Why It’s Essential to Reconcile Your Bank Statements Regularly?

When it comes to financial management, bank reconciliation is one of those essential tasks that often gets overlooked. However, it is crucial to keep your financial records accurate and reliable. Bank reconciliation involves comparing your financial records, whether personal or business, against your bank statements to catch any discrepancies. This practice is not just a good idea; it’s fundamental to ensuring your finances are in order.

Contents

Why Bank Reconciliation Matters for Everyone?

How It Ensures Financial Accuracy and Prevents Bigger Problems?

What is Bank Reconciliation? A Simple Explanation

Importance of Regular Bank Reconciliation: Key Benefits

The Risks of Neglecting Bank Reconciliation

Common Issues Encountered During Bank Reconciliation

Steps for Effective Bank Reconciliation

Leveraging Technology for Efficient Bank Reconciliation

Enhancing Financial Reporting Through Bank Reconciliation

Bank Reconciliation and Financial Planning

How Regular Bank Reconciliation Helps with Tax Preparation?

Best Practices for Ongoing Bank Reconciliation

Common Myths and Misconceptions About Bank Reconciliation

FAQs

Why Bank Reconciliation Matters for Everyone?

For individuals, regular bank reconciliation is vital for effective personal finance management. It helps you keep track of your spending habits, spot unauthorized transactions, and avoid unnecessary overdraft fees. When you take the time to reconcile your bank statements regularly, you get a clearer picture of your financial situation. This clarity leads to better budgeting decisions and more innovative financial planning.

On the business side, the stakes are even higher. For businesses, bank reconciliation isn’t just a recommendation; it’s a necessity. With a more complex financial landscape, businesses need accurate financial records to identify cash flow issues and streamline their accounting processes. Plus, it helps build trust with stakeholders, whether investors, clients, or employees, by showcasing a commitment to transparency and accountability.

How It Ensures Financial Accuracy and Prevents Bigger Problems?

The most significant benefit of bank reconciliation is that it promotes financial accuracy. By regularly comparing your financial records with your bank statements, you can catch mistakes, whether they’re due to accounting errors, fraudulent activities, or even bank errors. This proactive approach to financial oversight can save you from more significant issues that might arise later, such as cash flow problems, tax issues, or legal complications.

Think about it: knowing that your financial records are accurate gives you peace of mind. Regularly reconciling your bank statements allows you to focus on what matters most, your life or your business, without the nagging worry of potential financial discrepancies.

The Consequences of Neglecting This Important Task

Ignoring bank reconciliation can lead to severe consequences. For individuals, it might result in overspending, insufficient funds for essential bills, and a damaged credit score. For businesses, the stakes are even higher. Only accurate financial records can lead to good business decisions, cash flow crisis, and even legal troubles due to tax discrepancies.

What is Bank Reconciliation? A Simple Explanation

Bank reconciliation is a fundamental financial practice crucial in maintaining accurate records for personal and business finances. It involves comparing bank statements with accounting records to ensure everything aligns perfectly. Let’s delve deeper into what bank reconciliation entails, its purpose, and how it differs for businesses and individuals.

Definition and Purpose of Bank Reconciliation

At its core, bank reconciliation is verifying that the amounts in your accounting records match those in your bank statements. This verification is essential for several reasons:

Accuracy: The primary goal of bank reconciliation is to ensure the accuracy of financial records. You can correct errors that could otherwise lead to financial mismanagement by identifying discrepancies.

Fraud Detection: Regular reconciliation helps detect unauthorized transactions or fraud, providing an opportunity to address any suspicious activities promptly.

Financial Management: Bank reconciliation provides a clearer picture of financial health for individuals and businesses. It helps track spending, manage cash flow, and prepare for future financial decisions.

The Process of Matching Bank Statements with Accounting Records

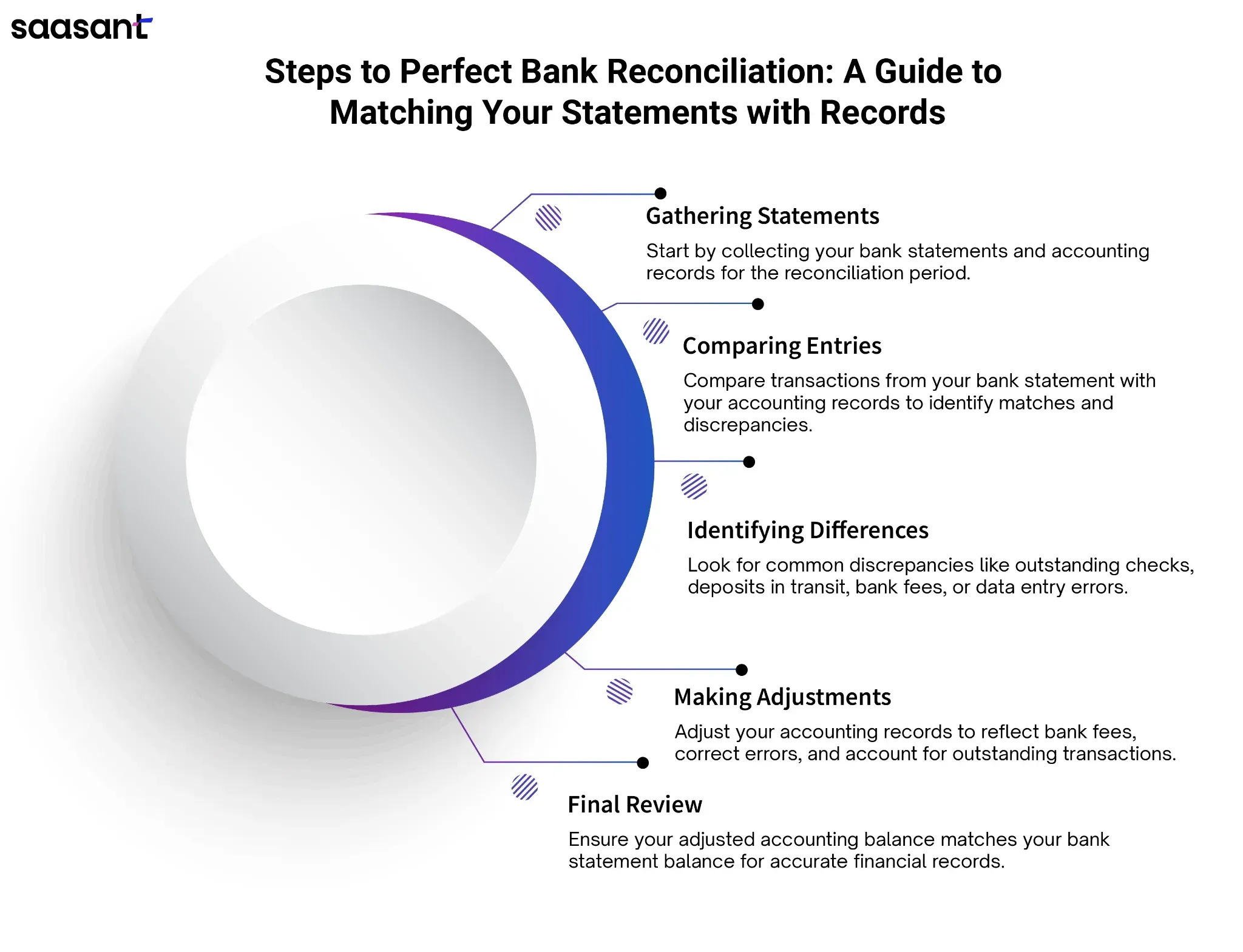

The bank reconciliation process typically involves the following steps:

Gathering Statements: Collect your bank statements for the period you wish to reconcile. Ensure you have your accounting records ready, including ledgers or software reports.

Comparing Entries: Start comparing the transactions in your bank statement with those in your accounting records. Mark each transaction that matches and take note of any discrepancies.

Identifying Differences: Common reasons for discrepancies include outstanding checks (checks written but still need to be cleared), deposits in transit (deposits made but not yet reflected in the bank statement), bank fees, and errors in data entry.

Making Adjustments: Once you identify the differences, make the necessary adjustments in your accounting records. This may involve correcting errors, recording bank fees, or adjusting for outstanding items.

Final Review: After adjustments, conduct a final comparison. Your adjusted accounting balance should now match the bank statement balance, confirming that your records are accurate.

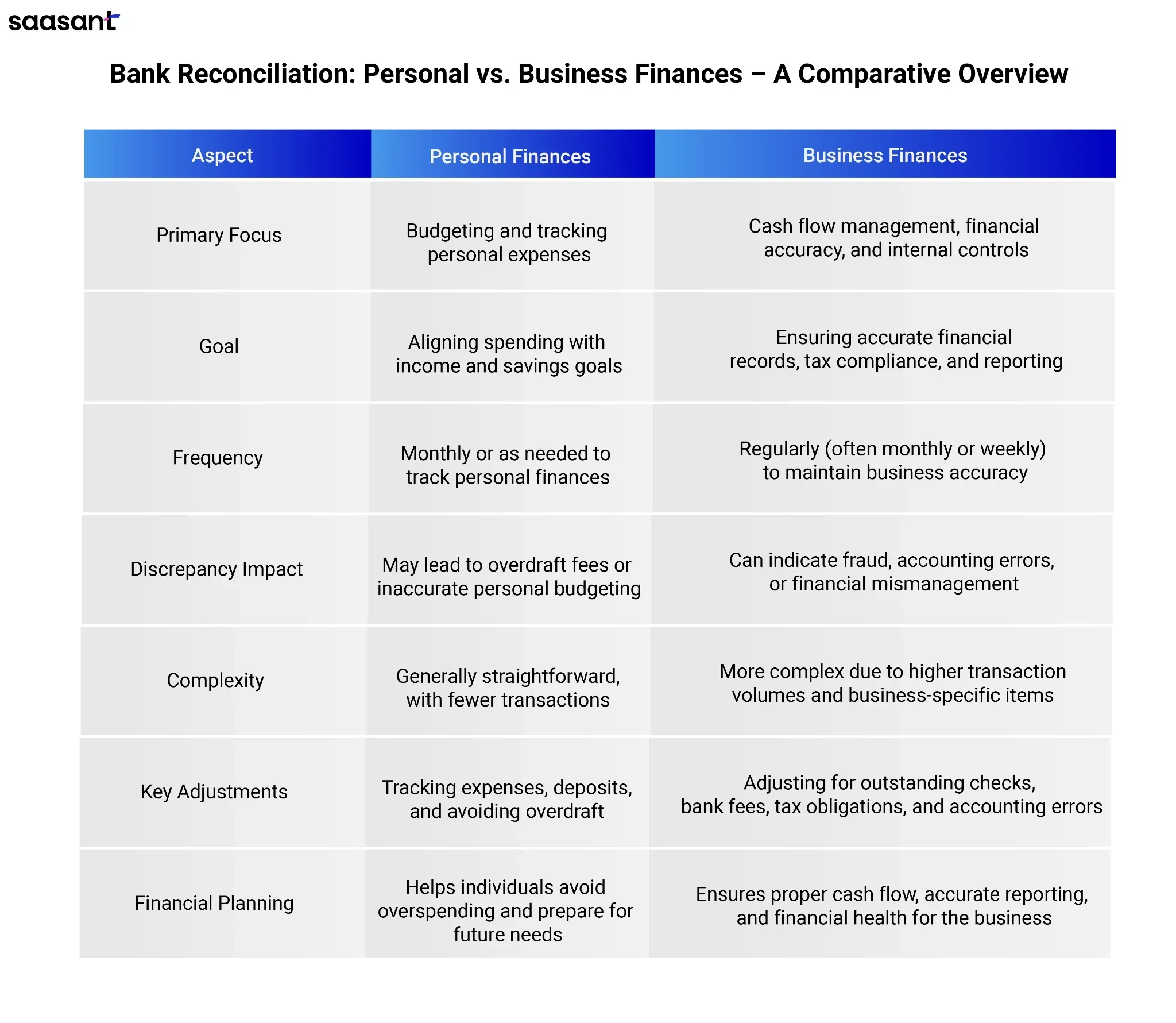

Difference Between Bank Reconciliation for Businesses vs. Personal Finances

While the fundamental process of bank reconciliation remains the same for businesses and personal finances, the context and implications can differ significantly.

Personal Finances: For individuals, bank reconciliation typically focuses on budgeting and tracking personal expenses. The primary goal is to manage personal finances effectively, ensuring that spending aligns with income and savings goals. It helps individuals avoid overdraft fees, track expenses, and plan for future financial needs.

Business Finances: Bank reconciliation is a critical internal control mechanism in a business context. It helps maintain accurate financial records and plays a key role in cash flow management, tax compliance, and financial reporting. For businesses, discrepancies may indicate more severe issues, such as fraudulent activities or significant accounting errors that could impact the organization's health.

Importance of Regular Bank Reconciliation: Key Benefits

Regular bank reconciliation is a mundane financial task and a cornerstone of effective financial management for individuals and businesses. By comparing your bank statements with your accounting records, you ensure that your financial information is accurate, transparent, and reliable. Let’s explore the key benefits of regular bank reconciliation and why it should be a priority in your financial routine.

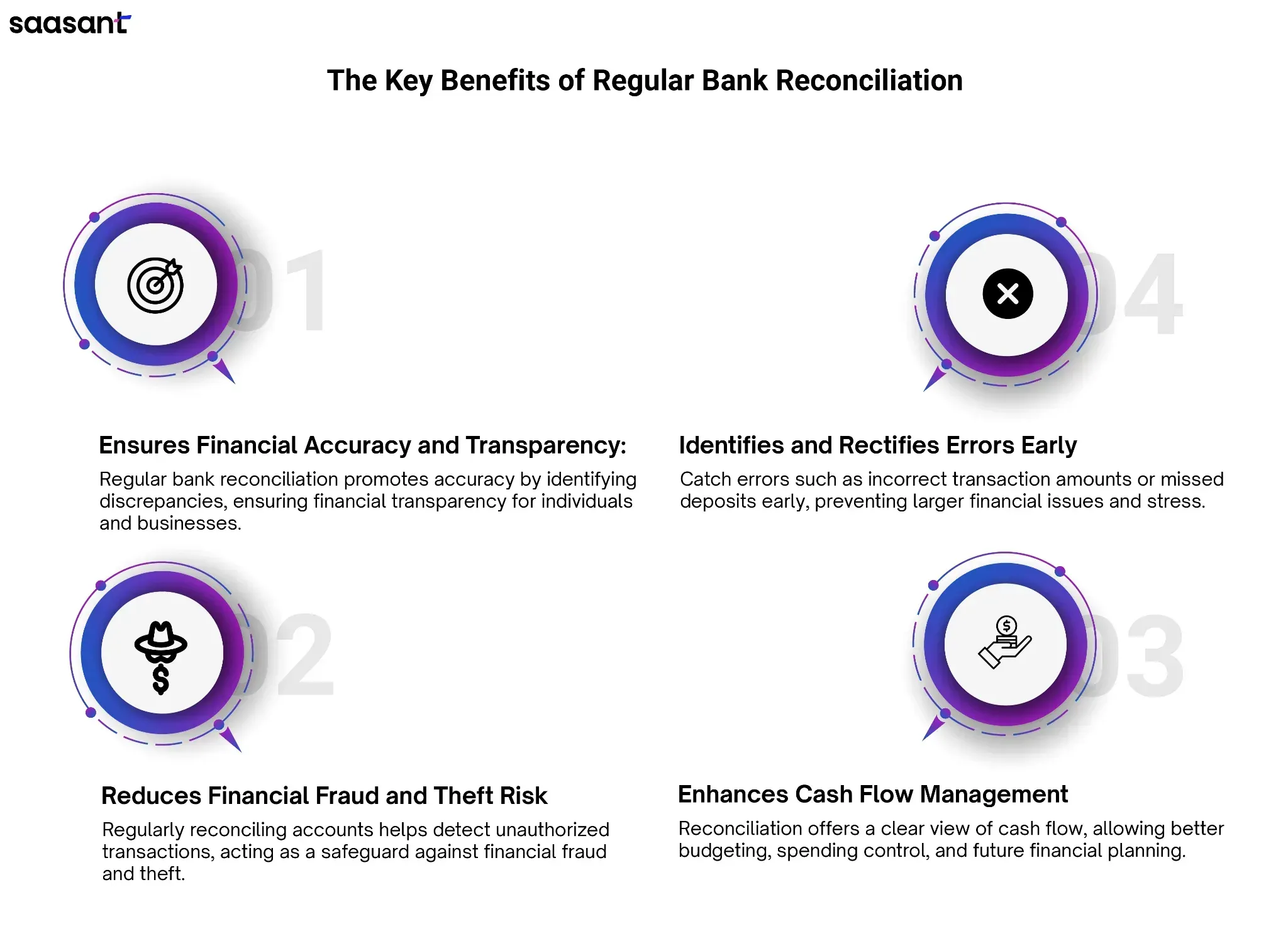

1. Ensures Financial Accuracy and Transparency

One of the most significant advantages of bank reconciliation is its role in promoting financial accuracy. Discrepancies between your bank statements and accounting records can arise for various reasons, such as data entry errors, timing differences, or bank fees. By regularly reconciling your accounts, you can quickly identify and correct these inconsistencies, ensuring that your financial records reflect true and accurate information. This transparency is vital for personal peace of mind and stakeholders, such as business partners or investors.

2. Identifies and Rectifies Errors Early

Mistakes happen, but they can be costly if not addressed promptly. Regular bank reconciliation allows you to identify and rectify errors early in the financial process. Whether it’s an incorrect transaction amount or a missed deposit, catching these errors early prevents more significant issues, such as cash flow problems or inaccurate financial reporting. You can avoid unnecessary stress and complications by managing your finances proactively.

3. Reduces Financial Fraud and Theft Risk

In an increasingly prevalent era of financial fraud, bank reconciliation is a critical safeguard against potential theft and unauthorized transactions. By routinely comparing your bank statements to your records, you can spot any unusual activities, such as withdrawals or transactions you did not authorize. This vigilant approach protects your assets and fosters a sense of security, knowing you have a system to detect fraudulent activities. Effective fraud detection through regular reconciliation ultimately helps maintain trust in your financial processes.

4. Enhances Cash Flow Management for Businesses and Individuals

Cash flow management is essential for maintaining financial health for individuals and businesses. Regular bank reconciliation provides insights into your financial status, helping you understand your cash flow patterns. You can make informed spending, saving, and investing decisions by accurately tracking incoming and outgoing funds. This enhanced visibility allows for better budgeting and planning, ensuring that you have sufficient funds for future needs and can avoid potential shortfalls.

The Risks of Neglecting Bank Reconciliation

While regular bank reconciliation is crucial for maintaining financial health, neglecting this essential practice can lead to significant risks impacting individuals and businesses. Understanding these risks can motivate you to prioritize reconciliation as part of your financial management routine. Let’s explore the critical consequences of neglecting bank reconciliation.

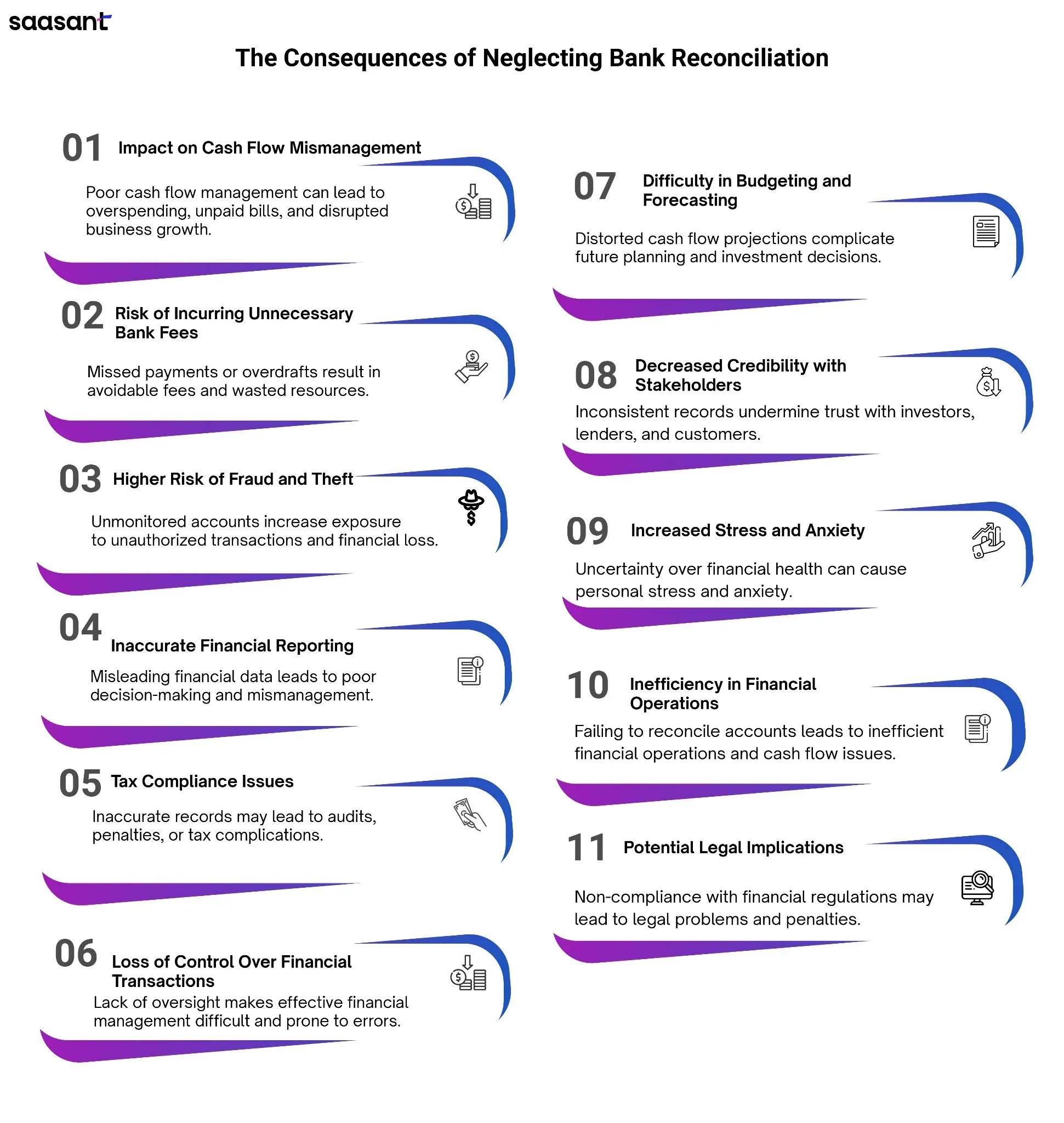

1. Impact on Cash Flow Mismanagement

Cash flow mismanagement is one of the most immediate effects of neglecting bank reconciliation. Regular updates to your financial records make maintaining an accurate picture of your available funds easier. This can lead to overspending, resulting in insufficient cash flow to meet essential obligations such as paying bills or making payroll. For businesses, cash flow problems can disrupt operations, hinder growth, and ultimately impact profitability. Personal finances may mean missing out on savings opportunities or incurring debt due to unplanned expenses.

2. Risk of Incurring Unnecessary Bank Fees and Penalties

Neglecting reconciliation can also lead to unnecessary bank fees and penalties. When transactions are not tracked properly, you may miss critical payments or overdraft your account, triggering fees that could have easily been avoided. Additionally, failing to identify recurring charges or subscriptions can result in wasted resources over time. By ensuring that your financial records are accurate and up-to-date, you can effectively manage your accounts and steer clear of these avoidable expenses.

3. Exposure to Higher Risk of Fraud and Theft Due to Unmonitored Accounts

Another critical risk of neglecting bank reconciliation is the increased exposure to fraud and theft. Unmonitored accounts can become prime targets for fraudulent activities, as unauthorized transactions may go unnoticed for extended periods. Regularly reviewing your bank statements against your accounting records lets you detect any irregularities promptly. Failing to reconcile your accounts leaves you vulnerable to financial loss, which can have long-lasting effects on your financial stability.

4. Inaccurate Financial Reporting

With regular reconciliation, the financial statements may accurately reflect the organization's or individual's financial position. This can lead to poor decision-making based on incorrect data.

5. Tax Compliance Issues

Inaccurate records can complicate tax preparation and filing, leading to errors that may trigger audits or penalties from tax authorities. More clarity in financial transactions is needed to avoid underreporting income or over-claiming deductions.

6. Loss of Control Over Financial Transactions

Neglecting reconciliation can cause a loss of oversight regarding financial transactions. This lack of control can hinder the ability to manage finances effectively and may lead to financial mismanagement over time.

7. Difficulty in Budgeting and Forecasting

An accurate understanding of financial health is crucial for effective budgeting and forecasting. Paying attention to bank reconciliation can distort cash flow projections, making planning for future expenses and investments challenging.

8. Decreased Credibility with Stakeholders

For businesses, inconsistent financial records can undermine credibility with stakeholders, including investors, lenders, and customers. Trust is vital for business relationships, and poor financial practices can erode that trust.

9. Increased Stress and Anxiety

On a personal level, failing to reconcile accounts can lead to increased stress and anxiety over financial matters. Uncertainty about one's financial situation can make feeling secure and planning for the future challenging.

10. Inefficiency in Financial Operations

Regular bank reconciliation contributes to streamlined financial processes. Neglecting this task can result in inefficiencies, complicating cash flow management and operational effectiveness.

11. Potential Legal Implications

In some cases, failing to keep accurate financial records can lead to legal issues, mainly if the discrepancies result in non-compliance with financial regulations or contractual obligations.

Common Issues Encountered During Bank Reconciliation

Bank reconciliation is vital for maintaining accurate financial records, but it is challenging. Understanding the common issues during reconciliation can help you navigate the process more smoothly. In this section, we will explore these common reconciliation issues, their causes, and strategies for resolution.

1. Timing Differences: Transactions Recorded in Different Periods

One of the most prevalent issues during bank reconciliation is timing differences. This occurs when transactions are recorded in different accounting periods. For instance, a deposit made at the end of the month may only appear in the bank statement in the following month. Similarly, checks written may take time to clear the bank, leading to discrepancies in your records.

Solution: To manage timing differences, clearly understand your transaction timeline. Keep a calendar of outstanding deposits and checks to monitor their expected clearing dates. This awareness will help you accurately reconcile your accounts.

2. Unrecognized Transactions: Misunderstanding or Forgetting Transactions

Another common issue is unrecognized transactions, which may result from misunderstandings or forgetting certain transactions. This can include automated payments or transfers that you may need to remember to authorize.

Solution: Review your transaction history regularly and ensure you know all payments and receipts. Use financial software that provides notifications for recurring transactions to track them efficiently.

3. Bank Errors: Banks Can Make Mistakes Too

It’s essential to remember that banks can also make mistakes. Errors can occur in transaction postings or fees charged, leading to discrepancies between your records and the bank statement. While rare, bank errors can complicate the reconciliation process.

Solution: If you suspect a bank error, contact your bank immediately. Maintain meticulous records of your transactions and be prepared to provide evidence of any discrepancies. Regularly reviewing your statements will help you identify such errors quickly.

4. Unanticipated Fees and Charges: Unrecorded Fees

Unanticipated fees can catch many individuals and businesses off guard. These may include monthly maintenance fees, ATM charges, or overdraft fees that have yet to be accounted for in your financial records.

Solution: Review your bank statements in detail each month. Keep a log of fees so you can factor them into your financial planning. If you frequently encounter unexpected charges, consider switching to a bank with lower fees or no monthly maintenance costs.

5. Duplicate or Missing Entries

Finally, duplicate or missing entries can lead to significant issues during reconciliation. Duplicate entries may occur due to data entry errors or importing transactions multiple times while missing entries can result from oversight or failure to record a transaction.

Solution: To avoid duplicates, implement a systematic method for entering and reviewing transactions. Financial software often includes features to detect duplicates, making this process easier. Regularly audit your entries to identify any missing transactions and rectify them promptly.

Steps for Effective Bank Reconciliation

Bank reconciliation is crucial for maintaining financial accuracy for personal or business finances. A structured and systematic approach is essential to ensure that your financial records align with your bank statements. This section will walk you through a step-by-step guide to performing bank reconciliation and share best practices to make the process smoother. By incorporating these steps into your routine, you can achieve financial clarity and reduce the risk of discrepancies.

Step-by-Step Guide to Performing Bank Reconciliation

1. Review Your Bank Statement

The first step in the reconciliation process is to obtain your bank statement. This document lists all the transactions recorded by your bank during a specific period. Ensure that you have the correct statement for the period you’re reconciling, and gather any supplementary documents that may be needed, such as receipts or invoices.

Tip: Most banks now offer online statements, which are more accessible to download, review, and store for future reference.

2. Cross-Check Transactions

Once you have your bank statement, compare it against your accounting records. This involves matching each transaction listed on the bank statement with corresponding entries in your financial records. Look for deposits, withdrawals, payments, and fees. Make sure everything matches.

Tip: Think of this step as playing a matching game; each entry in your accounting system should have a corresponding partner on your bank statement. If they don’t match, it’s time to investigate further.

3. Investigate Discrepancies

During the reconciliation process, discrepancies are likely to arise. These could be due to timing differences, unrecorded transactions, or bank errors. For example, checks might not have cleared yet, or specific fees may not have been accounted for in your records. It’s essential to identify the root cause of these discrepancies.

Common Issues

Outstanding checks: These have been issued but have yet to be cleared by the bank.

Unrecorded fees or payments: Sometimes, bank charges like maintenance fees or interest charges may have yet to be entered into your records.

Bank errors: Though rare, it’s possible that the bank recorded a transaction incorrectly.

4. Adjust Your Accounting Records Accordingly

Once you have identified the discrepancies, you must adjust your accounting records. This could involve entering missing transactions, correcting amounts, or addressing outstanding payments. Ensuring your records are updated will help your financial statements accurately reflect your financial standing.

Tip: Record all the adjustments you make for future reference. This will make tracking changes easier and resolve any issues that may arise later.

5. Reconcile the Ending Balances

After making all necessary adjustments, compare the ending balance on your bank statement to the balance in your accounting records. If they match, congratulations; you’ve successfully reconciled your accounts! If not, revisit the previous steps to find any remaining discrepancies.

Best Practices to Make Bank Reconciliation Smoother

Perform Reconciliation Regularly: The more often you reconcile, the easier it becomes. Monthly reconciliation is recommended for businesses, while individuals might do it quarterly or even monthly, depending on transaction volume.

Use Accounting Software: Applications like QuickBooks or Xero can help automate much of the reconciliation process, making it faster and more accurate. These platforms often include features like bank feeds, which automatically sync your bank transactions with your records.

Stay Organized: Keep all receipts, invoices, and other financial documents in one place. Organized records make reconciliation faster and reduce the likelihood of errors.

Monitor for Fraud: Regular reconciliation can help detect fraudulent transactions early, safeguarding your accounts from unauthorized activity.

Double-Check Your Work: After reconciling, take a final look to ensure everything adds up correctly. This additional step can catch any overlooked errors.

Leveraging Technology for Efficient Bank Reconciliation

Bank reconciliation is essential in financial management, ensuring an organization’s financial records match its bank statements. As businesses grow, manually handling reconciliation can become time-consuming and prone to errors. This is where technology plays a pivotal role in streamlining the process. With advancements in accounting software, AI, and cloud-based solutions, bank reconciliation has become faster, more accurate, and less burdensome.

The Role of Accounting Software: How Tools Like QuickBooks or Xero Streamline Reconciliation

Accounting software like QuickBooks and Xero have revolutionized how businesses approach bank reconciliation. These applications automatically import bank transactions, categorize them, and match them with records in the system. However, leveraging additional applications like SaasAnt Transactions or PayTraQer can further streamline and automate the process for businesses handling large volumes of transactions or dealing with multiple bank accounts.

By incorporating SaasAnt Transactions, businesses can efficiently import, export, and manage bulk financial data in QuickBooks or Xero. This reduces the time spent on manual data entry, ensuring that transactions are accurately recorded and reconciled. PayTraQer, another advanced application, syncs payment data from various platforms directly into QuickBooks, ensuring seamless reconciliation of sales and expenses. With both applications, businesses minimize the risk of errors and gain access to real-time financial insights.

One key feature of these solutions is the ability to automate transaction matching. Instead of manually sifting through transactions, QuickBooks, Xero, and enhanced integrations with applications like SaasAnt Transactions and PayTraQer use algorithms to identify matching entries, flag discrepancies, and suggest corrections. This accelerates the reconciliation process and allows businesses to focus on higher-value financial tasks.

In addition, with built-in reporting features and enhanced import/export capabilities offered by SaasAnt Transactions, businesses can generate comprehensive reports highlighting discrepancies between bank statements and company records. This real-time overview, supported by automatic synchronization through PayTraQer, ensures businesses can quickly resolve issues and maintain accurate financial statements without manual intervention.

AI and OCR Tools: Automating Reconciliation and Reducing Manual Effort

With the introduction of AI and OCR (Optical Character Recognition) tools, the automation of bank reconciliation has advanced even further. AI can analyze large volumes of financial data and detect anomalies, while OCR tools extract data from bank statements and other financial documents with minimal human intervention.

AI-powered reconciliation tools can learn from previous transactions, making future reconciliation processes smoother. They can predict and suggest the best matches for transactions, and in cases of discrepancies, AI can recommend solutions based on past patterns. This self-learning capability accelerates the process and reduces the likelihood of future errors.

On the other hand, OCR tools eliminate the need for manual data entry by scanning paper or PDF bank statements and converting them into digital data. This is particularly useful for businesses dealing with a high volume of transactions or banks that do not offer digital statement integration. These tools ensure that every transaction is captured accurately, reducing the chance of errors during reconciliation.

By leveraging AI and OCR, businesses can drastically reduce the time and effort spent on reconciliation while ensuring greater accuracy in their financial data.

Cloud-Based Solutions: Real-Time Reconciliation Benefits

The adoption of cloud-based reconciliation solutions is becoming increasingly popular, particularly for businesses looking to manage their finances from anywhere at any time. Cloud-based software offers real-time reconciliation, allowing businesses to stay updated with the latest transactions and account balances, regardless of location.

One of the primary advantages of cloud-based solutions like QuickBooks Online or Xero is the ability to synchronize bank transactions in real time. This means that the reconciliation software reflects a transaction as soon as it is made. This real-time capability allows for more accurate cash flow management and ensures that businesses have an up-to-date view of their financial health.

Moreover, cloud-based applications allow multiple users to access and collaborate on financial records simultaneously. This is especially beneficial for organizations with remote teams or businesses relying on external accountants for reconciliation. With secure access control, businesses can maintain the integrity of their financial data while allowing multiple stakeholders to engage with the records in real-time.

Cloud solutions also offer data security and automatic backups, ensuring that financial data is always protected and easily retrievable. This is particularly crucial for businesses concerned about data loss or security breaches.

Enhancing Financial Reporting Through Bank Reconciliation

Bank reconciliation is critical for ensuring a company’s financial records align with its bank statements. Discrepancies such as missed transactions, errors, or fraudulent activities can be identified and corrected by comparing the company's internal records with those from the bank. This reconciliation process is essential for maintaining the accuracy of financial reporting, which forms the foundation for informed decision-making, transparency, and trust in a business's financial health.

Accurate financial reporting helps businesses evaluate their current financial position and clearly reflects the company’s performance over time. When bank reconciliation is performed regularly, it ensures that all transactions, whether they involve sales, purchases, or expenses, are recorded correctly, contributing to reliable and precise financial statements. This alignment is essential for creating accurate profit and loss statements, balance sheets, and cash flow reports, which are critical for stakeholders assessing the company's financial viability.

How It Improves Transparency for Stakeholders and Financial Audits

Bank reconciliation is pivotal in improving financial transparency, particularly for stakeholders such as investors, lenders, and regulatory authorities. When financial records are consistently reconciled, it enhances the credibility of the reports provided to these external parties. Precise and accurate financial statements make it easier for stakeholders to understand a business's financial performance and operational efficiency, fostering trust and confidence in its management.

Moreover, bank reconciliation is crucial during financial audits. Auditors rely on reconciled records to verify that the reported financial information is accurate and complete. Well-reconciled bank accounts streamline the audit process, as auditors can quickly validate transactions, detect any discrepancies, and ensure that financial statements comply with accounting standards. This accuracy meets the requirements of external audits and prepares businesses for internal audits, further reinforcing the organization’s commitment to financial integrity.

Importance for Tax Compliance and Regulatory Adherence

Adhering to tax compliance and regulatory standards is a top priority for global businesses, and bank reconciliation is indispensable. Regular reconciliation ensures that all transactions are correctly recorded, minimizing the risk of discrepancies that could lead to underreporting or overreporting taxable income. Accurate financial data derived from reconciled bank accounts supports the preparation of tax returns, helping businesses meet their tax obligations with confidence.

Additionally, regulatory bodies in many countries require businesses to maintain accurate and detailed financial records. Bank reconciliation ensures that the financial reports submitted for regulatory compliance reflect the company's financial state. This process reduces the risk of penalties, audits, or investigations from inaccurate reporting, thus helping businesses avoid legal issues and maintain a good standing with regulatory authorities.

Bank Reconciliation and Financial Planning

Bank reconciliation plays a significant role in both short-term budgeting and long-term financial planning. By comparing internal financial records with bank statements, businesses and individuals can ensure that every transaction is accurately recorded, giving them a clear picture of their current financial position. This clarity is essential for effective budgeting, as it allows for the accurate tracking of income and expenses. When budgets are based on reconciled and reliable data, financial forecasts become more precise, reducing the risk of overspending or underestimating future financial needs.

Consistent bank reconciliation provides insights into spending patterns and cash flow management for long-term financial planning. This helps set realistic financial goals for business growth, expansion, or personal wealth accumulation. Accurate financial data also aids in planning for large-scale investments, ensuring that funds are available when needed and that unforeseen expenses are avoided. Individuals and businesses can create well-informed strategies that foster long-term financial stability and growth by integrating bank reconciliation into financial planning.

Benefits for Personal Savings, Business Expansion, and Investment Decisions

Bank reconciliation offers tangible benefits for both personal and business financial management. For individuals, reconciling bank accounts regularly helps track savings progress and manage personal finances more effectively. By identifying unnecessary expenditures and ensuring that all sources of income are accounted for, personal savings can be optimized. This practice also safeguards against potential fraud or bank errors, ensuring that personal finances remain healthy and secure.

Bank reconciliation is a powerful tool for supporting the expansion and growth of businesses. Clear, reconciled financial records allow businesses to assess their current financial position accurately, making planning for new investments or expansion projects easier. Additionally, businesses that regularly reconcile their accounts have better insights into their cash flow, helping them to allocate resources efficiently, negotiate better terms with suppliers, and make informed investment decisions. A solid financial foundation built on consistent bank reconciliation ensures businesses can confidently pursue growth opportunities while mitigating financial risks.

From an investment perspective, reconciling accounts allows individuals and businesses to make better decisions. With accurate and up-to-date financial information, investors can assess the viability of potential investments, ensuring that they have the necessary capital to support their plans without affecting day-to-day operations or personal financial stability.

How Regular Bank Reconciliation Helps with Tax Preparation?

Ensuring Accurate Tax Filings by Keeping Clean Financial Records

Regular bank reconciliation is a critical step in ensuring accurate tax filings. By consistently reconciling bank accounts, businesses and individuals can maintain clean and up-to-date financial records, which form the basis for precise tax reporting. When financial transactions are correctly categorized, and any discrepancies between bank statements and internal records are identified and corrected, businesses can be confident that all income and expenses are accurately reflected in their tax filings. This meticulous approach to record-keeping minimizes the risk of errors, ensuring that tax returns are complete and precise.

Accurate financial records also help claim all eligible deductions, ensuring that tax liabilities are not inflated due to missed expenses. Inaccurate records can lead to misreporting income or overlooking necessary deductions, which could increase the tax burden unnecessarily. Therefore, regular bank reconciliation ensures that every financial detail is captured, making the tax preparation process smoother and more reliable.

Avoiding Penalties from Incorrect Tax Submissions

Incorrect or incomplete tax filings can lead to significant financial penalties, fines, and legal consequences. One of the most effective ways to avoid these penalties is to ensure that all financial records are accurate through regular bank reconciliation. By reconciling accounts frequently, businesses and individuals can detect errors, omissions, or fraudulent transactions in real-time and correct them before tax season.

Additionally, when all financial records are in order, the risk of underreporting income or overstating deductions is significantly reduced, helping taxpayers avoid penalties for non-compliance. Properly reconciled records prevent mistakes and make it easier to compile tax information quickly and efficiently, reducing the chances of filing late or submitting incorrect information.

Tax Audits: Be Prepared with Proper Reconciliation Records

Properly reconciled bank records can be a lifesaver in a tax audit. Auditors typically request documentation to support the information provided on tax returns, and reconciled bank statements are a critical part of this documentation. If financial records are organized and accurate, the audit process can become much more stressful and time-consuming, potentially leading to fines or additional tax liabilities.

By performing regular bank reconciliations, businesses, and individuals can ensure that their financial records are accurate and audit-ready. Well-maintained and reconciled records provide transparency and proof of all financial transactions, helping auditors verify the accuracy of tax filings and reducing the likelihood of prolonged audits. In this way, bank reconciliation is a proactive measure that allows taxpayers to be well-prepared for scrutiny from tax authorities.

Best Practices for Ongoing Bank Reconciliation

Frequency of Reconciliation: Weekly, Monthly, or Quarterly

One of the most important aspects of maintaining accurate financial records is determining the right frequency for bank reconciliation. Depending on a business's size and complexity, reconciliations can be performed weekly, monthly, or quarterly. For larger businesses with a high volume of transactions, weekly reconciliation is recommended to identify and correct discrepancies in real-time. This frequent reconciliation helps quickly catch errors or unauthorized transactions, preventing them from snowballing into more significant issues.

On the other hand, small to medium-sized businesses may find that monthly reconciliations are sufficient, as they typically deal with fewer transactions. However, more frequent reconciliations may be necessary during peak business periods, such as year-end or tax season, to maintain financial accuracy. Though less common, quarterly reconciliation can be a good approach for businesses with few transactions, such as seasonal operations. Regardless of the chosen frequency, the key is consistency to ensure the business's financial health.

Recordkeeping Tips: Ensure Consistency and Accuracy in Records

Proper recordkeeping is crucial for practical bank reconciliation. Ensuring consistency and accuracy in financial records makes the reconciliation process more efficient and reliable. To achieve this, businesses should use a standardized method for documenting transactions, categorizing income and expenses, and maintaining receipts and invoices. By implementing a systematic approach to recordkeeping, it becomes easier to identify discrepancies during reconciliation and address them promptly.

Using accounting software can also help automate the reconciliation process, reducing the risk of human error and ensuring that records are always up to date. Additionally, businesses should conduct periodic reviews of their financial records to ensure that all transactions are correctly categorized and that no data is missing. Consistent and accurate recordkeeping supports seamless bank reconciliation and strengthens overall financial management.

Involve Multiple Team Members: The Benefits of Having Multiple Checks for Businesses

Involving multiple team members in the reconciliation process can significantly enhance accuracy and accountability. For businesses, implementing a system of checks and balances ensures that financial records are reviewed by more than one person, reducing the likelihood of errors or fraud. Assigning different team members to handle various aspects of bank reconciliation, such as one person preparing the records and another verifying them, provides an additional layer of oversight.

This practice is particularly beneficial for larger businesses, where the complexity and volume of transactions may increase the risk of discrepancies. Involving multiple team members not only distributes the workload but also ensures that anomalies are spotted quickly and addressed effectively. Moreover, having a collaborative approach to reconciliation fosters transparency within the finance team and ensures that financial records are reliable for reporting and decision-making.

Common Myths and Misconceptions About Bank Reconciliation

Bank reconciliation is critical to maintaining financial accuracy, yet it is often misunderstood. Misconceptions about its purpose and necessity can lead to significant financial discrepancies. Let's debunk some of the most common myths surrounding bank reconciliation to understand its importance for businesses and individuals better.

Myth 1: Reconciliation is Only for Businesses

Debunked

Many believe bank reconciliation is exclusively for businesses, but this is far from the truth. While companies certainly benefit from regular reconciliation to track their cash flow, individuals should also engage in this practice. Personal bank accounts can be vulnerable to errors, unauthorized transactions, and mismanagement like business accounts. Reconciling personal bank statements helps individuals ensure their financial records match what the bank reports, allowing them to avoid overdrafts, manage spending, and identify any discrepancies early on.

Why Does it Matter for Individuals?

Personal finance is often neglected, but regular bank reconciliation can help maintain financial health. Keeping accurate records allows you to spot errors or unauthorized transactions promptly, which could otherwise go unnoticed until it's too late.

Myth 2: If I Don't See Any Problems, My Account is Fine

Debunked

A common misconception is that everything is in order if there are no apparent issues. However, just because there aren’t immediate, noticeable problems doesn’t mean your account is flawless. Some discrepancies, such as bank errors, forgotten automatic payments, or duplicate transactions, can only be detected through thorough reconciliation. Additionally, minor discrepancies might accumulate over time, leading to significant financial consequences in the long run.

Reconciling ensures accuracy

Bank reconciliation helps uncover hidden issues that might not be visible through a glance at your balance. It provides a layer of financial oversight, ensuring that all transactions are accounted for correctly, no matter how minor.

Myth 3: Bank Statements Are Always Accurate

Debunked

Many individuals trust their bank statements, assuming they are 100% accurate. While banks have sophisticated systems in place to minimize errors, they are not infallible. Mistakes can occur, such as duplicate charges, incorrect transaction entries, or delays in processing. Relying solely on your bank statement without reconciling it against your records can result in missing critical mistakes that could affect your financial stability.

The Role of Reconciliation

You double-check the bank’s records against your own by reconciling your statements. This cross-verification process helps catch errors before they snowball into more significant problems, ensuring you always have an accurate representation of your financial standing.

Educating Readers on the Importance of Reconciliation

Whether you manage a business or your personal finances, bank reconciliation is essential for maintaining accuracy and financial integrity. It helps identify discrepancies, catch fraudulent activities, and record all transactions correctly. Regular reconciliation can improve your financial awareness and security, allowing you to avoid costly mistakes in the future.

By debunking these myths and understanding the actual value of reconciliation, you can maintain better financial health and ensure that your financial statements reflect the reality of your situation.

Wrap Up

Bank reconciliation is not just an occasional task; it should be viewed as a crucial financial habit that can protect your finances and promote overall financial health. By making bank reconciliation a regular practice, you can safeguard against fraud, ensure the accuracy of your financial records, and achieve greater peace of mind.

One of the primary benefits of regular bank reconciliation is its role in detecting fraudulent activity or unauthorized transactions. Financial discrepancies, accidental or intentional, can be spotted early through diligent reconciliation, allowing you to take corrective actions swiftly. Reconciling your statements regularly ensures that your accounts are monitored and protected.

Financial accuracy is essential for both personal and business finances. Inaccurate records can lead to incorrect financial reporting, affecting budgeting, tax reporting, and overall financial decision-making. Through regular reconciliation, you ensure that your financial records align perfectly with your bank statements, helping you avoid costly mistakes and mismanagement of funds. By maintaining precise records, you can confidently manage your cash flow and clearly understand your financial position.

Financial stress often stems from uncertainty about your finances. Regular bank reconciliation offers the peace of mind of knowing your accounts are accurate and up-to-date. This clarity lets you make informed financial decisions for personal budgeting or business planning. When you reconcile frequently, you gain control over your finances, reducing anxiety and helping you avoid potential issues.

To make bank reconciliation easier and more efficient, it's recommended that you leverage advanced accounting tools that automate and streamline the task. Applications like SaasAnt Transactions and PayTraQer, integrated with platforms like QuickBooks and Xero, offer seamless reconciliation processes by effortlessly importing, categorizing, and matching transactions. These tools save time, reduce the chance of human error, and ensure that your financial records are consistently accurate.

Start building a habit of regular reconciliation today, and consider using these applications to simplify the process. Whether you manage personal finances or run a business, establishing a reliable reconciliation routine will contribute to your financial security and long-term success.

FAQs

What Is Bank Reconciliation, and Why Is It Important?

Bank reconciliation compares your bank statement with your financial records to ensure both are accurate and aligned. It is essential because it helps identify discrepancies, detect fraud, correct errors, and ensure that your financial statements are up to date.

What Are the Benefits of Using Tools like Quickbooks or Xero for Reconciliation?

Using accounting tools like QuickBooks or Xero automates the reconciliation process by importing bank transactions, matching them with your financial records, and flagging discrepancies. This saves time, reduces manual errors, and ensures that your records are always accurate and up to date.

How Can SaasAnt Transactions Simplify Bank Reconciliation?

SaasAnt Transactions simplifies bank reconciliation by automating the import and categorization of financial transactions into QuickBooks or Xero. It eliminates the need for manual data entry, ensuring that bank statements match financial records easily and accurately.

What Is PayTraQer, and How Does It Help with Reconciliation?

PayTraQer is a powerful tool that syncs online payment transactions from platforms like PayPal, Stripe, and Square directly into QuickBooks and Xero. It streamlines the reconciliation process by matching incoming payments with the correct transactions, reducing manual errors and saving time.

Can SaasAnt Transactions and PayTraQer Help Prevent Reconciliation Errors?

Yes, both SaasAnt Transactions and PayTraQer minimize reconciliation errors by automating transaction imports and ensuring that each transaction is accurately categorized and matched. This reduces the likelihood of duplicate entries, misclassifications, or missing data.

How Does PayTraQer Improve Reconciliation for E-commerce Businesses?

PayTraQer is particularly beneficial for e-commerce businesses. It automatically syncs multi-channel payments from online platforms like Shopify, Amazon, and Etsy into accounting software. This ensures that all sales and transaction fees are reconciled correctly, providing a clear financial picture.

What Are the Benefits of Using SaasAnt Transactions for Bulk Data Imports in Reconciliation?

SaasAnt Transactions supports bulk data imports, allowing you to import thousands of transactions simultaneously into QuickBooks or Xero. This feature is handy for businesses with high transaction volumes, as it saves time and ensures that all transactions are accounted for during reconciliation.

Can SaasAnt Transactions and PayTraQer Be Integrated with Both QuickBooks and Xero for Reconciliation?

Yes, both SaasAnt Transactions and PayTraQer integrate seamlessly with QuickBooks and Xero, providing comprehensive support for bank reconciliation. These integrations ensure that your financial data is accurately reflected across all platforms, improving the efficiency and reliability of your reconciliation process.

Read also