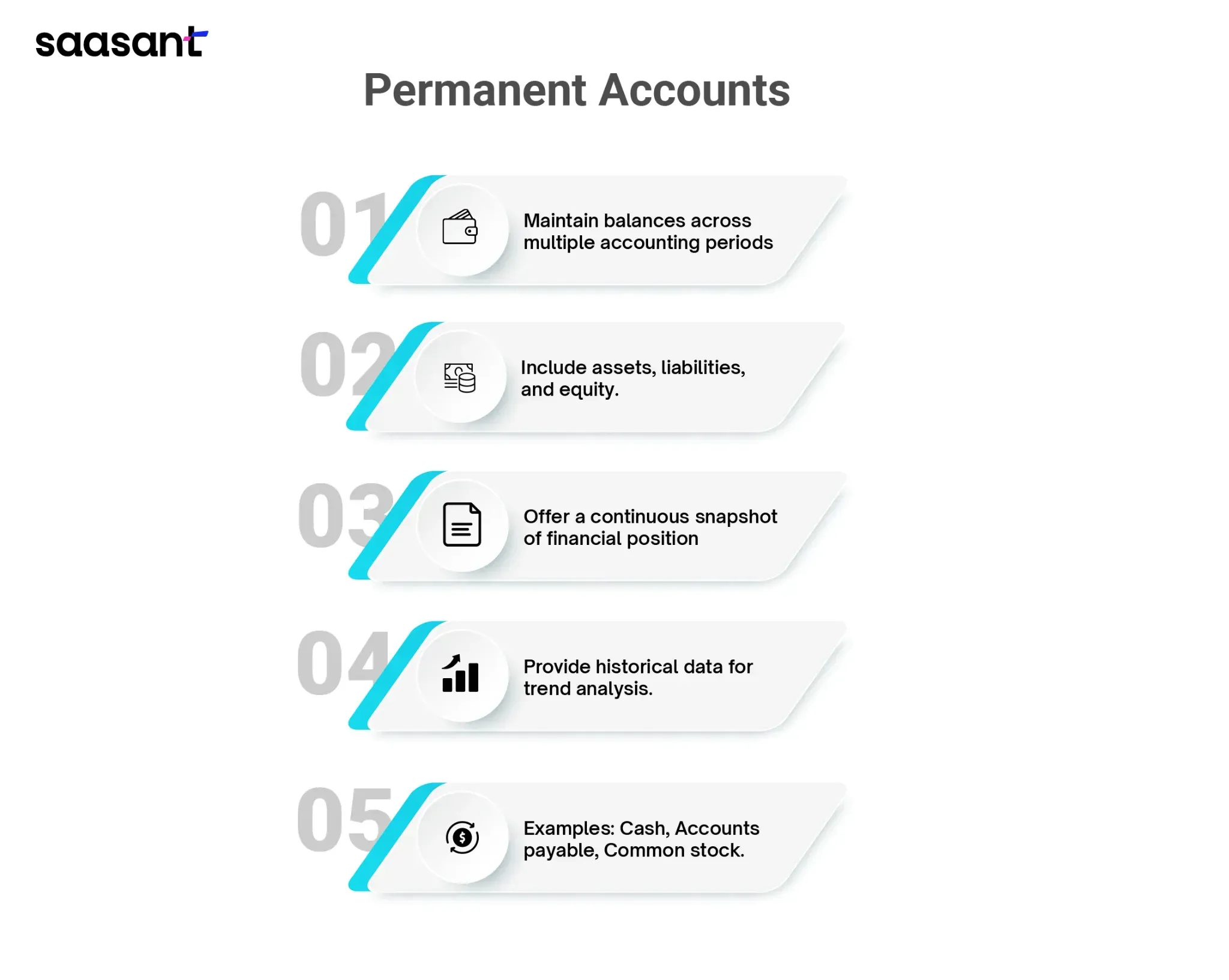

Understanding Permanent Accounts:

Permanent or real accounts are integral to a company's financial framework, persisting beyond individual accounting periods. Unlike temporary accounts, which capture transactions specific to a period, permanent accounts maintain balances over time, offering a continuous snapshot of a company's financial standing. They serve crucial functions in financial reporting and are pivotal for assessing long-term economic viability.

Purpose of Permanent Accounts:

Record Financial Position: Permanent accounts encompass balance sheet items like assets, liabilities, and equity, reflecting the company's financial standing at a given time. They provide insights into asset ownership, liabilities, and equity structure.

Provide Historical Data: Permanent accounts accumulate transactions over multiple periods, forming a historical record of the company's financial activities. This historical data aids stakeholders in trend analysis, tracking changes in economic performance, and making informed decisions about the company's future direction.

Support Financial Analysis: Permanent accounts offer a comprehensive view of the company's financial condition, facilitating financial analysis. Investors, creditors, and stakeholders use information from permanent accounts to assess profitability, liquidity, solvency, and overall economic stability.

Examples of Permanent Accounts:

Assets: Permanent accounts include cash, accounts receivable, inventory, property, plant, equipment (PP&E), and intangible assets such as patents and trademarks. These assets represent resources contributing to the company's value and future income generation.

Liabilities: Permanent accounts include liabilities like accounts payable, loans payable, bonds payable, and accrued expenses. These accounts indicate the company's obligations to creditors and other entities, requiring repayment or fulfillment over time.

Equity: Permanent accounts comprise equity accounts like common stock, retained earnings, and additional paid-in capital. Equity accounts portray shareholders' ownership interests and reflect cumulative profits or losses retained in the business.

Ongoing Nature and Role in Financial Reporting:

Permanent accounts play a critical role in financial reporting by furnishing essential information for preparing the balance sheet and summarizing the company's financial position at a specific moment. Unlike temporary accounts, closed at period end, permanent accounts maintain their balances across periods.

The ongoing nature of permanent accounts ensures continuity and consistency in financial reporting. Balances in permanent accounts persist over time, facilitating the seamless accumulation of economic data. This continuity enables stakeholders to track financial position changes, monitor long-term trends, and make informed decisions about investment, financing, and operational strategies.

In essence, permanent accounts form the bedrock of a company's financial reporting, providing a continuous record of financial position, historical performance, and ownership structure. By maintaining balances over time, permanent accounts uphold transparency, accountability, and informed decision-making, which is crucial for effective business management and governance.

Identifying Permanent Accounts:

Permanent or non-temporary accounts are integral elements of a company's financial framework that persist across accounting periods. In contrast to temporary accounts, which document transactions within specific periods, permanent accounts retain their balances over time, offering a continuous overview of a company's financial health. Identifying permanent accounts entails recognizing balance sheet items that endure beyond individual accounting cycles, including assets, liabilities, and equity accounts.

Common Characteristics of Permanent Accounts:

Enduring Balances: Permanent accounts uphold their balances over multiple accounting periods, unlike temporary accounts, which reset after each period. This feature provides a perpetual snapshot of the company's financial position.

Long-Term Financial Position Reflection: These accounts mirror a company's enduring financial status by encompassing assets, liabilities, and equity items that transcend short-term transactions. Permanent accounts offer insights into asset ownership, financial obligations, and shareholders' equity interests.

Integral to Financial Reporting: Permanent accounts are crucial in financial reporting, supplying vital data for preparing balance sheets. This information aids stakeholders, investors, and creditors in decision-making by providing insights into the company's financial condition.

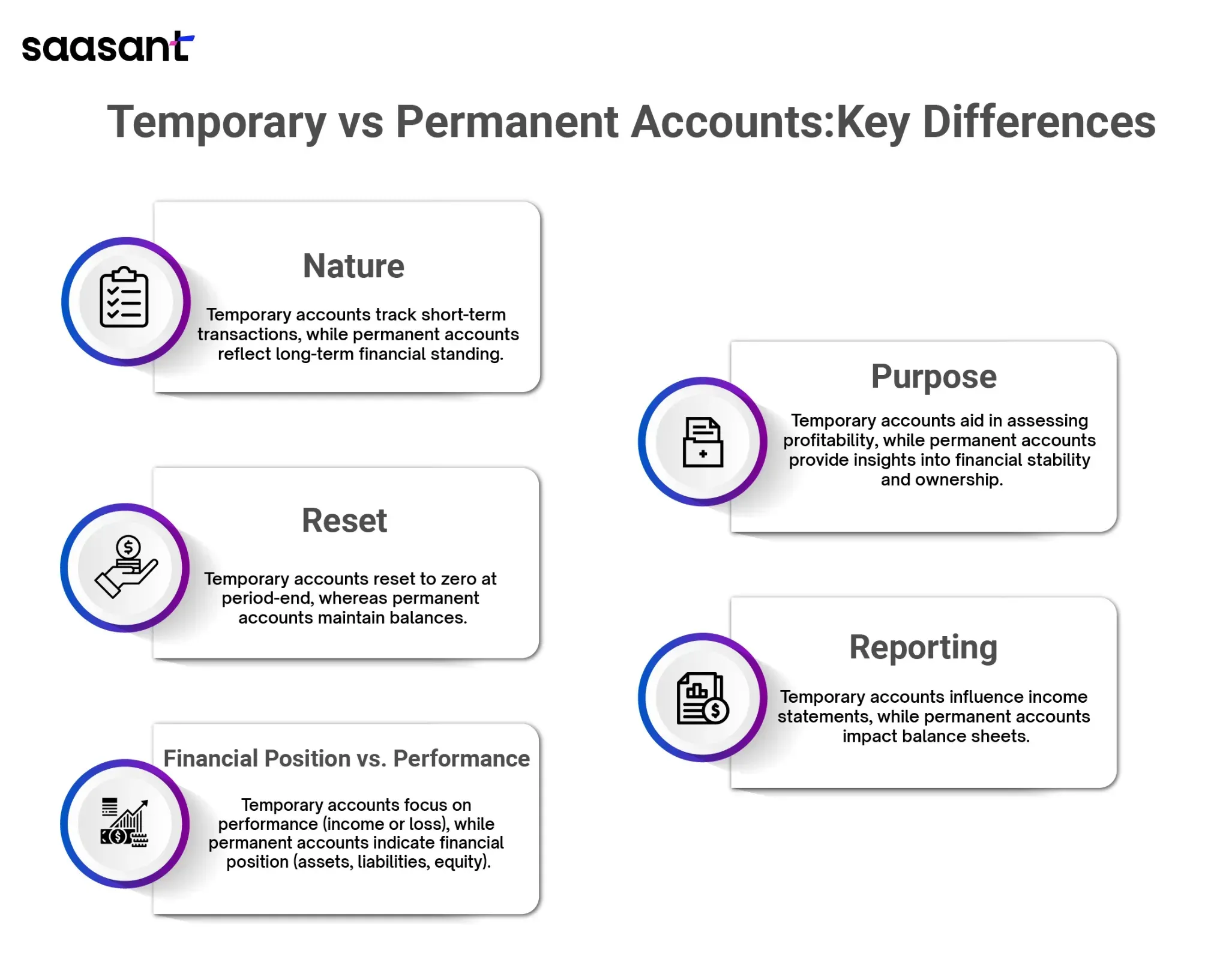

Key Differences from Temporary Accounts:

Balance Continuation: Permanent accounts maintain their balances from one accounting period to the next, whereas temporary accounts reset to zero at period-end.

Transaction Scope: Permanent accounts capture long-term financial transactions such as asset acquisitions, debt issuances, and equity investments. Conversely, temporary accounts focus on short-term revenue, expense, gain, and loss transactions specific to each period.

Financial Position vs. Performance: Permanent accounts depict a company's financial position by reflecting assets, liabilities, and equity items that persist over time. Temporary accounts, however, concentrate on economic performance by capturing revenue and expense transactions to determine net income or loss for a specific period.

Examples of Permanent Accounts:

Assets: Permanent accounts encompass various asset categories that extend beyond individual accounting periods, including:

Cash: Liquid funds available for operational and investment purposes.

Inventory: Goods held for sale or raw materials used in production.

Equipment: Tangible assets like machinery, vehicles, and furniture utilized in business operations.

Liabilities: These accounts comprise long-term financial obligations persisting beyond short-term transactions, such as:

Loans Payable: Long-term borrowings from financial institutions or creditors, with repayment terms extending beyond one year.

Accounts Payable: Amounts owed to suppliers or vendors for goods or services purchased on credit.

Equity Accounts: Permanent accounts include equity items portraying shareholders' interests and cumulative profits or losses retained in the business, such as:

Common Stock: Ownership shares issued to shareholders, granting them voting rights and dividends.

Retained Earnings: Cumulative profits or losses retained after distributing dividends to shareholders.

Identifying permanent accounts entails recognizing balance sheet items that endure across accounting periods, offering a continuous record of a company's financial position. These accounts maintain enduring balances, reflect long-term financial positions, and play a pivotal role in financial reporting. Examples encompass assets like cash, inventory, and equipment, liabilities like loans and accounts payable, and equity accounts like common stock and retained earnings.

Specific Accounts Analysis

Is Interest Income a Temporary Account?

Yes, interest income is typically considered a temporary account in accounting. Temporary accounts capture transactions specific to a particular accounting period and are reset to zero at the end of each period for financial reporting purposes. Interest income represents a company's earnings from interest-bearing assets such as savings accounts, bonds, or loans. Since interest income accrues over a short period and is directly related to specific financial transactions, it falls under temporary accounts. At the end of the accounting period, the balance in the interest income account is closed, and its balance is transferred to a permanent account, typically retained earnings or income summary, to begin anew in the next period.

Is Salaries Expense a Temporary Account?

Yes, salary expense is considered a temporary account in accounting. Temporary accounts track revenue, expenses, gains, and losses for a specific accounting period, typically one fiscal year. Salaries expense represents the amount a company pays its employees for services rendered during a particular period, such as a month or a year. Since salaries expense reflects expenses incurred within a specific timeframe and are reset to zero at the end of each accounting period, they fall under the temporary accounts category. At the end of the period, the balance in the salaries expense account is closed, and its balance is transferred to a permanent account, usually retained earnings or income summary, to start anew in the subsequent period.

Is Service Revenue a Temporary Account?

Yes, service revenue is typically considered a temporary account in accounting. Temporary accounts track revenue, expenses, gains, and losses for a specific accounting period, usually one fiscal year. Service revenue represents the income generated by a company from providing services to its customers during a particular period, such as a month or a year. Since service revenue reflects revenue earned within a specific timeframe and is reset to zero at the end of each accounting period, it falls under the category of temporary accounts. At the end of the period, the balance in the service revenue account is closed, and its balance is transferred to a permanent account, usually retained earnings or income summary, to start anew in the subsequent period.

Are Dividends a Temporary Account?

No, dividends are not considered temporary accounts in accounting. Temporary accounts track revenue, expenses, gains, and losses for a specific accounting period, typically one fiscal year. Dividends represent distributions of a company's earnings to its shareholders. Unlike temporary accounts, dividends are not reset to zero at the end of each accounting period. Instead, dividends are recorded as distributions of profits and are typically classified as a reduction of retained earnings within the equity section of the balance sheet. Unlike temporary accounts, retained earnings carry forward balances from one period to the next, reflecting the cumulative profits or losses retained in the business. Therefore, dividends are classified as a permanent account in accounting, as they reflect a company's long-term financial activities rather than short-term transactions.

Is Common Stock a Permanent Account?

Yes, common stock is considered a permanent account in accounting. Permanent accounts maintain their balances across multiple accounting periods, providing a continuous record of a company's financial position. Common stock represents the equity ownership stake held by shareholders in a company. Unlike temporary accounts, which capture short-term transactions specific to a particular period, common stock reflects a long-term ownership interest in the company. The balance in the common stock account is not reset to zero at the end of each accounting period but carries forward from one period to the next. It is classified as a permanent account because it reflects the enduring ownership structure of the company, representing the initial investment made by shareholders and any subsequent changes in ownership through stock issuance or repurchases.

Is Service Revenue a Permanent Account?

No, service revenue is not considered a permanent account in accounting. Permanent accounts maintain their balances across multiple accounting periods, providing a continuous record of a company's financial position. On the other hand, service revenue is a temporary account that captures revenue earned from providing services to customers during a specific period, such as a month or a year. For financial reporting purposes, temporary accounts are reset to zero at the end of each accounting period. Service revenue represents income generated from the company's primary operations. It is closed at the end of the period, with its balance transferred to a permanent account, typically retained earnings or income summary, to start anew in the subsequent period. Therefore, service revenue is classified as temporary, reflecting short-term revenue transactions rather than the company's long-term financial position.

Practical Application in Accounting

The Impact of Account Classification on Financial Statements and Business Decision-Making

Classifying accounts as temporary or permanent significantly impacts financial statements and business decision-making processes. Temporary accounts, covering revenue, expenses, gains, and losses, undergo closure at the end of each accounting period to determine the net income or loss for that specific period. Conversely, permanent accounts, comprising assets, liabilities, and equity, maintain balances throughout accounting periods, offering a consistent overview of a company's financial standing. This classification ensures precise and transparent reporting in financial statements, enabling stakeholders to evaluate short-term performance and long-term economic stability. Additionally, classifying accounts influences business decisions by providing insights into revenue streams, expenditure trends, asset management, and debt handling. Analyzing data from temporary and permanent accounts empowers stakeholders to make informed choices regarding resource allocation, investment strategies, operational enhancements, and risk management initiatives, fostering business growth and sustainability.

Closing Temporary Accounts and Transferring to Permanent Accounts

Closing temporary accounts and transferring their balances to permanent accounts is a crucial step in the accounting cycle at the end of each accounting period. Temporary accounts include revenue, expense, gain, and loss, which capture transactions specific to a particular period. These accounts are reset to zero at the end of each period to prepare for the next reporting cycle, while permanent accounts, such as assets, liabilities, and equity accounts, maintain their balances across multiple accounting periods.

The process of closing temporary accounts involves several steps:

Identifying Temporary Accounts: The first step is to identify all temporary accounts that must be closed. These typically include revenue accounts (e.g., sales revenue, service revenue) and expense accounts (e.g., salaries expense, utilities expense).

Determining Net Income or Net Loss: Next, the balances of all revenue and expense accounts are summarized to calculate the net income or net loss for the period. This involves adding up all revenues and subtracting all expenses.

Transferring Balances to Income Summary Account: The net income or net loss amount is then transferred to an intermediate account. If the total revenue exceeds total expenses, resulting in a net income, this amount is credited to the Income Summary account. Conversely, if expenses exceed revenue, resulting in a net loss, this amount is debited to the Income Summary account.

Closing Revenue Accounts: After transferring the net income or net loss to the Income Summary account, all revenue accounts are closed by debiting each revenue account and crediting the Income Summary account for the total amount of revenue.

Closing Expense Accounts: All expense accounts are closed by crediting each account and debiting the Income Summary account for the total expenses.

Closing Income Summary Account: Once all revenue and expense accounts are closed, the balance remaining in the Income Summary account represents the net income or net loss for the period. This balance is transferred to a permanent account, typically retained earnings for corporations or the owner's equity account for sole proprietorships and partnerships.

Verification and Adjustment: Finally, the closing entries are verified to ensure accuracy, and any necessary adjustments are made before the financial statements are prepared for the next accounting period.

By following these steps, temporary accounts are closed, and their balances are transferred to permanent accounts, providing a clear picture of the company's financial performance and position for the period. This process ensures accurate financial reporting and prepares the company for the subsequent accounting cycle.

Conclusion

Understanding the distinction between temporary and permanent accounts is paramount in managing a company's financial records and preparing accurate financial statements. Temporary accounts, capturing revenue, expenses, gains, and losses within specific accounting periods, provide insights into short-term financial activities and aid in evaluating profitability. In contrast, permanent accounts, encompassing assets, liabilities, and equity, offer a continuous record of a company's financial position, supporting long-term strategic decision-making and financial planning efforts, classifying accounts as temporary or permanent influences financial statements by ensuring accuracy and transparency in reporting, enabling stakeholders to assess short-term performance and long-term financial health. Moreover, this classification impacts business decision-making by providing insights into revenue sources, expense patterns, asset utilization, and debt management. By analyzing data from temporary and permanent accounts, stakeholders can make informed decisions about resource allocation, investment strategies, operational improvements, and risk mitigation efforts, ultimately fostering business growth and sustainability. Therefore, understanding and appropriately classifying accounts as temporary or permanent are vital to effective financial management and decision-making processes in any organization.

FAQs

What are temporary accounts, and why are they important?

Temporary or nominal accounts record revenue, expenses, gains, and losses within specific accounting periods. They are crucial for assessing short-term financial performance and profitability.

How do temporary accounts differ from permanent accounts?

Temporary accounts capture transactions for a specific period and are closed at the end of each accounting period. In contrast, permanent accounts maintain balances over multiple periods, offering continuous insights into a company's financial position.

What types of transactions do temporary accounts cover?

Temporary accounts include revenue accounts (e.g., sales revenue, service revenue) and expense accounts (e.g., salaries expense, utilities expense), tracking income and costs related to a specific time frame.

Can you provide examples of temporary accounts?

Examples of temporary accounts include revenue accounts (e.g., sales revenue, service revenue) and expense accounts (e.g., salaries expense, utilities expense), which reflect short-term financial activities.

What is the purpose of closing temporary accounts?

Closing temporary accounts involves transferring their balances to permanent accounts to prepare for the next accounting period. This process ensures accurate financial reporting and resets temporary account balances for the new period.

How do permanent accounts differ from temporary accounts?

Permanent or real accounts maintain balances over multiple accounting periods, including assets, liabilities, and equity. They offer a continuous snapshot of a company's financial position.

Why are permanent accounts essential for financial reporting?

Permanent accounts provide insights into a company's long-term financial health by reflecting assets, liabilities, and equity items that endure over time. They support accurate financial reporting and decision-making.

Can you give examples of permanent accounts?

Examples of permanent accounts include asset accounts (e.g., cash, inventory), liability accounts (e.g., accounts payable, loans payable), and equity accounts (e.g., common stock, retained earnings).

How does the classification of accounts impact financial statements?

Classifying accounts as temporary or permanent influences financial statements by ensuring accuracy and transparency. Temporary accounts reflect short-term performance, while permanent accounts provide a continuous overview of a company's financial position.

What is the significance of understanding temporary and permanent accounts in business decision-making?

Understanding temporary and permanent accounts aids stakeholders in making informed decisions about resource allocation, investment strategies, operational improvements, and risk mitigation efforts. It provides insights into both short-term performance and long-term financial health.